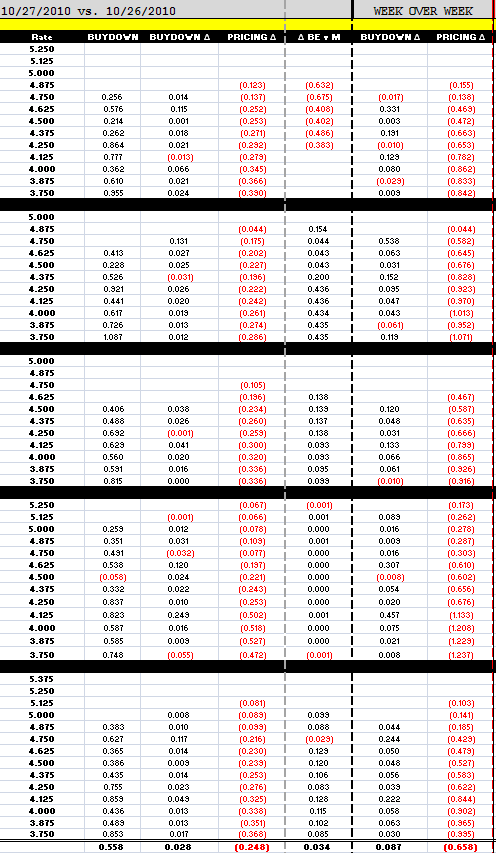

Loan pricing is another 24.8bps worse today. Rebate has been cut by over 100bps in the past three days. 4.25% is officially "best execution" for well-qualified borrowers.

There is a great deal of nervousness regarding the outlook for interest rates as it relates to QEII. I expected this to happen.

The bond market got ahead of itself with QEII and now we are experiencing a correction. I am confident that the recent rise in rates is not a function of a fundamental shift in economic outlooks though. It is a factor of the pain trade playing out followed by position squaring and tactical short selling by day trading black boxes.

Look at it this way...

At this point QEII isn't baked into yields anymore. This seems like a good thing to me as it reduces the potential for a "buy the rumor, sell the news" retracement on November 3.

Treasury announces the results of $35billion 5s at 1pm. I expect a strong turnout.