In the absence of new domestic data, the Fed's fifteenth QEII open market operation has been the primary force behind price action in the government bond market so far today. Fast$ day traders are playing an active role in directionality as well as below average trading volumes and a general lack of liquidity (spotty two-way flows).

The move lower in yields was sparked last night by Benny B's prime time appearance on 60 Minutes. Just in case you missed it here is a quick recap of Bernanke's comments....

- 05Dec10 -FED'S BERNANKE ON CBS' 60 MINUTES: "CERTAINLY POSSIBLE" FED COULD BUY MORE THAN $600 BLN IN ASSETS, DEPENDS ON PROGRAM'S EFFICACY, INFLATION, ECONOMY

- 05Dec10 -BERNANKE SAYS "VERY CLOSE TO THE BORDER" ON WHETHER RECOVERY SELF-SUSTAINING, DOUBLE-DIP RECESSION NOT LIKELY

- 05Dec10 -BERNANKE SAYS COULD TAKE 4 TO 5 YEARS BEFORE WE ARE BACK TO MORE "NORMAL" JOBLESS RATE AROUND 5-6 PCT

- 05Dec10 -BERNANKE SAYS JOBLESS RATE "JUST NOT GOING DOWN," ADDING: "THAT'S A MAJOR CONCERN"

- 05Dec10 -BERNANKE SAYS THAT, BECAUSE THE FED IS ACTING, DEFLATION RISK IS PRETTY LOW

- 05Dec10 -BERNANKE SAYS IF FED HAD NOT ACTED, DEFLATION WOULD BE A MORE SERIOUS CONCERN

- 05Dec10 -BERNANKE SAYS FEAR OF INFLATION DUE TO FED'S ACCOMMODATIVE MONETARY POLICY IS "WAY OVERSTATED"

- 05Dec10 -BERNANKE SAYS IDEA THAT FED "PRINTING MONEY" IS A MYTH, MONEY SUPPLY NOT CHANGING SIGNIFICANTLY

- 05Dec10 -BERNANKE: TO KEEP INFLATION AT BAY MUST FIND RIGHT TIME TO UNWIND POLICY, "AND THAT'S

Asian markets reacted almost instantaneously to the Fed Chairman's dovish outlook with a 4bp rally in benchmark 10yr note yields down to 2.96% (ooo big rally! note sarcasm). After that 10 yr yields slowly meandered lower into the London open where levels held steady in the mid 2.90s until the Fed's QEII POMO, which began at 10:15am and ended at 11am. Since then positive progress has backed up a bit as profits are booked on fast$ positions and preparations are made for the $66 billion in Treasury coupon supply that will be offered over the next three days.

Plain and Simple: This behavior shines a spotlight on the tactical nature of current bond investing biases. With year end looming and portfolio managers playing catch up vs. equities, we remain defensive of any rate rallies. If we do see bonds yields rally into year-end, the move lower will be choppy as we do not expect traders to leave profits on the table for too long.

Not much to really report in terms of directionality. The post Employment Situation Report rally was briefly tested overnight but not broken. The 10yr note is currently +13/32 at 97-05 yielding 2.595%

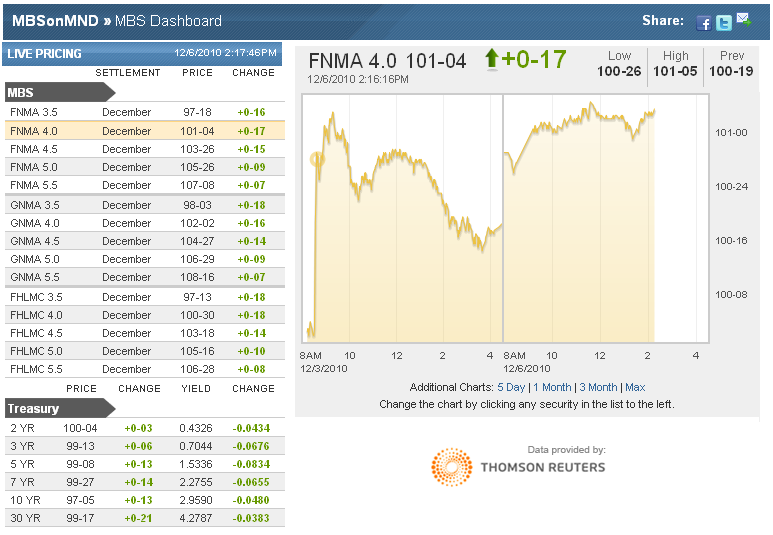

Current coupon mortgages are outperforming the long end of the yield curve but are lagging the belly. I've got the current coupon marked at 3.885%, which works out to about 2bps tighter vs. 10s and 3bps wider to 5s. Just like TSYs, the TBA MBS market has been quiet today but the bid seems more stable as illustrated by production coupons holding near their session price highs (see chart below). Rate sheets are better for the most part but I do note rebate reductions in the note rates at or below 4.375%

Here's a snapshot of the stack and benchmark Treasury indications....

ALERT: In the next 2 weeks we are opening our new MBSonMND product to a limited number of users. The above chart is a screenshot of MBSonMND. We are currently taking reservations for the final invite list to participate in this pre-release. If you are interested, please go to the following page and request an invitation. The page has more details about the product, including free trial and pricing information. You must be logged into MND to accept THIS INVITATION.