Argh. I hate when I write a strong post and the market moves immediately after I publish it.

The New York Fed's trading desk was in the market for Treasuries this morning, buying $7.79bn in rate sheet influential benchmarks maturing between 02/15/2018 and 11/15/2020. As a result, with the calendar lite and momentum leaning in favor of the bond bulls, longer dated TSYs rallied and the curve flattened out the gate all the way into the Fed's 10:15 POMO. However once the Fed's open market operations were done for the day...we started seeing rates make a move higher along with with a modest increase in trading volume and a positive uptick in trading flows. This is indicative of new money entering the market via SHORT SELLING followed by profit taking on pre-POMO positions.

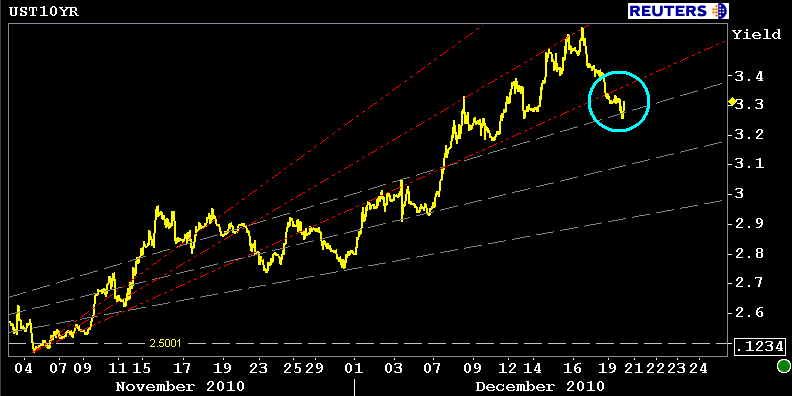

OTR 10s ventured as low as 3.25% before running right into resistance at my long term 38% fibonacci fan. 10s are currently bid +7/32 at 94-08 yielding 3.309%. This seems bad but the March 10yr TSY futures contract has found support near the overnight lows at 120-10. A break of this support level would suggest 10s are gonna retest the 3.36 area.

Consequently, production MBS coupon prices have fallen from intraday highs. The FNCL 4.5 is +5/32 at 102-05. We're 10 ticks off the intraday high...thus some lenders may reprice for the worse.

Again, liquidity is greatly lacking and the possibility for chopatility remains high. This means little to lenders though...a 10/32 price dip from the morning highs is more than enough to warrant a rebate recall.