Today is Class

A Notification Day in the TBA Secondary Mortgage Market. Class A MBS coupons consist of Fannie Mae and Freddie Mac 30 year loan notes.

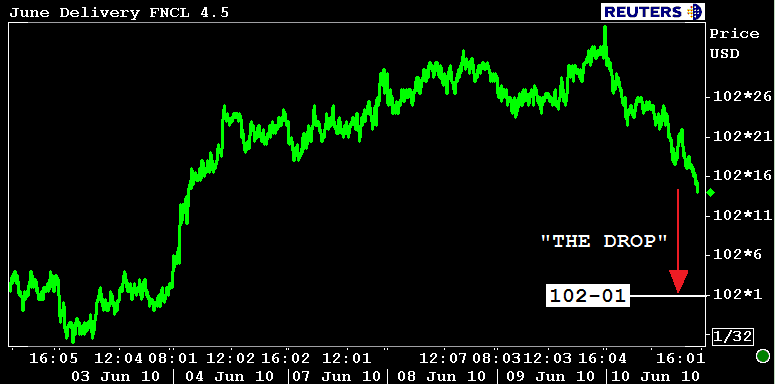

The June FN 4.5 MBS coupon has now begun the settlement process. Before the

end of the session, the FN 4.5 price will seem to fall from where it is

currently priced at 102-14, all the way down to 102-01.

WHY???

The MBS coupons that determine rate sheet

pricing are traded in the TBA MBS market.

TBA = To be Announced

In the TBA MBS market, at the

time a trade is made, buyers and sellers agree to a few specific terms

like what coupon, the issuing agency (Fannie, Freddie, Ginnie), size of

trade, and a buy/sell price....the actual pools of loans are NOT

exchanged at the time of this commitment. Instead, the MBS buyer and the

seller make an agreement to complete the transaction at a later date.

In the MBS market this date is pre-determined; it is called SETTLEMENT

DAY (clever name huh?).

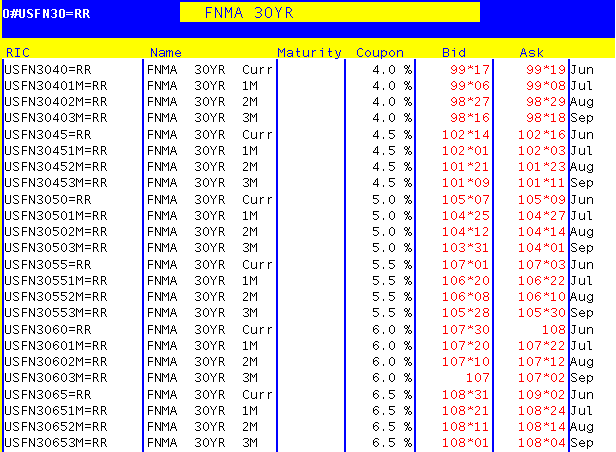

Agency MBS trading settles once a

month. We've been watching the June FN30 4.5 MBS coupon trade since May 11, 2010. As of tomorrow morning, we'll be watching the July FN30 4.5 MBS coupon until July 12, 2010 (August coupons for 30 day locks).

We can

actually watch forward pricing as much as three months ahead.

SEE:

Anyway...two

days before the pre-scheduled settlement date, the MBS seller

"notifies" the MBS buyer of the specific pools that they will deliver to

satisfy the previously agreed upon terms of the trade.

This

is Fannie Mae's guidance:

Forty-eight hours prior to

settlement, pool information must be communicated to the Capital Markets

Sales Desk's back office by phone (202-752-5384), facsimile

(202-752-3439), or via EPN transmission. Delivery of pool information

must take place by 3:00 p.m. eastern time. It is advisable that pool

information is communicated early as phone lines, fax machines, and the

EPN queues are extremely taxed as the 3:00 p.m. deadline approaches. If

the transmission does not occur by 3:00 p.m., one day's fail will be

incurred, despite the fact the information is residing in queue.

Then

the MBS buyer reviews the pool information to ensure the seller has

delivered loans that meet the agreed upon terms. 48 hours later, after

being deemed to within "Good Delivery" guidelines, pool purchase funds

are wired and the trade is complete (it goes deeper...this is the

outline).

