Markets were thinly traded yesterday as there was no domestic data to digest and Japan was off for the annual "Coming of Age" holiday....leaving market participants more or less in a holding pattern, waiting on something more substantial to trade on.

The resulting effect was a slow sideways shift for "rate sheet influential" debt...all while stocks enjoyed a modest rally that led the S&P and Dow to new 15 month highs.

The 10yr TSY note went out at the highly trafficked 3.82% pivot point, which was high enough to lead the yield curve to new record steepness levels. The S&P was up 0.17% to 1,146 (a fresh 15 month index high), the Dow rose 0.43% to 10,663 (a fresh 15 month high).

FRESH 15 MONTH HIGHS!?!?! WHAT? WHY?

I spent a fair amount of time over the summer into early fall discussing positive progress made in stock markets since March 2009. At that time the overwhelming perception of the equity market was one of frustration regarding the consistent bias to buy buy buy. Fast forward to present day and nothing has changed. Stocks are still rallying (freight train) and many still feel the non-stop recovery rally is unwarranted as perceptions of economic reality are not truly indicative of "better things to come" in the marketplace. I think we are all in need of a reminder of where stocks were and how far they have come since finding a bottom in March09.

The worst case scenario was priced into stocks from October08 to March09. During that time the Federal Reserve and Treasury worked tirelessly to restore stability to financial markets. Soon thereafter we began to see a slowing in the pace of contraction and a turning of the tide in investment outlooks. Bottom pickers started re-allocating funds towards risk and sentiment shifted from "WORSE CASE SCENARIO" to "BETTER THAN EXPECTED". To keep it short and sweet...stocks have merely recovered the "WORST CASE SCENARIO" discount and are now in a bit of a gray area...below the pre-crash range but above the crisis induced dip.

So while I understand the frustration one might foster over the positive progress made in the equity market...I cannot say it is totally unjustified. I can however say that 1200 is going to be a VERY important pivot point. The 9 month rally in stocks will be put to the test...the perception of economic "better than expecteds" will have its day of reckoning when the S&P approaches 1200. It wouldn't surprise me to see stocks continue their march higher until then though..

Lastly, sayings like "FRESH 15 MONTH HIGH" make me laugh, in fact I view them in a similar manner as I view economic data. Yes, there has been a stabilization. Am I willing to call it a recovery? NO. I am willing to say that we have STABILIZED from the worst case scenario (in markets and economic data)...don't confuse a financial market recovery from the "worst case scenario" and an economic stabilization from record low levels of activity. They are two completely separate events.

So Far this AM...

In overnight trading: SHANGHAI +1.91%, HANG SENG -0.38%, NIKKEI +0.75%, TOPIX +1.36%, CAC -1.37%, DAX -1.50%, FTSE -1.28%

US Treasuries fared well in overseas trading last night. In STRONG volume the long end of the yield curve rallied, pushing 10s down to the ALL IMPORTANT 3.75% pivot point. This is largely an extension of yesterday's rally...

Many reasons can be cited for the large overnight swing in yields. Japan returned to work to find a record steep 2s/10s yield curve, bargain buying boosted the TSY bid which was obvious out the gate last night thanks to a weaker than expected start to the earnings season. Alcoa reported a net loss of $277 million. On top of that Chevron warned that Q4 earnings would be "sharply lower" thanks to deterioration of refining margins. Furthering the bid in the TSY market was speculation on the fate of Greece. The IMF will be making a visit to Athens to help the government devise a likely bail out plan...Greece says they just need help creating a new tax system, the market says "I dont care" we're assuming the worst. Also helping out the US Treasury market was news that China increased bank reserve requirements ,after the PBOC pushed their 1yr T-bill rate higher...call it a pre-emptive hint of a pending INTEREST RATE HIKE aka FEARS OF INFLATION in China.

Overall the market's landscape was heavily in favor of a flight to quality last night. This morning there hasn't been much data to sway that sentiment.

The National Federation of Independent Businesses (NFIB) this morning released their latest monthly survey on small business optimism. This release has become more and more influential in the market as small businesses are the main driver of hiring in the US. The NFIB index fell 0.3 points in December to 88. That’s up from the lows of March 2009, but has been below 90 for 15 months. “Optimism has clearly stalled in spite of the improvements in the economy,” the NFIB said. “Continued weak sales and threatening domestic policies from Washington, have left small business owners with little to be optimistic about in the coming year.”

Basically what I take from this is that small businesses SEE NO REASON TO HIRE NEW LABOR

All this does is fuel our bias that the economy is really not recovery as much as it has stabilized from record low levels of activity. Makes you think a little harder about the above discussed 1,200 ceiling in stocks doesnt it?

I suppose I should also comment on 830 data: the TRADE DEFICIT

The US Trade Deficit rose 9.7% in November to $36.4 billion. Imports rose 2.6%. Exports were up only 0.9%. I could care less about this at the moment...market's feel the same way. READ MORE if youre interested.

So...again I say that there has been little news/data to slow the extension of yesterday's rally. Check out the progress made in 10s. The 3.375 coupon bearing 10yr TSY note is trading +0-23 at 97-03 yielding 3.728%. 3.75% HAS BEEN BROKEN

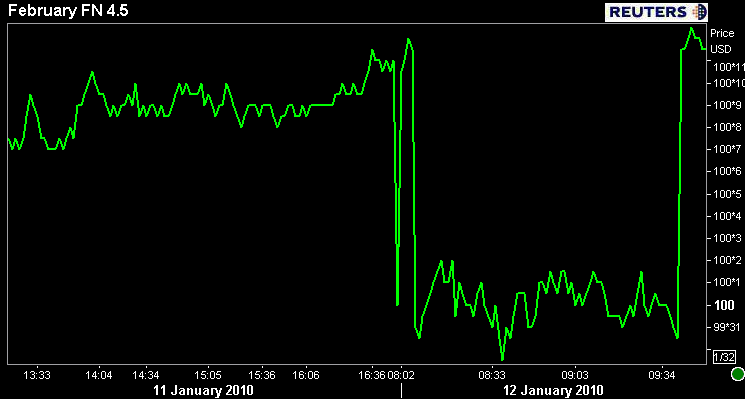

Mortgage prices are rallying too. The FN 4.5 is currently +0-13 at 100-14. I would like to show you a chart but Reuters rolled one month too far last night. They are only showing me the FN 4.5 March coupon...which is at 100-01. We already made the call to have it fixed. Will post MBS charts ASAP.

UPDATED AT 9:50am..."THE DROP" has been recovered already!

Rate sheets will be improved this morning...BUT

THIS IS VERY IMPORTANT:

I am taking profits ahead of the looming auction cycle...we still have $74billion in TSY notes to be auctioned. I am however feeling like my strategy to BUY after the auctions is becoming more and more likely. There has been a noticeable consolidation around 3.80% and 3.82% indicating the market likes these higher yields and may be looking to do some bargain buying. Supporting that theory is the JP Morgan Investor survey which indicates investors reduced SHORT positions and increased LONGS last week. While short positions were near a two year high, this is still supportive of at least an attempt of a recovery rally later in the week.

If we can get some volume behind that relief rally we would see some improved mortgage pricing over the next 10 days. Unfortunately, looking further down the road....I am not yet willing to change my outlook for higher yields by the end of Q1 2010.

PS. I am feeling the flow today!