For many years homebuyers looking for homes priced above entry level employed every device they could to keep their loan amount below whatever might be the current limit for conforming (Fannie Mae, Freddie Mac) loans. It might mean determining between the purchase of two similarly priced homes if only one squeaked by under the limit. Buyers came up with larger down payments, dipping more deeply into savings, hitting up the bank of mom and dad, or employing piggy-back second mortgages. Why? Because a jumbo loan would almost always have a higher interest rate than a conforming loan. That higher monthly payment could even mean the difference between qualifying for the loan or not.

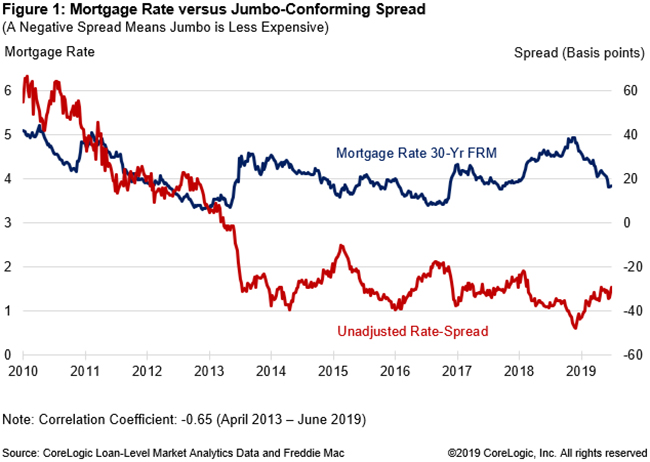

However, starting in 2013 the spread between a conforming and a jumbo loan began to narrow, and today's jumbo loans typically have a lower interest rate. In a recent post in CoreLogic's Insights blog, Arachana Pradhan looked at this trend and some of the reasons behind it.

Interest rates account for some of the variation in the spread. The degree of the spread is inversely correlated with prevailing interest rates. For example, as the mortgage rate dropped during the first eight months of 2019 the spread has gone up. The drop in rates prompted a surge in refinance applications and, because there is a limited secondary market for jumbo loans and also because many lenders had reduced staffs, there were bottlenecks in production for jumbo loans which was reflected in an increasing spread. Other factors contributing to the spread are an increase in the GSE guarantee fee, a reduction in the GSE funding advantage, and portfolio lenders' desire to hold jumbo loans.

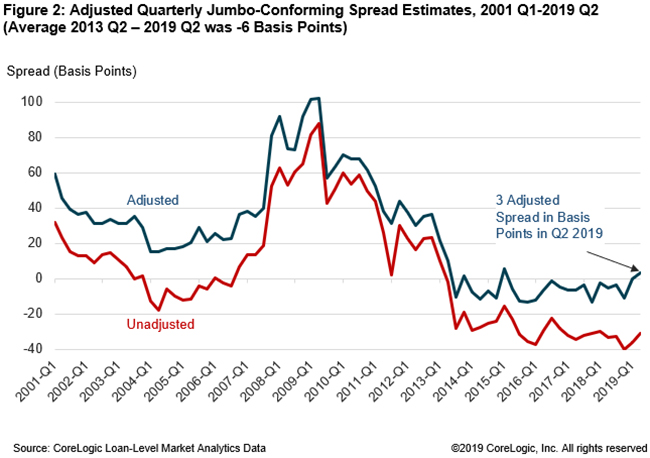

But Pradhan says, when certain salient borrower and loan characteristics are taken into consideration, the spread becomes near zero. When conditions such as credit risk, location, and loan size are controlled, the spread narrowed from an average of 30 basis points (unadjusted) to an average of 6 basis points from the second quarter of 2013 to the same quarter in 2019.

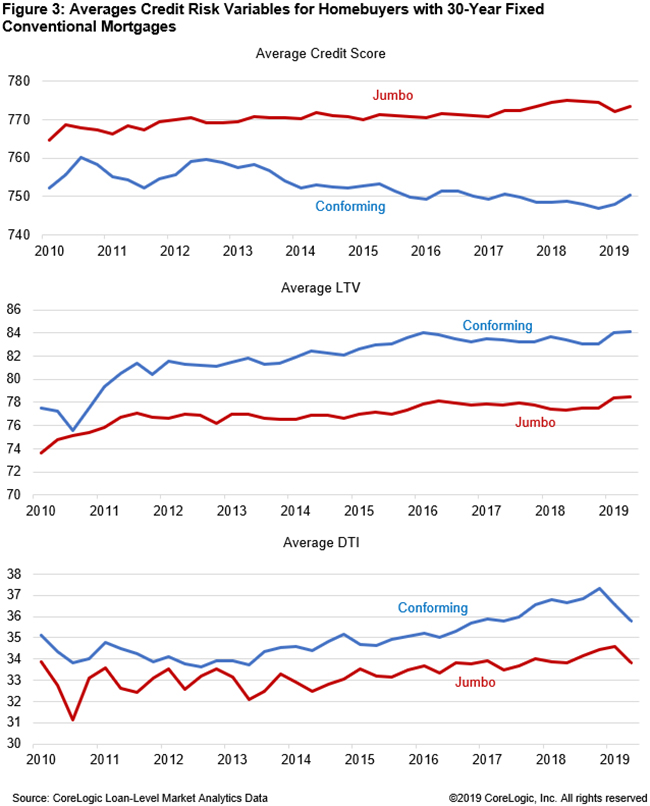

Because of higher underwriting standards, the three main loan qualifiers, credit scores, loan to value (LTVs) and debt-to-income (DTI) ratios, jumbo loans today have a higher credit profile than conforming loans. In 2018 jumbo loan scores averaged 26 points higher than conforming loans, LTVs are 6 points and DTI's 3 points lower. Pradhan says these differences help account for much of the jumbo/conforming spread over the past several years.