The government sponsored enterprises'' (GSE's) introduction of 97 percent loan-to-value (LTV) mortgages, implemented by Fannie Mae' in late 2014 and by Freddie Mac in the spring of 2015, has apparently done little damage to the government guarantee sector's dominance in that market place. Black Knight Financial Services' most recent Mortgage Monitor points out that the Federal Housing Administration (FHA) and the Veterans' Administration (VA) loan programs have continued as the primary drivers in that expanding segment of purchase mortgage lending.

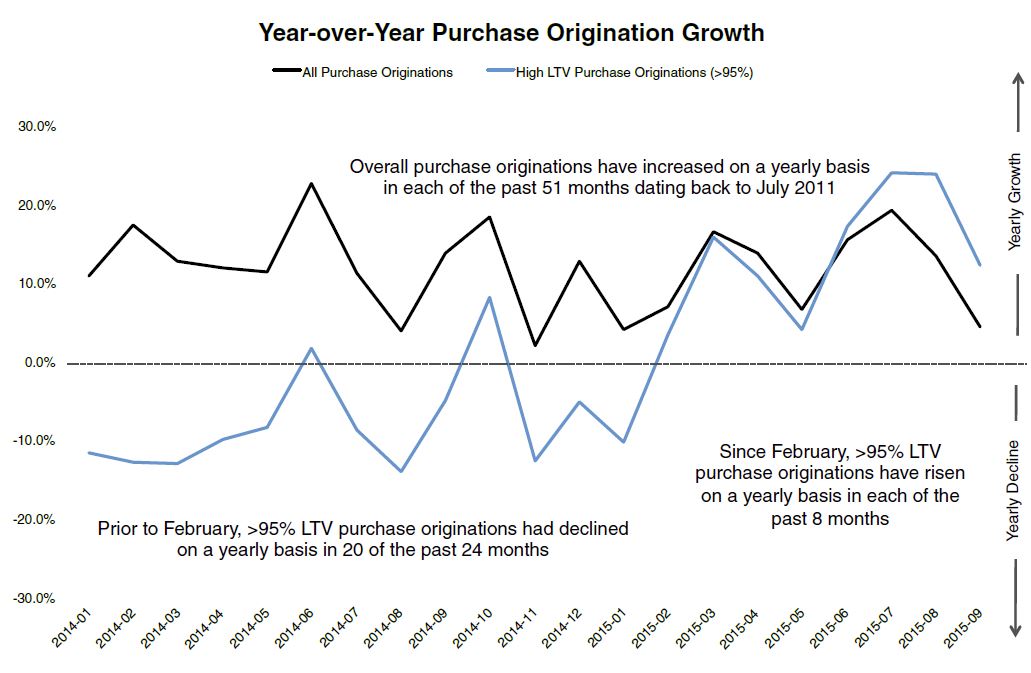

Low downpayment lending, that is mortgages with a 95 percent or higher LTV ratio, were up 20 percent in the third quarter of 2015 compared to the same period in 2014 while the overall purchase market expanded by only 13 percent. Despite this increase the GSEs' new products garnered only 3 percent of those low down-payment originations.

One factor that probably mitigated against greater use of the GSEs' new loans was a 50 basis point reduction in the FHA annual mortgage insurance premium which went into effect as Fannie and Freddie's products were being rolled out.

