Treasury just auctioned $21 billion reopened 2.625 coupon bearing 10 year notes.

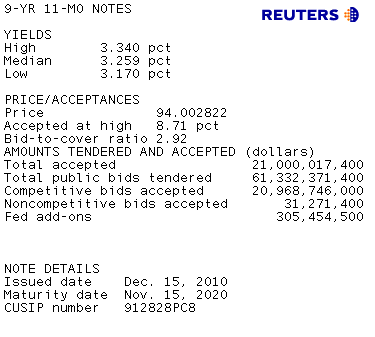

The bid to cover ratio, a measure of auction demand, was 2.92 bids submitted for every 1 accepted by Treasury. This is below both the five and ten auction averages (3.03 & 3.12) which is indicative of apathetic demand.

The high yield was 3.34% but only 8.71% of the issue was allotted there. The 1pm WI yield was 3.333%, so this auction tailed by less than a bp which implies buyers forced Treasury to lower their offer prices. It should be noted that the "on the run" 10yr note yield and the WI both moved sharply higher into the 1pm auction stop. This illustrates the market's pre-auction concessionary efforts.The fact that we still tailed implies investors did their best to make Treasury come to their declining bids.

Primary dealers added $9.3 billion in 10yr note inventory. This represents 44% of the competitive bid which is a slightly above average award for the street but not terrible when you consider the defensive year-end bias that currently moderates the market. We were prepared for the possibility that dealers were gonna have to do much more heavy lifting than they did, it's a big positive that other accounts participated.

Direct bidders, which include bond fund managers like PIMCO and Vanguard, were awarded a six auction high 11.4% of the competitive bid, or $2.4 billion.

At 44.4%, indirect demand, largely seen as a gauge of overseas investor bidding, was considerably quieter than the November refunding as well as below the five auction average, but did not dip below the ten auction average of 43.4%. Indirect bidders were also somewhat more aggressive on what they bid with an above average 75.4% hit rate, but we can attach an asterisk to that as they only bid on $12.3 billion in 10s (lowest since January). Overall, indirect activity was well-within the range of their recent 10yr note auction participation.

Plain and Simple: the market clearly tried its hardest to price in a supply concession before the 1pm stop, but buyer demand metrics were not dissappointing. Average auction, no reason to believe the world is exiting their U.S. debt positions in size.

Market Reaction...

We're seeing modest improvements in the aftermath of the auction, mostly led by the futures market. I would say this is more short covering than outright demand but today's selloff seems to have been greatly exaggerated by supply concession attempts and a lack of willing buyers....so it wouldn't be surprising to see some bargain buying real$ types nibbling at the price lows/yield highs. We gotta start somewhere!

10yr yields were priced at 3.315% just before the auction results were released, since then they've fallen 5bps to 3.265%. The 2s/10s yield curve has flattened 4bps from 269 wide to 265. And the January delivery FNCL 4.5 has risen from 101-26 to 101-31.The FNCL 4.0 has risen from 98-19 to 98-29. This price jump may give lenders enough incentive to reprice for the better but I am not holding my breath unless the rebound picks up some steam. Hope for the best but prepare for it to get worse....

MG is working on charts.