Markets are taking a break from capitulative-esqe behavior today...

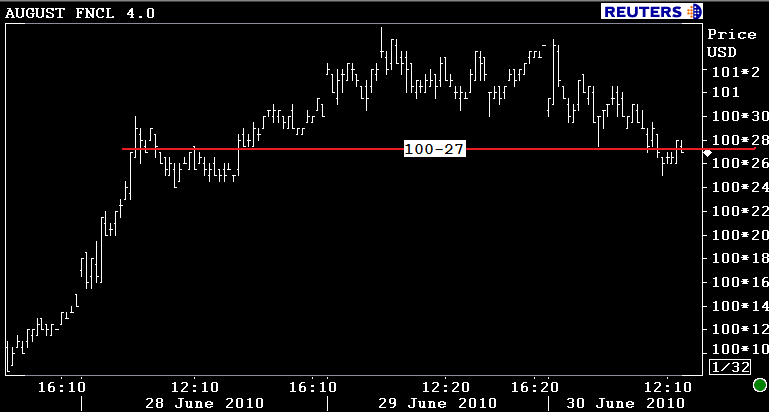

The August delivery FN 4.0 has given back the modest price improvements seen yesterday, currently bid -0-08 at 100-28. The secondary market current coupon is 3.7 basis points higher at 3.841%. Yields spreads are wider which implies there is localized weakness in "rate sheet influential" MBS coupons. Here is my scorecard: the CC is +86.7 basis points over the 10yr TSY note yield and 80.9 basis points over the 10yr IRS.

100-27 is support...

The benchmark 10 year TSY note is also giving back the gains seen yesterday, currently -0-04 at 104-17 yielding 2.967%. As profits are consolidated, energy is being stored for another directional move. Essentially the 10yr note is in "wait and see" mode.

Stock futures have generally ticked sideways at higher handles today and the beginnings of a supportive base has formed around 1035, that base has been defended twice already this morning. I'm not looking into this price action too deeply. Stock trader sentiment is decidely bearish but a modest uptick in open interest at the price lows implies there is bargain buyer interest out there...unfortunately short term signals are extremely mixed because investor participation is paltry.

Overall, these observations imply uncertainty is the only certainty in the marketplace. While this is to be expected ahead of a major economic event (the Employment Situation Report), recent BIG PICTURE developments lead us to believe the market's attention has re-focused on macroeconomic fundamentals as opposed to the microeconomic earnings potential of the most profitable U.S. companies. This perspective leaves rate watchers feeling more bullish than bearish...but I wouldn't bet the farm on floating right now because the 3.50 MBS market has yet to liquefy. This puts a floor under further positive progress, at least until 10s settle in a range below 2.85% READ MORE ABOUT WHY THE 3.5 MBS COUPON MATTERS TO LOAN PRICING

Q2 ends today and Q3 starts tomorrow with pending home sales and the Employment Situation Report on Friday. If you're floating in the short term, it is EXTREMELY UNLIKELY that 3.5 MBS start trading with enough liqudity to warrant further mortgage rate improvements. While you may see a few extra bps here and there, this is one of those times where pigs get fat and hogs get slaughtered.