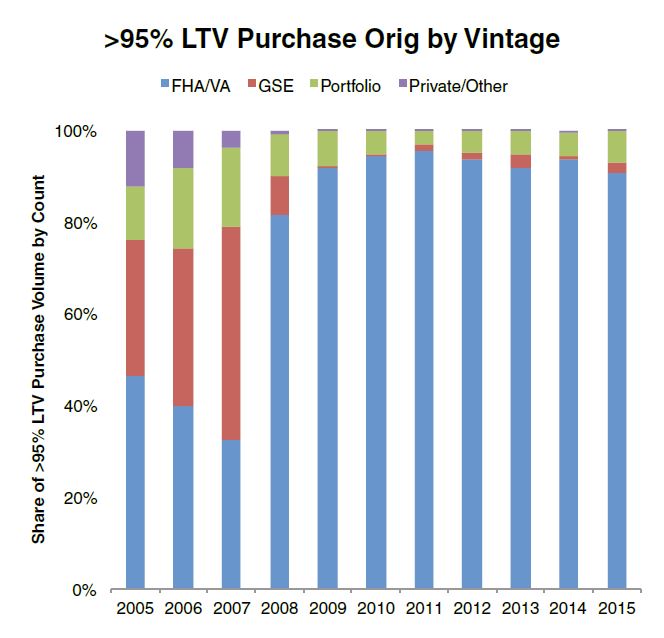

Black Knight Data & Analytics Senior Vice President Ben Graboske said, "High-LTV products now account for 23 percent of all purchase originations. What's particularly interesting is how heavily this market is dominated by FHA/VA. Back in 2007, the GSEs made up over 45 percent of high-LTV purchase originations, while FHA/VA lending made up roughly one-third. Since 2009, FHA/VA products have made up over 90 percent of high-LTV purchase originations every year, and the same is true in 2015, even with the GSEs having reintroduced their own 97 percent LTV products. In fact, those products have accounted for less than 3 percent of all high-LTV originations so far this year.

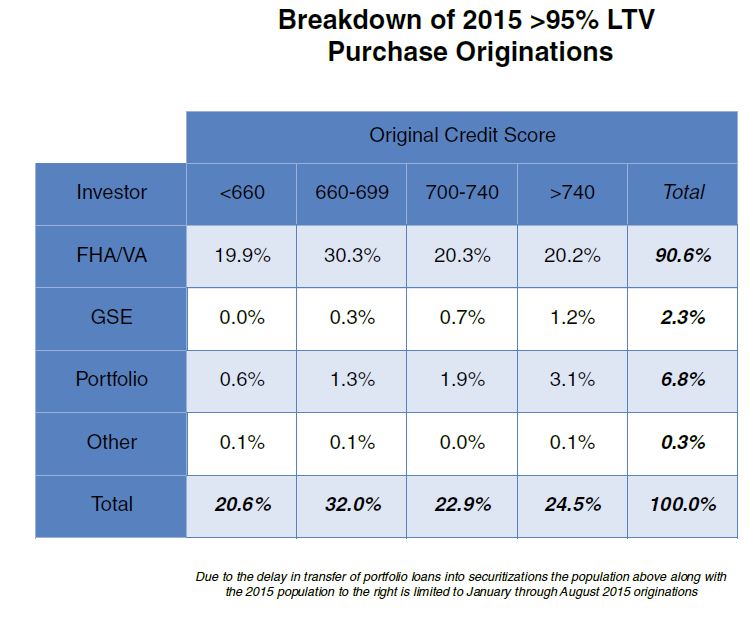

"As we reported last month, recent increases in purchase lending have been driven primarily by higher-credit- score borrowers, and these high-LTV products are no exception. We've seen average credit scores on high-LTV FHA/VA loans rise six points from last year to 706. Of course, scores for GSE and portfolio high-LTV loans are roughly 35 points higher still. We've actually seen annual declines in high-LTV lending among 620-660 credit scores for each of the past six months even though overall high-LTV purchase volumes have risen in each of those months. This may be attributed to tightening credit, or it may be that the FHA's reduced annual mortgage insurance - which FHA estimates will reduce borrowers' mortgage payments by $900/year - has enticed some higher-credit borrowers into those FHA products."

