We're back to and maybe even setting new year-to-date mortgage rate lows right now.

These positive developments follow a short period of stagnation where volatility in the secondary mortgage market kept us on edge, but never really amounted to much on rate sheets. Loan pricing drifted mostly sideways since setting new YTD lows on June 8th. And even though we didn't have far to travel, we're back to those lows again. And maybe even teetering on lower lows....

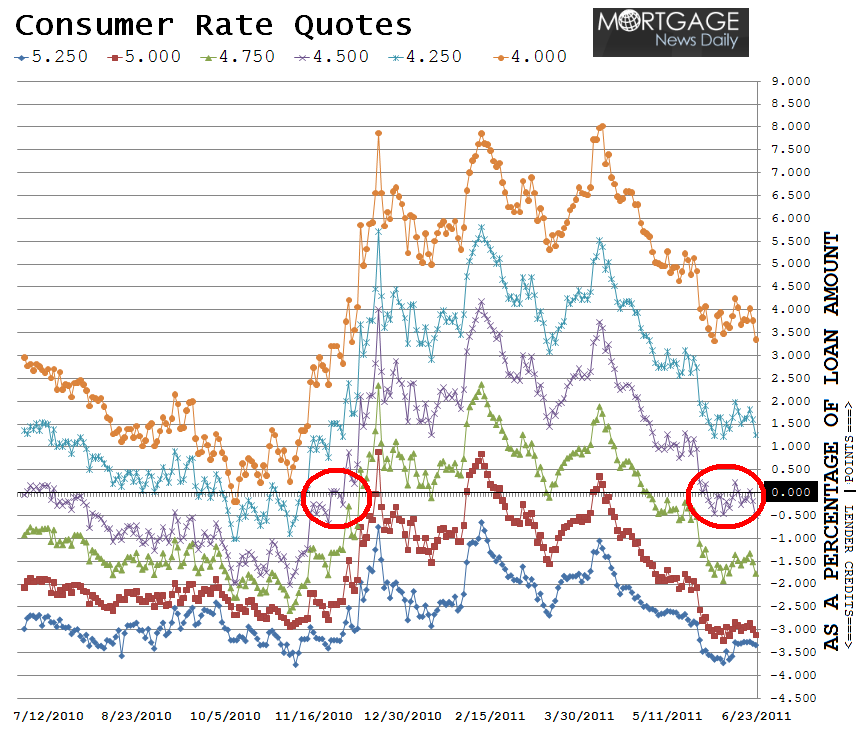

In the chart of Consumer Rate Quotes below, if the line is moving up, closing costs are rising. If the line is moving lower, costs are getting cheaper. Sideways mortgage rate behavior followed by an abrupt drop followed by another spell of mostly sideways activity can be seen when looking closely. This spell of sideways activity has taken place near the most aggressive rate quotes of the year. Today is just as good a day as June 8th to lock. That is unless you're waiting for 4.25% (still).

See the RED CIRCLES.BEST LEVELS SINCE THE MIDDLE OF NOVEMBER.

The chart above compares the average origination costs (as a percentage of loan amount) for several available mortgage note rates as quoted by the five major lenders. Each line represents a different 30 year fixed mortgage note rate. The numbers on the right vertical axis are the origination closing costs, as a percentage of your loan amount, that a borrower would be required to pay in order to close on that note rate. If the note rate graph line is below the 0.00% marker, the consumer may potentially receive closing cost help from their lender in the form of a lender credits. If the note rate line is above the 0.00% marker, the consumer should expect to pay additional points at the closing table to cover permanent buydown costs and origination fees. PLEASE SEE OUR MORTGAGE RATE DISCLAIMER BELOW

CURRENT MARKET: The "Best Execution" conventional 30-year fixed mortgage rate is 4.50%. Some lenders may be quoting 4.375%, but that offer is aggressive and will likely carry increased closing costs in the form of origination fees. These costs could be worth it to applicants who plan to keep their new mortgage outstanding for long enough to breakeven on the extra upfront costs. On FHA/VA 30 year fixed "Best Execution" is 4.25%. 15 year fixed conventional loans are best priced at 3.75%. Five year ARMs are best priced at 3.125% but the ARM market is more stratified and there is more variation in what will be "Best-Execution" depending on your individual scenario.

