It was a volatile week for mortgage rates.

Monday and Tuesday saw rates near their best levels in nearly a month. Consumer borrowing costs then got beat up on Wednesday and Thursday, so much that we had to up the "Best Execution" 30-year fixed mortgage rate to 5.000%. That's where we last left you, just ahead of today's high risk event: The Employment Situation Report

CURRENT MARKET: The "Best Execution" conventional 30 year fixed mortgage rate has fallen BACK to 4.875%. For those looking to buy down their rate to 4.75%, this quote carries higher closing costs. The upfront cost of permanently buying down your rate to 4.75% is not worth it to many applicants. We would generally only advise the permanent floatdown if you plan to hold your new mortgage for longer than the next 10 years. Ask your loan officer to run a breakeven analysis on any origination points they might require to cover permanent float down fees. On FHA/VA 30 year fixed "Best Execution" is still 4.75%. 15 year fixed conventional loans are best priced between 4.125% and 4.25%, but 4.25% is more efficient in terms of the floatdown breakeven cost. Five year ARMS are best priced at 3.625%.

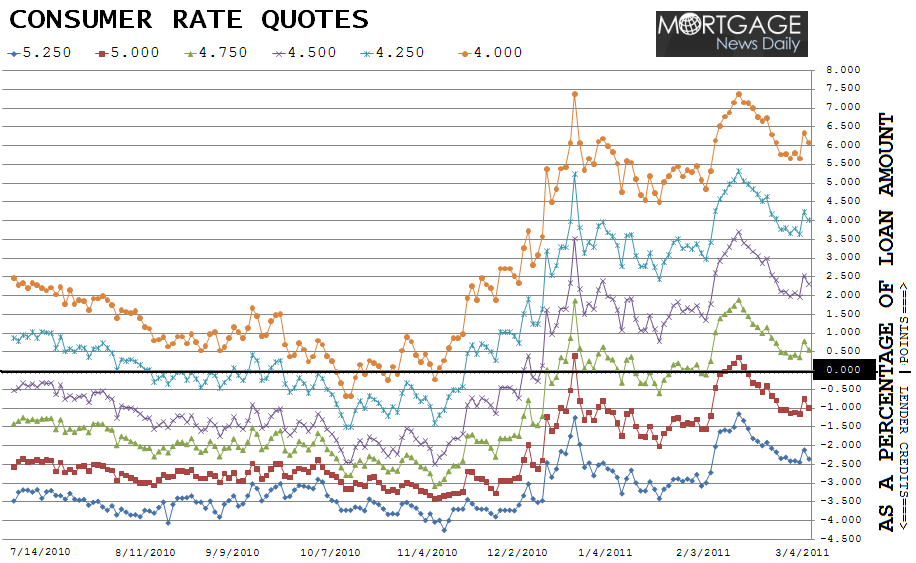

To illustrate the recent behavior of mortgage rates, we offer the chart below. It graphs the average origination closing costs associated with specific mortgage note rates as quoted by the five major mortgage lenders.

If the note rate line is moving up, the closing costs associated with that rate quote are rising. In December, closing costs rose rapidly. Mortgage rates did improve from those levels, but then moved sideways for 7-weeks. And then the range broke following the January Employment Situation Report and consumer rate quotes rose back to their December highs. As you can tell, borrowing costs have steadily improved since then but moved sharply higher this week before correcting today. This leaves home loan rate quotes just above one-month lows. Again.

Each line represents a different 30 year fixed mortgage note rate. The numbers on the right vertical axis are the origination closing costs, as a percentage of your loan amount, that a borrower would be required to pay in order to close on that note rate. If the note rate graph line is below the 0.00% marker, the consumer may potentially receive closing cost help from their lender in the form of a lender credits. If the note rate line is above the 0.00% marker, the consumer should expect to pay additional points at the closing table to cover permanent buydown costs and origination fees. PLEASE SEE OUR MORTGAGE RATE DISCLAIMER BELOW

OUR GUIDANCE LAST FRIDAY: The bond market is still in limbo in terms of an extension of the recent rally. Approach floating from a defensive posture, especially after Best Execution improved to 4.875% this week because it's going to take a sustained rally in the bond market before Best Execution reaches 4.75%. That means current market is likely as good as it gets for at least the next week. If you don't have more than a week to float your loan, you should be locking very soon. As you can see in the chart above, it's been almost a month since rates were this aggressive. And we wouldn't be surprised one bit if the market pushes back against the recent mortgage rates rally next week. Profit taking is a naturally occurring event whenever interest rates move lower.

NEW GUIDANCE: Phew! We dodged a bullet today. The conventional 30-year fixed Best Execution note rate has fallen to 4.875%. Consumer borrowing costs have almost recovered fulLy from the mid-week hiccup we experienced on Wednesday and Thursday. There is still work to done, but after reprices for the better were awarded today by lenders, we're just above one-month lows. BEYOND THAT...same exact guidance as last Friday!

READ MORE: LOAN PRICING STALLED

"Best Execution" is the most efficient combination of note

rate offered and points paid at closing. This note rate is determined based on

the time it takes to recover the points you paid at closing (discount) vs. the

monthly savings of permanently buying down your mortgage rate by 0.125%.

When deciding on whether or not to pay points, the borrower must have an idea

of how long they intend to keep their mortgage. For more info, ask you originator

to explain the findings of their "breakeven analysis" on your

permanent rate buydown costs.

Important Mortgage Rate Disclaimer: The "Best Execution" loan

pricing quotes shared above are generally seen as the more aggressive side of

the primary mortgage market. Loan originators will only be able to offer these

rates on conforming loan amounts to very well-qualified borrowers who have a

middle FICO score over 740 and enough equity in their home to qualify for a

refinance or a large enough savings to cover their down payment and closing

costs. If the terms of your loan trigger any risk-based loan level pricing

adjustments (LLPAs), your rate quote will be higher. If you do not fall into

the "perfect borrower" category, make sure you ask your loan originator

for an explanation of the characteristics that make your loan more expensive.

"No point" loan doesn't mean "no cost" loan. The best 30

year fixed conventional/FHA/VA mortgage rates still include closing costs such

as: third party fees + title charges + transfer and recording. Don't forget the

intense fiscal frisking that comes along with the underwriting process

HERE is a full recap of the Employment Situation Report