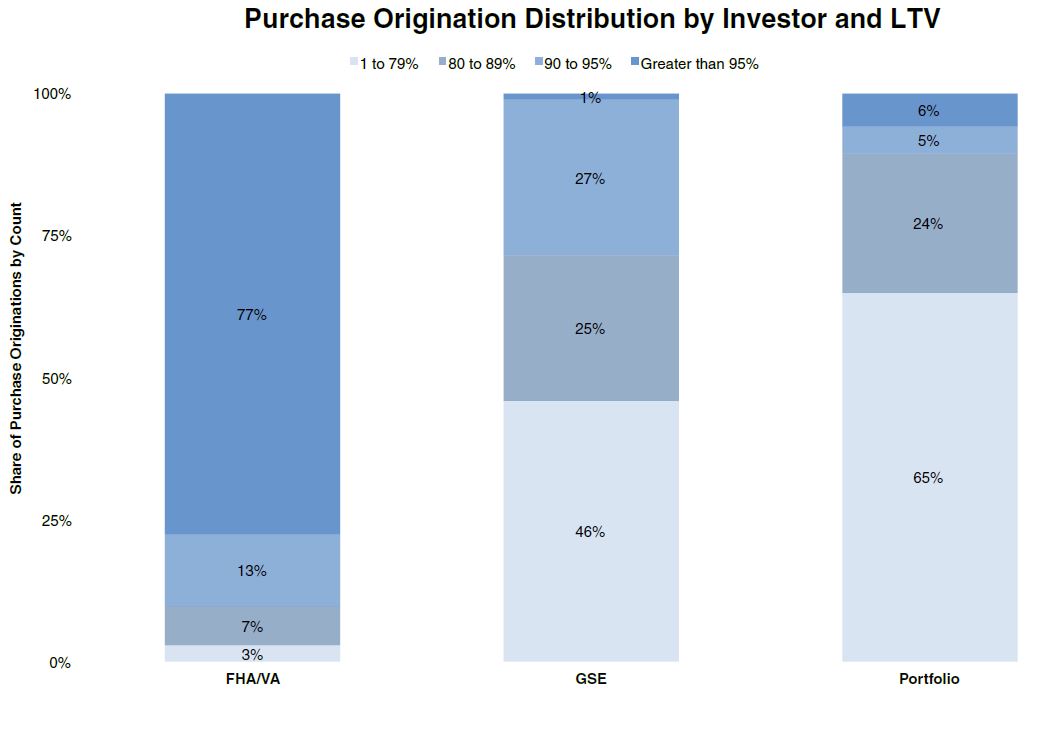

High LTV lending also comprises the lion's share of FHA and VA purchase originations - 77 percent for the year through August - while making up only 1 percent of the GSEs' purchase lending. Portfolio lending is also skewed toward lower LTV loans, they make up two thirds of that purchase lending, and the high LTV loans that are made by that investor group tend to be in higher credit tranches. Nearly 75 percent of high LTV purchase loans made by portfolio lenders had credit scores above 700 while half of all such FHA/VA originations had scores below that line.

The Monitor also found that residential home sales so far in 2015 are 4 percent higher than at the same time last year but the share of traditional sales has risen by 7 percent. The sale of lender owned real estate (REO) and short sales had fallen to 8.8 percent in July, the lowest since 2007 after falling on an annual basis for 42 consecutive months. The cash share of overall purchase transactions has likewise fallen to its lowest level since Q3 2008, accounting for 28 percent of single-family transaction in the third quarter compared to 32 percent a year earlier. The cash share of condo sales fell below 50 percent in the second quarter for the first time in nearly five years although it is still at twice the rate seen in 2005 and 2006.

