A flurry of data just flashed...

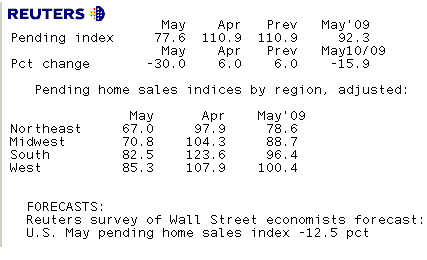

Pending Home Sales: The Pending Home Sales Index dropped 30.0 percent to 77.6 based on contracts signed in May from a reading of 110.9 in April, and is 15.9 percent below May 2009 when it was 92.3. The falloff comes on the heels of three strong monthly gains as home buyers rushed to take advantage of the tax credit. Weakness was evident across the country. WORSE THAN EXPECTED

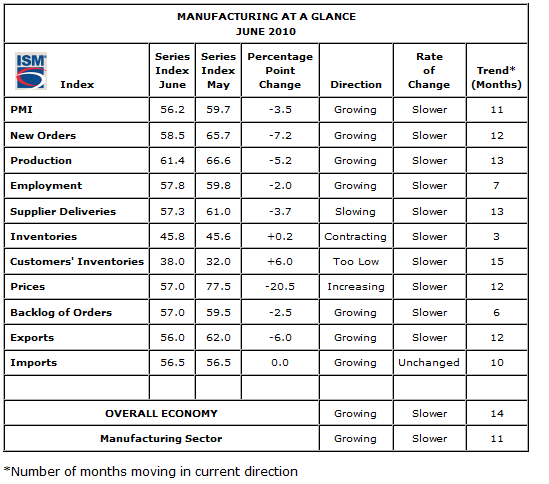

ISM Manufacturing: The PMI came in at 56.2 vs. expectations for a read of 59.0 vs. the previous print of 59.7. The prices paid index moved significantly lower, from 77.5 in May to 57 in June vs. expectations for a read of 71.0. The Employment Index declined from 59.8 to 57.8. WORSE THAN EXPECTED

Although economic activity in the manufacturing sector expanded in June for the 11th consecutive month and the overall economy grew for the 14th consecutive month (index > 50 = economic expansion), every category but inventories and imports failed to match index levels seen in May.

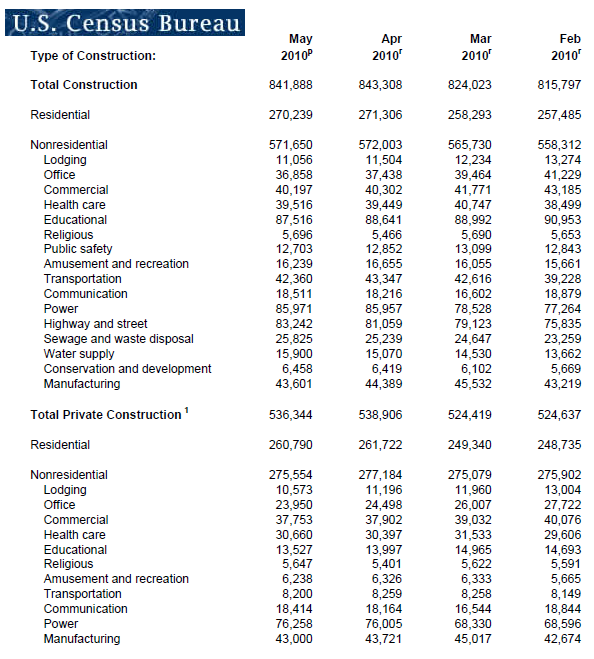

Construction Spending: Construction spending during May 2010 was estimated at a seasonally adjusted annual rate of $841.9 billion, 0.2 percent below the revised April estimate of $843.3 billion. The May figure is 8.0 percent below the May 2009 estimate of $915.4 billion. During the first 5 months of this year, construction spending amounted to $314.2 billion, 12.0 percent below the $356.9 billion for the same period in 2009. Private residential construction was at a seasonally adjusted annual rate of $260.8 billion in May, 0.4 percent below the revised April estimate of $261.7 billion. BETTER THAN EXPECTED