BUT WHY DO PRICES SEEM TO FALL WHEN WE ROLL FROM

FRONT MONTH TO BACK MONTH COUPONS?

Today the front month is

the June delivery coupon. The back month is the July coupon.

Prices

don't really fall though. We just start watching the back month MBS

coupon because the front month coupon has just entered into the

settlement process. The back month coupon price remains the same!

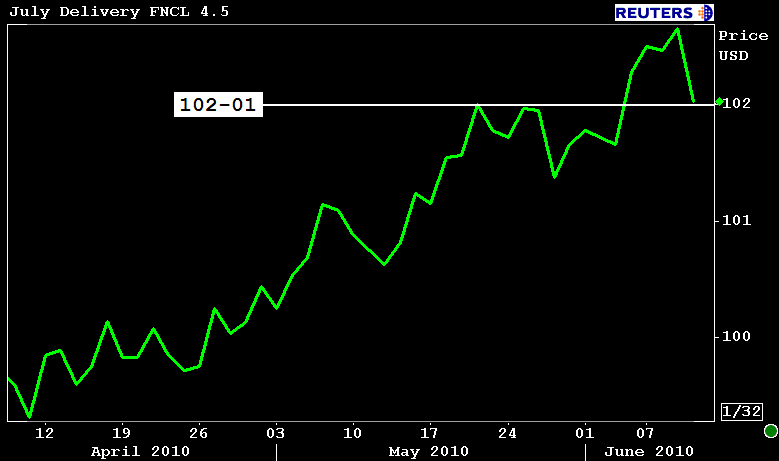

Below

is the current July settlement FN 4.5 MBS coupon. It's bid at 102-01.

This is where prices will "seem" to fall later this afternoon.

The main reason behind the price

"DROP" is lost "time value of money".

Interest rates can be

thought of in three ways..

- Required Rate of Return: this is the minimum amount of return an investor is willing to receive when making an investment.

- Discount Rate: the rate used to determine the present value of future cash flows. When you loan someone money with the intention of being paid back in the future, you must place a value on how much of a premium you are losing by not spending that money right now. The discount rate is essentially how much you are charging to delay repayment until a future date.

- Opportunity Cost: the value an investor passes up when choosing an alternate investment. You must earn enough interest when you loan someone money to compensate for the loss of income that you could have been earning by investing elsewhere.

LET ME POSE A QUESTION: Would you rather have $1.00 today or

$1.00 tomorrow?

You would rather have $1.00 today! If you have

$1.00 today you can invest it today...the fact you are investing

today vs. tomorrow implies you are giving the asset more time to

appreciate, more time to accumulate interest earned (ACCRUE).

To

relate this concept to the MBS market---if you buy the June FN 4.5

coupon, then your returns will begin accruing on June 1. If you buy the

July coupon---your returns don't start accruing until July 1. That means

you would have to wait 20 days (from today) for your money to start working for

you. Investing now, before the roll, puts money to work now, or in today's case, on June 1.

Starting tomorrow, because the June coupon has entered into the

settlement process, MBS investors will have to wait until July 1 to see

their funds start working. To compensate for the lost Time Value of

Money, investors demand higher MBS yields. This lost time value of money

is represented by lower back month MBS prices (in this case the July

FN 4.5 coupon).

Note: to be clear, the previous owner has

rights to the income (accrued interest) earned from while they owned the

coupon. The price you pay to purchase the back month coupon includes

the income the current owner has accrued while they owned the coupon.

The buyer recovers the added premium when the coupon payment is

deposited in their account. This is called the 'clean price'...its the

same way Treasuries trade.

Plain

and Simple: If you own the June FN 4.5 MBS coupon, then you

are entitled to the coupon clips (income) paid in June. If you decided to

wait and buy the July MBS coupon...then you have to wait until July for

your investment to start accruing interest. To compensate for the lost

"time value of money", investors demand higher yields, which is why

prices fall when delivery rolls from front month to back month. (not including any profit earned from price movement)

This

explains why 60 and 90 day locks are more expensive. The longer the

lock commitment period, the more it costs the lender to hedge

interest-rate volatility and fall out risk.