Final Q3 GDP data is out.

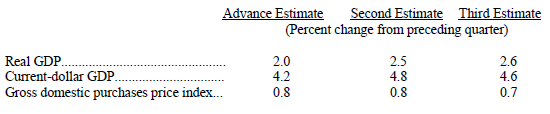

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 2.6 percent in the third quarter of 2010, (that is, from the second quarter to the third quarter), according to the "third" estimate released by the Bureau of Economic Analysis.

In the second quarter, real GDP increased 1.7 percent. The GDP estimate released today is based on more complete source data than were available for the "second" estimate issued last month. The "third" estimate of the third-quarter increase in real GDP is 0.1 percentage point, or $1.1 billion, higher than the "second" estimate issued last month, primarily reflecting an upward revision to private inventory investment that was largely offset by a downward revision to personal consumption expenditures.

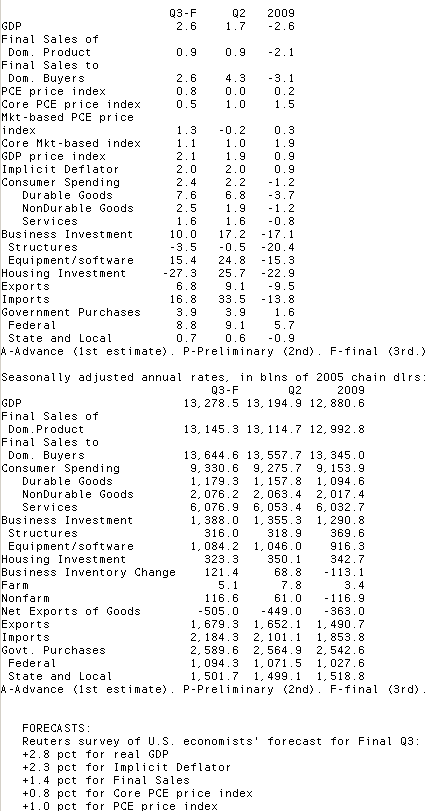

The increase in real GDP in the third quarter primarily reflected positive contributions from personal consumption expenditures, private inventory investment, nonresidential fixed investment, exports, and federal government spending that were partly offset by a negative contribution from residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The acceleration in real GDP in the third quarter primarily reflected a sharp deceleration in imports and an acceleration in private inventory investment that were partly offset by a downturn in residential fixed investment and decelerations in nonresidential fixed investment and in exports. Motor vehicle output added 0.49 percentage point to the third-quarter change in real GDP after subtracting 0.06 percentage point from the second-quarter change. Final sales of computers added 0.29 percentage point to the third-quarter change in real GDP after adding 0.03 percentage point to the second-quarter change.

Reuters Quick Recap...

RTRS-US FINAL Q3 GDP +2.6 PCT (CONSENSUS +2.8 PCT), PREV +2.5 PCT; FINAL SALES +0.9 PCT (CONS +1.4 PCT), PREV +1.2 PCT

RTRS-US FINAL Q3 GDP DEFLATOR +2.0 PCT (CONS +2.3 PCT), PREV +2.2 PCT

RTRS-US Q3 PCE PRICE INDEX +0.8 PCT (CONS +1.0 PCT), PREV +1.0 PCT; CORE PCE +0.5 PCT (CONS +0.8 PCT), PREV +0.8 PCT

RTRS-US Q3 CONSUMER SPENDING +2.4 PCT (PREV +2.8 PCT), DURABLES +7.6 PCT (PREV +7.4 PCT)

RTRS-US Q3 MARKET-BASED PCE PRICE INDEX +1.3 PCT (PREV +1.3 PCT), CORE +1.1 PCT (PREV +1.1 PCT)

RTRS-US Q3 BUSINESS INVESTMENT +10.0 PCT (PREV +10.3 PCT), EQUIPMENT/SOFTWARE +15.4 PCT (PREV +16.8 PCT)

RTRS-US Q3 HOME INVESTMENT -27.3 PCT (PREV -27.5 PCT), BUS. INVESTMENT IN STRUCTURES -3.5 PCT (PREV -5.7 PCT)

RTRS-US Q3 EXPORTS +6.8 PCT (PREV +6.3 PCT), IMPORTS +16.8 PCT (PREV +16.8 PCT)

RTRS-US Q3 GDP EX MOTOR VEHICLES +2.1 PCT (PREV +2.0 PCT)

RTRS-US Q3 YEAR-ON-YEAR PCE PRICE INDEX +1.4 PCT (PREV +1.4 PCT), CORE PCE +1.2 PCT (PREV +1.3 PCT)

RTRS-US Q3 BUSINESS INVENTORY CHANGE +$121.4 BLN (PREV +$111.5 BLN)

RTRS-US Q3 BUSINESS INVENTORY CHANGE ADDS 1.61 PERCENTAGE POINT TO GDP CHANGE

RTRS-US Q3 CORE PCE +0.5 PCT RISE SMALLEST SINCE RECORDS BEGAN IN 1959

The change in real private inventories added 1.61 percentage points to the third-quarter change in real GDP, after adding 0.82 percentage point to the second-quarter change. We've already noted that an increase in inventories is a good thing if it is a function of consumers spending more money. But consumer spending was revised lower from +2.8% to +2.4% (vs. the advance read of +2.6%), indicating businesses might be building up inventories a bit too fast. That could come back to bite GDP growth in the quarters ahead unless consumer spending ramps up enough to encourage a continued uptick in inventory growth.

The Fed's preferred gauge of inflation, the Core PCE Price index fell from +1.2% in the 1st quarter to +1.0% in the 2nd quarter to a record low QoQ rate of +0.5% in the 3rd quarter. We're seeing inflation in food prices, energy, education costs, and health care....but those are the sectors of our economy that are seeing the most demand (necessities). Home prices haven't hit a floor, wage growth is anemic, and there is much slack in resource utilization. This does not bode well for businesses who are trying to pass along higher input costs to bargain hunting consumers.

Business investment continues to improve though.I wrote this in March....

One of the categories I believe will help lead aggregate demand from anemic levels is Business Investments. Firms will look to reduce costs by increasing productivity and efficiency via investments in new technology (scary outlook for the labor market!).

Although business investment was marked lower vs. the preliminary read, it still grew by 10% in the 3rd quarter led by a 15% increase in equipment and software upgrades. See comments above re: technology increasing productivity. Again...these investments reduce the need for humans on the assembly line. America is a service based economy now---we must train our youth to handle technology because robots (automation) are taking over the non-specialized assembly line positions.

Re: Housing Investment. It was revised for the worse to a putrid 27.3% QoQ decline (following the expiration of the home buyer tax credit)

Market Reaction...