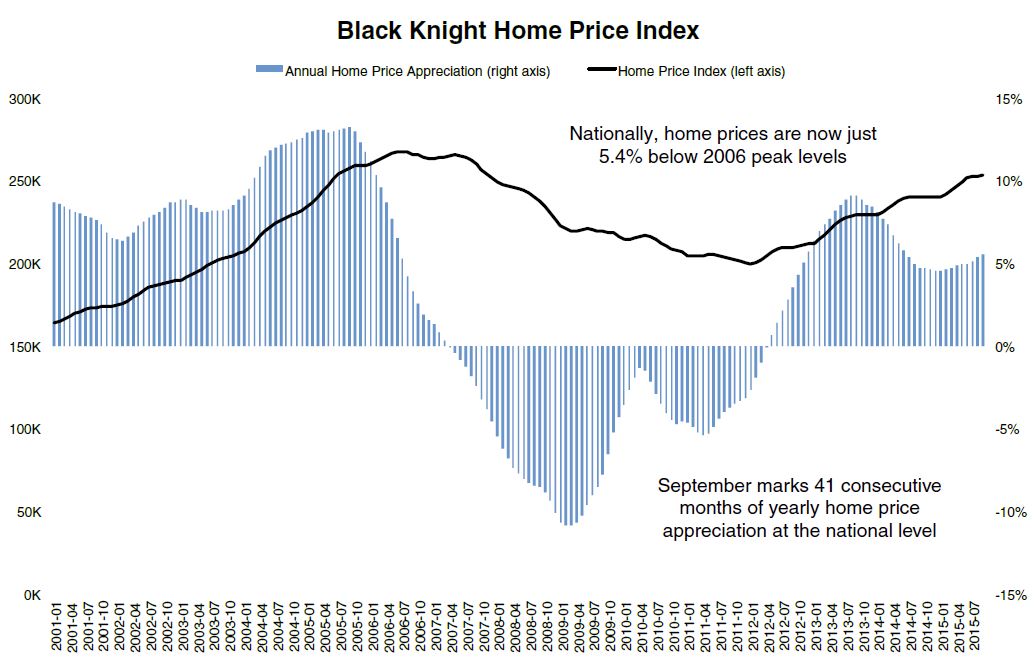

As of September, the U.S. has now experienced 41 consecutive months of annual home price appreciation. That month, with annual appreciation of 5.5 percent, had the largest gain thus far in 2015. The trend of decelerating price increases seen going into the year has now reversed itself and September also marked the ninth consecutive month in which annual appreciation increased.

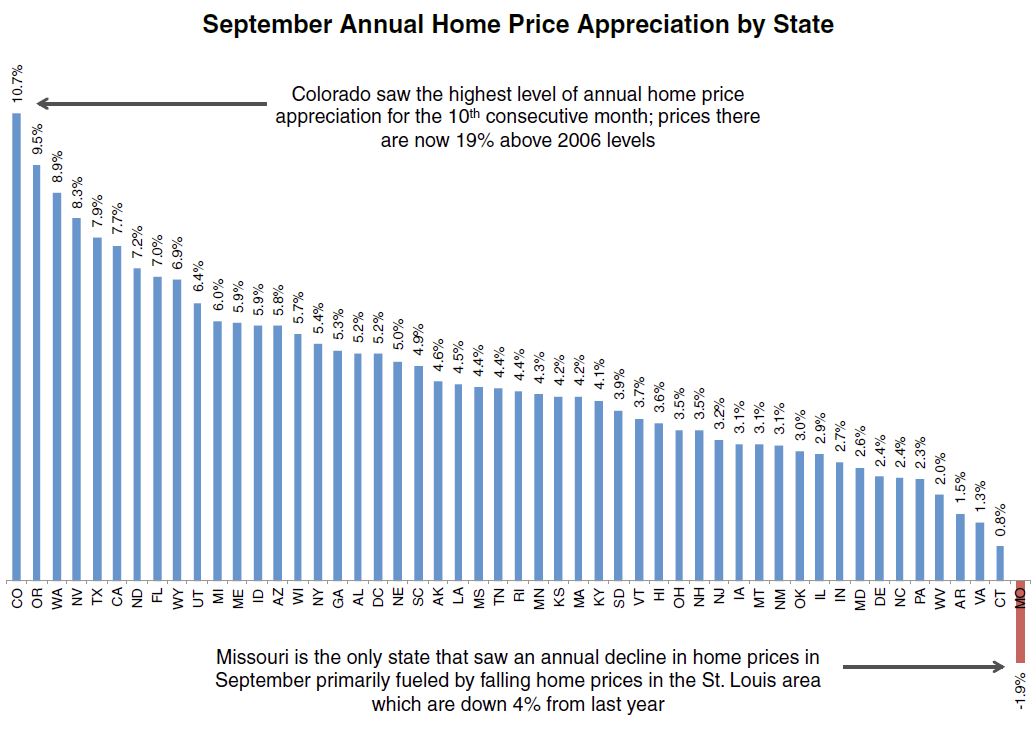

Colorado stands out among all states with a near 11 percent annual gain, leading the country in annual home price appreciation for the 10th consecutive month. Home prices in Colorado are now 19 percent above their 2006 prior peak levels. North Dakota - fueled by the oil boom there - leads the nation in terms of growth over pre-crisis peaks, with home prices 31 percent above 2006 levels. Nineteen states and Washington DC have now surpassed their price peaks of 2005-2006.

Missouri is the only state that saw an annual home price decline in September, with home prices in the state down 1.9 percent from last year, driven primarily by a decline in the St. Louis metro area. Declines in St. Louis were most pronounced on homes valued in the high end (down 7 percent) and the low end (down 5 percent), with a metro area average decline of 4 percent.