On this final day of a holiday-shortened work week we find ourselves facing a jam packed macroeconomic data calendar. Just over an hour before the first report prints, stock futures are off their overnight highs as equity investors pause to reflect on pushing stocks past two-year highs. Meanwhile in the bond market, the 10-year note is creeping outside the upper limit of AQ&MG's 3.27 to 3.36/37% range.

S&P 500 futures are 2 points lower at 1,252.50 and Dow futures are 3 points lower at 11,492. The S&P has climbed in each of the five past trading days, having moved up 6.63% since Dec. 1.

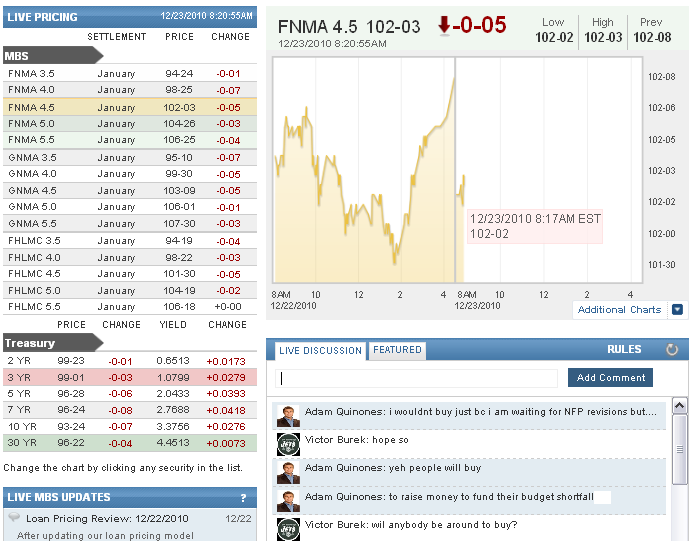

The benchmark 10-year Treasury note is -7/32 at 93-21 yielding 3.376%. The FNCL 4.5 has opened 5/32 lower at 102-03.

Light crude oil is down 0.10% at $90.40 per barrel while gold prices are off 0.47% at $1,378.

Key Events Today:

8:30 ― Durable Goods Orders are expected to fall 0.4% in November, subtracting from the -3.4% print a month before. Expectations range widely, from -3.6% to +3%. One reason for the expected decline is a sharp drop in Boeing aircraft orders. Excluding transportation, orders are forecast to be up 1.6%, compared with a 2.7% drop the month before. Core durable goods ― non-defense orders excluding aircraft ― should rise 2.5% in the month after a 4.3% cutback in October.

“Non-defense aircraft and parts has been either feast or famine for the past two years, and September and October were feasts and November was a famine,” said economists at IHS Global Insight. “Aircraft orders should slump from about $13 billion per month in September and October, as November comes up short at about $5.5 billion. Even the rebound in machinery orders after a dismal October, which should push core capital goods orders up 5.0%, and a rebound in defense bookings can't offset the downdraft in aviation on the total.”

8:30 ― The Personal Incomes & Outlays report is anticipated to show incomes rising slowly and consumption rising a bit more rapidly amid mild inflation. Income is forecast to rise 0.2% in November, adding to the 0.5% gain a month before. Consumption is set to move up 0.5% after a 0.4% gain. Core inflation ― the Fed’s preferred measure ― is anticipated to rise 0.1% in the month after a flat reading in October, which would leave the annual rate at just +0.9%, far below the optimal 2% pace.

“U.S. retail sales in November increased by 0.8% and reached a level of 7.7% above its November 2009 level,” noted economists at BBVA. “Total sales in the last three months jumped 7.8% from the same period a year ago. Retail sales excluding autos also increased by 1.2%, above expectations of a 0.6% increase. ... Therefore, we expect personal income and spending to continue increasing in November.”

“Overall,” added economists from IHS Global Insight, “real consumer spending is heading for a 3.5% increase in the fourth quarter; significantly higher than the third quarter's 2.8%, which was the strongest since late 2006 in seasonally adjusted annual rate (SAAR) terms.”

8:30 ― The four-week average of Initial Jobless Claims has declined for six consecutive weeks and currently stands at just 422,750 ― the lowest since early August 2008). For the week ending Dec. 18, economists are anticipating 420k claims, the same figure as the prior week.

“This continued fall signals a gradually improving labor market,” said economists at Nomura. “Because this week's report will reflect job conditions during the 12 December reference week for the official employment report, another low reading on initial claims could raise market expectations for December nonfarm payrolls.”

Economists at BBVA pointed out that initial claims remain higher than pre-recession levels, however, suggesting the recovery remains slow.

9:55 ― Holiday spirit isn’t expected to have much impact on Consumer Sentiment in December. The Reuters / U of Michigan index is anticipated to rise six-tenths from the preliminary reading to 74.8, with expectations ranging from 73 to 77. The preliminary index did, however, advance 2.6 points to the highest level since June. The economic conditions component increased to 85.7, while the economic outlook component moved up to 66.8.

Economists at IHS Global Insight said the preliminary reading was “good news for retailers, since an increase in consumer optimism translates into relatively good news for holiday sales.” They predicted that holiday retail sales would be up 4.5% compared to last year.

“Gains in household net worth due to the rising stock market and relatively good news on the employment front should drive the recent momentum in consumer sentiment slightly higher, despite higher gasoline prices and a poor housing market,” they added.

10:00 ― New Home Sales nosedived 8.1% to an annualized pace of 283k sales in November ― the second lowest figure on records dating back to 1963. The unexpected fall came after two increases and was further hurt by downward revisions to the prior three months of data. For November, economists look for an increase to 300k, a pace well below the historical average of 697k, according to BBVA.

“Considering current inventories in the housing markets, we expect new home sales remain weak even in 2011,” they added.

Other economists point to improvements based on November’s increase in single-family housing permits, an improving job market, and a pick-up in MBA’s index of mortgage purchase applications.

SIFMA recommends a 2pm close for the bond market.