Productivity and Labor Cost data & Weekly Jobless Claims were just released. Rate sheet influential MBS coupons are rallying in the aftermath.

Reuters Quick Recap: Productivity and Unit Labor Cost

08:30 04Nov10 RTRS-U.S. Q3 NON-FARM PRODUCTIVITY +1.9 PCT (CONS +1.0 PCT) VS Q2 -1.8 PCT (PREV -1.8 PCT)

08:30 04Nov10 RTRS-U.S. Q3 NON-FARM UNIT LABOR COSTS -0.1 PCT (CONS +0.7 PCT) VS Q2 +1.3 PCT (PREV +1.1 PCT)

08:30 04Nov10 RTRS-TABLE-U.S. Q3 non-farm productivity rose 1.9 pct

Nonfarm business sector labor productivity increased at a 1.9 percent annual rate during the third quarter of 2010, the U.S. Bureau of Labor Statistics reported today.

Labor productivity, or output per hour, is calculated by dividing an index of real output by an index of hours worked by all persons, including employees, proprietors, and unpaid family workers. Output increased 3.0 percent and hours worked increased 1.1 percent in the third quarter. (All quarterly percent changes in this release are seasonally adjusted annual rates.)

Productivity increased 2.5 percent over the last four quarters, as output rose 4.1 percent and hours worked rose 1.6 percent

Unit labor costs in nonfarm businesses decreased 0.1 percent in the third quarter of 2010, because productivity grew 1.9 percent while hourly compensation increased 1.8 percent. From the third quarter of 2009 to the third quarter of 2010, unit labor costs declined 1.9 percent.

BLS defines unit labor costs as the ratio of hourly compensation to labor productivity; increases in hourly compensation tend to increase unit labor costs and increases in output per hour tend to reduce them.

Plain and Simple: The great thing about workers being productive is it opens the door to request higher hourly wages. Whether or not employers are willing to provide these pay increases is a factor of several variables such as how easily a worker can be replaced and what it costs to train new labor or if it is more efficient to just hire another employee. In this environment, there are many many willing labor substitutes, especially in the low-skill sector, so wage growth in blue collar space won't be too rapid, which reduces a workers incentive to seek out a job (do you see the potential for a downward spiral?). Furthermore, businesses are replacing more and more low-skilled labor with investments in technology. This affirms the idea that low skilled labor will face extra sticky hourly wages and find less incentive to seek out work. However, for workers who have a job and perform tasks that require specialized training (investment in humans), higher productivity is a positive as firms would like to remain efficient and would rather not spend the extra money on retraining new employees as opposed to incentivizing those they've already trained. Ben and the Board are hoping to spark some wage growth (via wage growth) as it would likely lead to greater disposable income and more consumer spending/investment in a low interest rate environment or simply allow for faster deleveraging. Their strategy seems to be capable of reaching only those who have jobs though, for those out of work, well I have yet to see a sustainable solution to that problem. We're still losing the lower middle class to investments in technology and CHINA's super low unit-labor costs.

Reuters Quick Recap: Jobless Claims

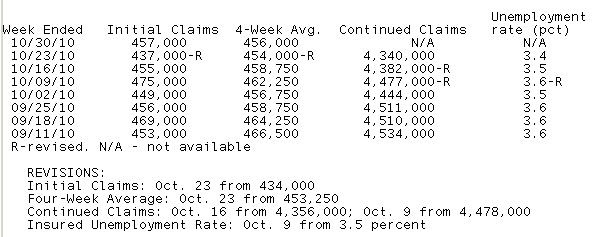

08:30 04Nov10 RTRS-US JOBLESS CLAIMS ROSE TO 457,000 OCT 30 WEEK (CONSENSUS 443,000) FROM 437,000 PRIOR WEEK (PREVIOUS 434,000)

08:30 04Nov10 RTRS-US JOBLESS CLAIMS 4-WK AVG ROSE TO 456,000 OCT 30 WEEK FROM 454,000 PRIOR WEEK (PREVIOUS 453,250)

08:30 04Nov10 RTRS-US CONTINUED CLAIMS FELL TO 4.340 MLN (CON. 4.380 MLN) OCT 23 WEEK FROM 4.382 MLN PRIOR WEEK (PREV 4.356 MLN)

08:30 04Nov10 RTRS-US INSURED UNEMPLOYMENT RATE FELL TO 3.4 PCT OCT 23 WEEK, LOWEST SINCE DEC 20, 2008 WEEK, FROM 3.5 PCT PRIOR WEEK (PREV 3.5 PCT)

08:30 04Nov10 RTRS-TABLE-U.S. jobless claims rose in latest week

Plain and Simple: The number of Americans out of a job for longer than 28 weeks = 6.1 million. That doesn't include the folks who aren't trying to get a job. There is a massive amount of resource slack in our economy. The labor market has locked out low-skilled workers. Jobless Claims data isn't telling us anything we don't already know.

Market Reaction...

Rate sheet influential MBS prices are closing in on record highs and the 2s/10s yield curve is bull flattening as benchmark TSY yields decline.

The 2s/10s curve is 8bps flatter at 216bps wide. The 5-yr note is +12/32 at 101-01 yielding 1.037%. 7s are +21/32 at 100-31 yielding 1.727%. The 10yr note is +23/32 at 101-03+ yielding 2.498%. No matter how you hedge your MBS position, the belly of the curve is outperforming, this a huge positive for MBS valuations. (The street is pacing production MBS coupons against a 50% hedge ratio vs. 10s.)

The 10yr note is up against a key resistance point and seems to be in need of more rally motivation (overcrowded longs should be enough). Fortunately 5s and 7s will probably continue to catch a bid regardless of econ data and earnings. Fed coupon lifts trump rational expectations at this point. I still feel the 10yr note should be lumped into that category but we'll need to monitor the situation closely as traders digest developments and adjust for pending debt issuance (3s,10s,30s next week). For now...all systems go on QEII TSY buying spree and lower interest rates.

Rate sheet influential MBS coupons are approaching record price highs in light early session trading flows. This should allow lenders to carefully inch back toward record low mortgage rates while keeping a close eye on capacity constraints and the potential for pipeline fallout.

The December delivery FNCL 3.5 is +0-18 at 101-05. The December FNCL 4.0 is +0-14 at 103-17. Current coupon yield spreads are wider on the spot.

I normally don't take a side as explicitly as I did over the past month re: QEII and lower mortgage rates. I am happy I did so but I do not want to encourage excessive risk taking with your lock/float strategy. Let's enjoy the ride but start getting back to a more responsible approach toward pipeline management.

Be patient with loan pricing. Lenders will be slow to pass along rebate improvements. The last thing secondary wants is to go gung ho only to see mortgage rates move even lower. This would increase fallout and hedging costs. The dust has yet to fully settle.