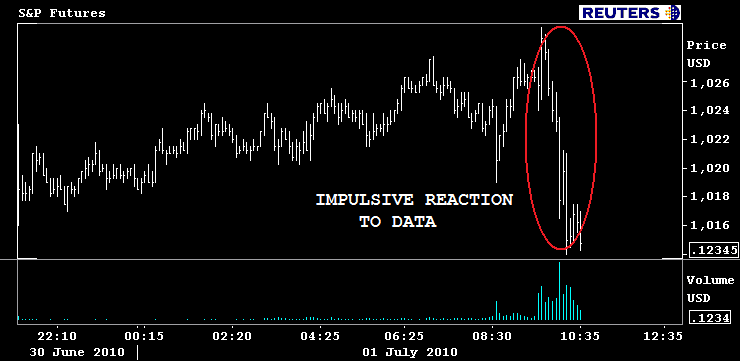

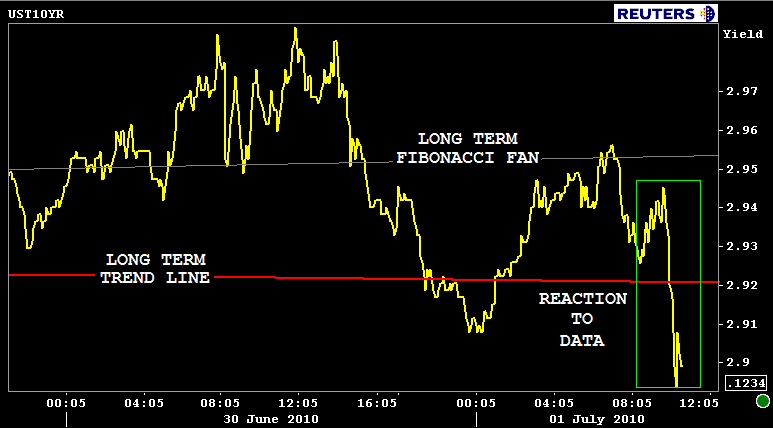

Stocks are getting smashed. S&Ps are -16.75 at 1009. Still searching for a floor....

The 10yr note is trading below 2.90%, currently +0-12 at 105-06 yielding 2.892% (4.3bps lower on the day). The 2s10s curve is another 4bps flatter at 229bps.

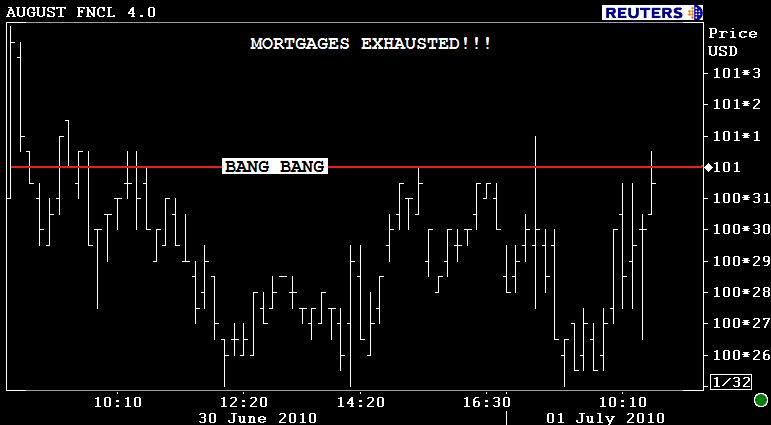

This seems like good news for mortgage rate watchers but MBS aren't keeping up with their benchmark big brothers. The August delivery FN 4.0 MBS coupon is +0-02 at 101 the figure. The secondary market current coupon is UNCH on the day at 3.829%. Yield spreads are WIDER. Here are my marks: the current coupon yield is +92.7 basis points over the 10yr TSY note yield and 85bps above the 10yr IRS.

Rate sheet influential MBS are exhausted (fears of negative convexity grip valuations).

I haven't updated my spreadsheet yet but I assume loan pricing isn't improved vs. yesterday....