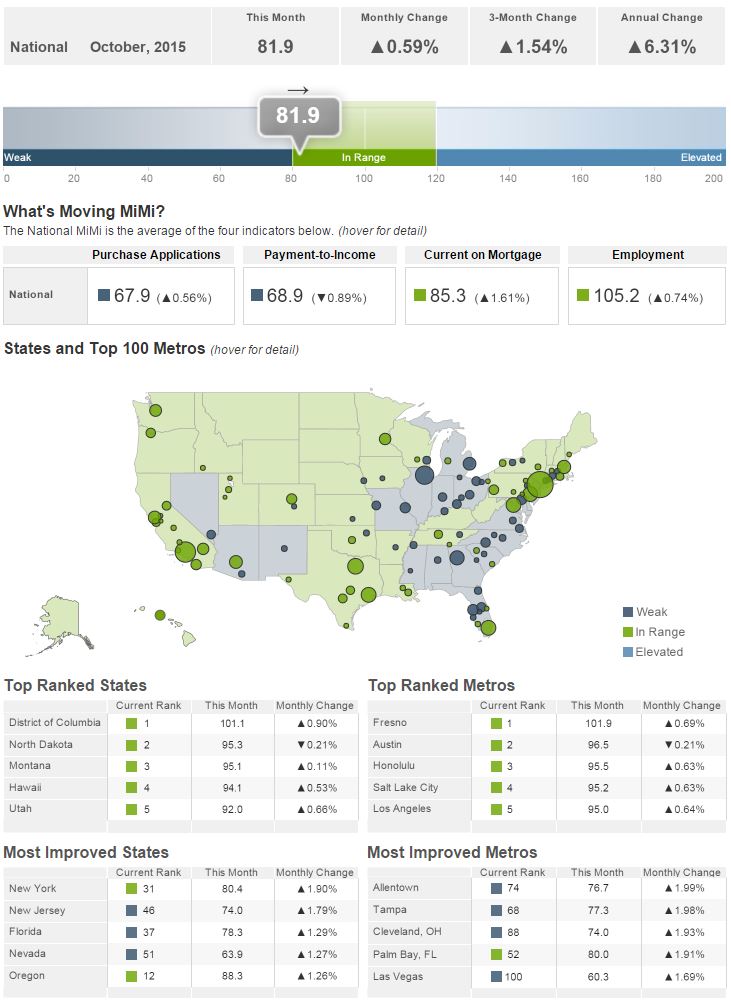

The Multi-Indicator Market Index (MiMi) produced by Freddie Mac's Office of the Chief Economist shows that the U.S. housing market is within the outer range of being considered stable. The national value of the index improved by 0.59 percent from September to October and has gained 1.54 percent over the last three months. The MiMi in October stood at 81.9.

On a year-over-year basis, the national MiMi value has improved +6.31 percent. Since its all-time low in October 2010, it has rebounded by 38 percent, but remains significantly off its high of 121.7. Two additional states-New York and Kansas-entered their outer range of stable housing activity, as did three more metro areas: New York, New York; Minneapolis, Minnesota and Palm Bay, Florida.

Freddie Mac Deputy Chief Economist Len Kiefer said, "The strong annual change of 6.31 percent is the best improvement we've seen in the MiMi on a year-over-year basis since July 2014. While strong home purchase applications and rising home values in some markets are contributing to this improvement, its largely more of a reflection of mortgage delinquencies continuing to decline at a steady pace, especially in those hardest hit markets, and a better employment picture overall.

"States in the West are still seeing some of the strongest housing activity and among those Utah really stands out. Not only do many of the state's local housing markets such as Salt Lake City, Provo and Ogden have strong buyer demand but they're also still largely affordable for the typical family looking for a median priced home. This is due to the state's robust economy and better than average job creation."

MiMi monitors and measures the stability of housing markets in each of the states and in the top 100 metro markets by combining proprietary Freddie Mac data with current local market data to assess where each single-family housing market is relative to its own long-term stable range. Freddie Mac looks at home purchase applications, payment-to-income ratios (changes in home purchasing power based on house prices, mortgage rates and household income), proportion of on-time mortgage payments in each market, and the local employment picture to create a composite MiMi value for each market. MiMi also indicates how each market is trending, whether it is moving closer to, or further away from its stable range. A market can fall outside its stable range by being too weak to generate enough demand for a well-balanced housing market or by overheating to an unsustainable level of activity.

Thirty-two of the 50 states plus the District of Columbia are now considered to be in a stable range for housing activity. The top ranked jurisdictions are the District of Columbia (101.1), North Dakota (95.3), Montana (95.1), Hawaii (94.1) and Utah (92). At the same time in 2014 21 states and the District of Columbia were in the stable range.

Twenty-nine of the top 100 metro areas were considered stable in October 2014; that number has now increased to 53 with Fresno (101.9), Austin (96.5), Honolulu (95.5), Salt Lake City (95.2) and Los Angeles the five top-ranked.

The five most improved states over the last month were New York, New Jersey, Florida, Nevada, and Oregon, each improving more than 1.25 percent. On an annual basis the leaders were Florida (+14.47%), Oregon (+12.2%), Colorado (+11.97%), Washington (+11.69 %) and Nevada (+11.13%).

The most improved metro areas from September to October were Allentown, Tampa, Cleveland, and Palm Bay, Florida all of which showed improvement ranging from 1.91 to 1.99 percent, and Las Vegas, up 1.69 percent. On a year-over-year basis, the most improving metro areas were Orlando, (+17.94%), Tampa, (+16.94%), Cape Coral, (+16.60%), Denver, (+15.21%) and Palm Bay, (+14.78).

In October, 43 of the 50 states and 89 of the top 100 metros were showing an improving three-month trend compared to a year earlier when 36 states and 70 of the top 100 metro areas were doing so.

Kiefer continued, "We do expect homebuyer affordability to decrease in the coming year, but we don't expect tighter monetary policy to generate a spike in longer-term interest rates in the foreseeable future. The Fed has committed publicly to measured increases in short-term rates. While mortgage rates will rise modestly, they will still remain at historically low levels. Combined with stronger job and income growth, the net result may be strong growth in household formation, construction, and home sales."