The Treasury has successfully auctioned $36 billion 3-year notes. This is $4 billion below the April 6, 2009 issue and the smallest 3-yr offering since August 2009.

The bid to cover ratio, a measure of auction demand, was 3.23 bids submitted for every one accepted by the Treasury. This is well above the ten auction average of 2.99 and the five auction average of 3.06.

Bidding stopped out at a high yield of 1.220%---which was less than 1 basis point below the 1pm "when issued" quote. Cash market yield will be based on a semi-annual 1.125% coupon payment. That is 20bps below the previous coupon of 1.375% and 62.5bp below the April issue. I believe 1.22% is the 2nd lowest "high yield" ever recorded at a 3-yr note auction...only the January 2009 auction was lower (1.20%)

Primary Dealers, aka the street, took down 36.9% of the auction. This is about average vs. recent norms. Dealers were more aggressive bidders but still not big buyers of this maturity. 17.6% of their bids were accepted.

Direct bidders, aka domestic fund managers like Vanguard and PIMCO, were awarded 16.3% of the issue. This is above the ten auction average of 8.2% and the five auction average of 14.2%. Unlike dealers, direct bidders continue to be big supporters of 3 year note auctions.

Indirect buyers took home 46.7% of the auction. This is well below recent norms.

Plain and Simple: 3s were the weakest spot on the curve all morning as traders built in a modest debt supply concession before Treasury cutoff bids at 1pm (thanks to a stock "rally"). The concession, while not huge, was large enough to draw out healthy demand from direct bidders and primary dealers, who offset less aggressive demand from indirect buyers. Most importantly, primary dealers were not forced into underwriting the majority of this new issue (+50.% of issue awarded). It was a strong auction overall.

It's been a choppy day in financial markets but price action has been contained in a well-defined range.

Stocks are playing follow the leader with the Euro. Currently the Euro is +0.13% at 1.1933 and the S&P is +0.39% at 1054.54. The EU member currency managed to breach the 1.20US$ handle again, but that move lasted less than a minute. Gold is $15 off its newly hit record price highs.

10s have mostly mirrored the movements of equities, trading in a choppy manner between 3.19% and 3.15%. The FN 4.0 is +0-04 at 100-09 and the FN 4.5 is +0-01 at 102-30. The secondary market current coupon is 1.2bps lower at 3.985%. Yield spreads are tighter (even though vols are higher).

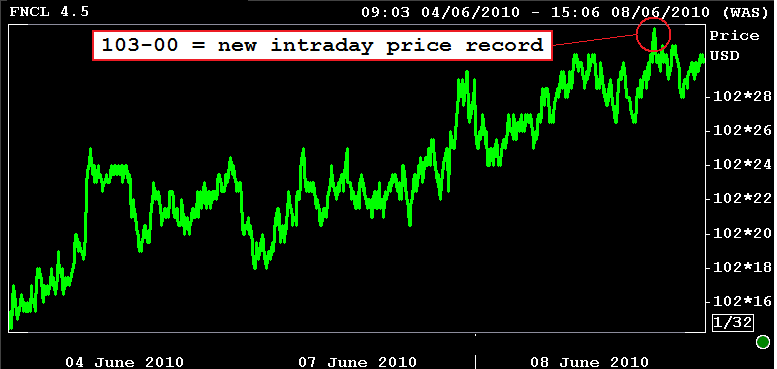

MBS profit taking has been seen as "rate sheet influential" coupon prices hit new intraday price records today. The FN 4.5 touched 103-00 after the auction!

Depending on fallout, your secondary marketing department may be underwater on their pipeline after the recent run-up in MBS prices.

If fallout is on the rise or new loan apps aren't coming in as fast as one might expect given uber low mortgage rates, the operation is likely losing money on the decision to peel off its forward hedge or make up the losses on a new trade (which are primarily in July coupons btw. July = 30 day lock). If this is the case you can rest assured these added hedging costs would show up in your rate sheets at some point down the road...and loan officers would think lenders were being greedy.

If fall out is a non-issue or new loan apps are pouring into the pipeline, at these prices secondary can make a decent profit on the pulled through portion of the pipeline OR offer your NEW loan applicants lower mortgage rates without losing the margin they need to make a living. One way to profit on the MBS price rally, assuming fall out has been limited, is to assign the old forward commitment (taken down at 102-00 price) to a dealer or bigger mortgage banker. After that, they would sell forward a new loan commitment at current market and either lock up the current floating portion of the pipeline with a little extra juice baked in or just buy the market with lower rates. I gather the first option is most attractive at the moment.

This really only applies to lock desks who sell loans on a mandatory basis. Best Efforts lenders are free to flip flop as they please without having to deal with pair-off fees (to an extent). Assuming most of the larger loan operations use mandatory commitments, secondary should've bought back their hedges as MBS prices rose. If hedging the pipeline is primarily a function of pull-through, that probably didn't happen and now some lenders are being forced to renegotiate with borrowers...which eats away at their profit margins. Again these added costs would likely end up being baked into your loan pricing at some point down the road.

You tell me, are y'all losing deals as rates fall or have new disclosure regs helped keep your clients locked at current rates?