PREVIOUS GUIDANCE: As volatility continues in the secondary market, it's becoming apparent that lenders are pricing loans from a defensive stance. Lenders are waiting for the secondary market to commit to a directional trend. With today's high-risk event over, it might seem safer to float if lenders are pricing defensively by default. And in fact, if you're able to act quickly and are somewhat flexible with respect to the risk of slightly higher closing costs, that can be a valid strategy here, but floating is best reserved for the longer term and most flexible scenarios here. While there is potential upside even for short term outlooks, it's not likely to ratchet the Best-Execution rate down another 1/8th of a percent quickly enough to be worth the risk.

CURRENT GUIDANCE: This is as good as it's been all year. Since the middle of November really. If you're on a short lock/float timeline (15 days), now is a good time to considering locking. While a few sessions of continued loan pricing rallies could lead to a lower overall note rate offer, we've been here before (recently) and failed to see investors commit to a sustained rally in the bond market. Our long-term outlook still supports the case for lower rates though, however until we see investors display a commitment to rally, we will be reluctant to advise floating in the short-term, especially with volatility only 2-days behind us.

A PEEK AT THE WEEK AHEAD: The week begins at a brisk pace with Personal Income and Spending right off the bat at 830 on Monday morning Soon after we'll be preparing for the week's Treasury auction cycle, starting early this time with $35bn 2s at 1pm. 5’s and 7’s arrive in a similarly early fashion, on Tuesday and Wednesday. While the auction cycle will certainly be one of the week’s focal points, there’s an interesting twist to the calendar of events ahead.... Thursday is the last day of the month, the quarter, the half, and of QE2. Adding a few layers of complexity to that situation will be a diverse line-up of Fed Speakers not to mention the ongoing potential for tapebomb news headlines. Otherwise there’s nothing earth-shattering on the data docket, we get Consumer Confidence, Pending Home Sales, Chicago PMI, Consumer Sentiment and the ISM Manufacturing Index, just to name a few. We look most forward to seeing Consumer Confidence and ISM as these are early indicators of June data to come. Regarding the markets, investors haven't been displaying much directional commitment lately. With benchmark 10-year yields rallying to new YTD lows today (which mortgages did not keep up with), we'll be looking for a confirmation rally early and often next week.

What MUST be considered BEFORE one thinks about capitalizing on a rates rally?

1. WHAT DO YOU NEED? Rates might not rally as much as you

want/need.

2. WHEN DO YOU NEED IT BY? Rates might not rally as fast as you

want/need.

3. HOW DO YOU HANDLE STRESS? Are you ready to make tough

decisions?

----------------------------

"Best Execution" is the most cost efficient combination of

note rate offered and points paid at closing. This note rate is determined

based on the time it takes to recover the points you paid at closing (discount)

vs. the monthly savings of permanently buying down your mortgage rate by

0.125%. When deciding on whether or not to pay points, the borrower must

have an idea of how long they intend to keep their mortgage. For more info, ask

you originator to explain the findings of their "breakeven analysis"

on your permanent rate buy down costs.

Important Mortgage Rate Disclaimer: The "Best Execution" loan

pricing quotes shared above are generally seen as the more aggressive side of

the primary mortgage market. Loan originators will only be able to offer these

rates on conforming loan amounts to very well-qualified borrowers who have a

middle FICO score over 740 and enough equity in their home to qualify for a

refinance or a large enough savings to cover their down payment and closing

costs. If the terms of your loan trigger any risk-based loan level pricing

adjustments (LLPAs), your rate quote will be higher. If you do not fall into

the "perfect borrower" category, make sure you ask your loan

originator for an explanation of the characteristics that make your loan more

expensive. "No point" loan doesn't mean "no cost" loan. The

best 30 year fixed conventional/FHA/VA mortgage rates still include closing

costs such as: third party fees + title charges + transfer and recording. Don't

forget the fiscal frisking that comes along with the underwriting process