The word of the month in the primary mortgage market is "RANGE". <<<---- We wrote that last Friday.

On Monday we said a storm was a brewin. "Don't get complacent".

Tuesday we took off because nothing happened on TuesDAY. TuesNIGHT was when the action was expected.

Nope. TuesNIGHT came and went with little action to report. Wednesday too.

So on Thursday we were back to preaching the principles of "THE RANGE". And then came Friday.........................

To sum up what you want to hear in one easy to understand statement, I quote Chris Kopec of Owl Tree Mortgage - "MBS out on the highs of the day....likey likey"

Well-said Chris. Well said. Even those who know nothing of MBS can figure out what happened in the mortgage market today. "Likey likey" says it all.

MG's gut instincts were spot on yesterday. It was worth an overnight float if you had the time and the stomach.

A flight to safety played out in the bond market today as stocks sold off. This put an end to an 8-week win streak for stocks and pushed benchmark interest rates lower which helped MBS prices, as Chris mentioned above, close at their highest levels of the day and allowed lenders to "reprice for the better".

To remind readers, a flight to safety happens when investors are nervous about owning risky assets like stocks, but do not want to miss out on earning a return on their funds, so they allocate their money into risk-free government guaranteed U.S Treasury debt to provide a safe-haven AND an investment return. As benchmark Treasury yields fall on "flight to safety" buyer demand, prices of mortgage-backed securities move higher in unison. This allows lenders to reprice their rate sheets for the better and gives originators an opportunity to offer fence-sitting borrowers lower mortgage rates or more competitive closing costs.

Anyway.....

On conventional 30 year fixed loans Best Execution is now split between 4.75% and 4.875%. Reports of 4.75% quotes are not widespread though. They are actually quite scattered. The permanent buydown cost from 4.875 to 4.75% is still expensive, but your lender will likely compensate you for those additional costs by providing some sort of closing cost help via lender credit. Again, these quotes are very scattered and vary greatly from lender to lender, but 4.75% is on the board for a few lucky fence-sitters. The same can be said about FHA/VA 30 year fixed loans, Best Execution is split between 4.75 and 4.625% though. If you're shopping for a 15 year fixed mortgage rate, we see a sweet spot between 4.125% and 4.25%. On 5-year ARMs, we've heard of very well qualified borrowers being quoted rates as low as 3.50%.

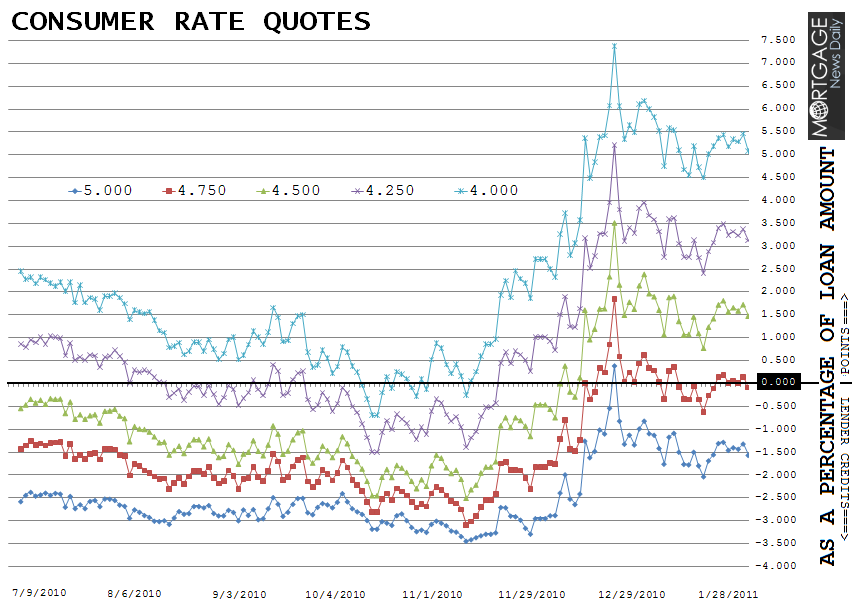

To illustrate the recent behavior of mortgage rates, we offer this chart which graphs the average note rate costs offered by the five major mortgage lenders.

