Security has been tightened up across the U.S after two suicide bombers attacked the Moscow metro system this morning, killing at least 38 people and injuring 65 more. Islamic extremists from the North Caucasus region of Russia are believed to be the source of the bombing, however authorities are not taking any chances after an Al-Qaeda plot to attack the NYC subway system was foiled in late 2008. In D.C and New York there are bomb sniffing dogs patrolling train/metro/subway stations and civilian law enforcement tensions are high.

No one go Michael Douglas, "FALLING DOWN" please...

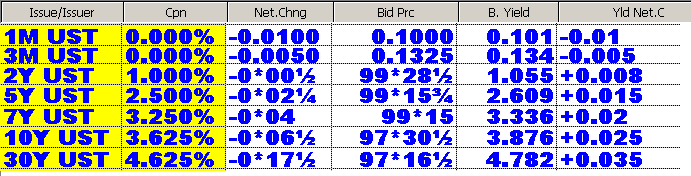

The most obvious headline to me in the rates market today would be the long bond hitting a nine-month yield high today. Read more below...

The long end of the yield curve is the biggest loser today. In order from worst to best: 30s,10s, 7s, 5s, 2s. See "Yld Net. C" column. I call this a "disdain for duration".

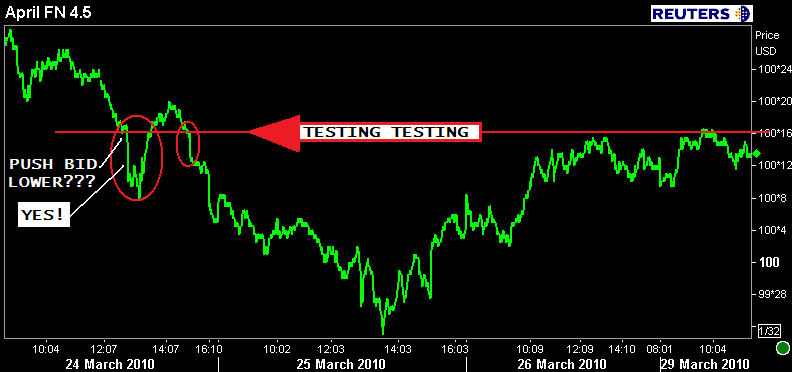

The 3.625% coupon bearing 10 year TSY note trend channel is consolidating. We grow increasingly more nervous as the channel narrows . Once the two red lines meet, we expect price action to take a new course...either higher or lower. Then, again...many market paricipants are sitting it out...waiting for more guidance. So while morning action may look like a trend at the moment, it's likely just range bound chopatility. This implies 10s may rise up to 3.90% before the day is over.

Mortgages are flat. The FN 4.0 is -0-03 at 97-03 yielding 4.282% and the FN 4.5 is -0-02 at 100-11 yielding 4.465%. The secondary market current coupon is 4.456%. The current coupon yield is 57.0 bps over the benchmark 10 yr TSY note and +62.3bps over the 10yr swap rate.

The sideways nature of today's session is a bit more obvious when looking at FN 4.5s.

Stocks look the same as 10s...but are likely heading sideways.

Plain and Simple: the long end of the yield curve is the biggest loser today. This is most likely a function of low trading volume and a thinly attended marketplace. Working market participants are selling into strength and buying at the lows.....this is expected to continue at least until new data or an event provides more meaningful directional guidance. This implies RANGE TRADING is in effect! Thus, in the hours ahead 10s could re-test 3.90% which will raise reprice alert concerns. Don't panic, the range is still in play. Stay tuned...

Looking further ahead, the Fed finishes up the MBS Purchase Program on Wednesday. I would expect to see increased volatility around this event...with "rate sheet influential" MBS coupons playing a bit less follow the leader with 10s than we are accustomed. If benchmark 10 year notes rally, don't expect the FN 4.5 to keep pace. When 10s sell, the FN 4.5 should make up lost ground. Call it a "feeling out" period if you want...either way the road ahead for mortgages specifically is more uncertain than it has been since November 2008. Stay defensive of any increases to rate sheet rebate. My strategy would be to ride this out and hope for a few more bps from lenders in the next 24 hours, but I would register locks and keep close watch of the MBS stack.