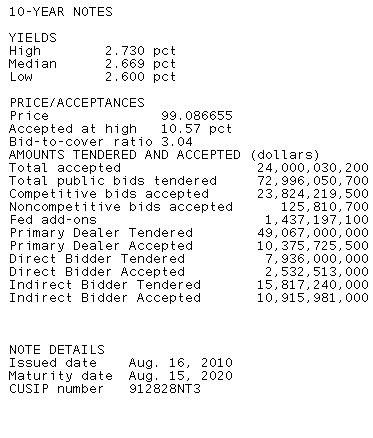

The Treasury just sold $24 billion 10 year notes.

The bid to cover ratio, a measure of auction demand, was 3.04 bids submitted for every one accepted by Treasury. While this is a bit below average, demand was still 3 times the amount offered which is never a bad thing, especially when you consider the last "When Issued" 10-year note was nearly 40bps higher in yield.

Primary dealers were awarded an average amount of inventory, 43.6% of the issue. Directs took down 10.6% of the issue, this is below average but an improvement from the July auction where directs were awarded a six auction low of 9.8%. Indirects were big buyers, taking home 45.8% of the competitive bid. This is above average and their largest award since November. Overall this was a strong auction when you consider how expensive the 10yr note is relative to the rest of the curve and outright vs. previous auctions.

Stocks are tanking and the long-end of the yield curve is outperforming. S&Ps are officially in "falling knife mode", down 30 handles to 1090. Meanwhile, 2s/10s are another 6bps flatter at 218bps. 10s haven't lost a step since auction results flashed. The 3.50% coupon bearing 10-year note is currently +0-19 at 106-26 yielding 2.703% (-6.6bps on session). Below is the long-term 10yr note yield chart we've been watching. 10s are on the verge of entering the PANIC ZONE we discussed on August 2

While mortgages have lagged the TSY rally, they aren't far off the pace. The September FNCL 4.0 is +0-09 at 102-26 and the FNCL 4.5 is +0-04 at 104-23.

I'm going back to the beach to enjoy my "vacation"....use the comments to update each other.