Each line is a different 30 year fixed mortgage note rate. The numbers on the right vertical axis are the origination closing costs, as a percentage of your loan amount, that a borrower would be required to pay in order to close on that note rate. If the note rate graph line is below the 0.00% marker, the consumer may potentially receive closing cost help from their lender in the form of a lender credits. If the note rate line is above the 0.00% marker, the consumer should expect to pay additional points at the closing table to cover permanent buydown costs and origination fees. SEE OUR MORTGAGE RATE DISCLAIMERS AND OTHER ASTERISKS BELOW.

Plain and Simple: If the note rate line is moving up, the closing costs associated with that quote are rising. In December, closing costs rose rapidly which significantly altered the mortgage rate market. Mortgage rates have since improved from those levels. The best opportunity to lock over the past month was on January 14th. Closing costs are currently higher than those levels, but we're currently sitting at week-over-week lows.

DECISION TIME....

The motivation behind the above discussed "flight to safety" is mixed. So our encouragement level is mixed as a result. The decision really depends on your timeline: Are you a short-timer, a medium-term opportunist, or a "ho-hum 4.00%er"????

For a short-timer day to day risks are still manageable. But we caution you. We're not far from the best levels of the month. If you need to lock your loan soon, this is an opportunity. We are GUARDED/DEFENSIVE about your position. But encouraged.

For the medium-term rate watcher, your situation is similar to the short-timer. This is an opportunity. But you've got more time and we're feeling more encouraged about the prospects for lower rates in the next 15-20 days. Sit tight for now, but remain very cautious. We have some cushion to work with....let's see how this plays out on a day-to-day basis. (The range is still the range until the range is no more.)

For the "ho-hum 4.00%ers"...There is much work to be done in the bond market before we can even talk to you again. The 4.00% note rate is currently costing 5 points. Stay hopeful and enjoy the ride.

WHAT WE NEED NEXT WEEK: A STOCK MARKET SELL OFF AND MORE FLIGHT TO SAFETY

"Bext Execution" is the most efficient combination of note rate and

points paid at closing. This note rate is determined based on the time

it takes to recover the points you paid at closing (discount) vs. the

monthly savings of permanently buying down your mortgage rate by

0.125%. When deciding on whether or not to pay points, the borrower

must have an idea of how long they intend to keep their mortgage. For

more info, ask you originator to explain the findings of their

"breakeven analysis" on your permanent rate buydown costs.

Important Mortgage Rate Disclaimer: Loan originators will only be able

to offer these rates on conforming loan amounts to very well-qualified

borrowers who have a middle FICO score over 740 and enough equity in

their home to qualify for a refinance or a large enough savings to cover

their down payment and closing costs. If the terms of your loan trigger

any risk-based loan level pricing adjustments (LLPAs), your rate quote

will be higher. If you do not fall into the "perfect borrower" category,

make sure you ask your loan originator for an explanation of the

characteristics that make your loan more expensive. "No point" loan

doesn't mean "no cost" loan. The best 30 year fixed conventional/FHA/VA

mortgage rates still include closing costs such as: third party fees +

title charges + transfer and recording. Don't forget the intense fiscal

frisking that comes along with the underwriting process.

MORE EXPLANATION ON THE GRAPH: As an example, 4.00% note rates would cost a borrower 5.00

discount/origination points at the closing table, as a percentage of

their loan amount. This is clearly not advisable nor is it attainable. A

more relevant example is the 4.75% note rate. 4.75%

is very close to the 0.00% line. If you do recieve a lender credit on that note rate, it is only because you were asked to pay an origination fee.