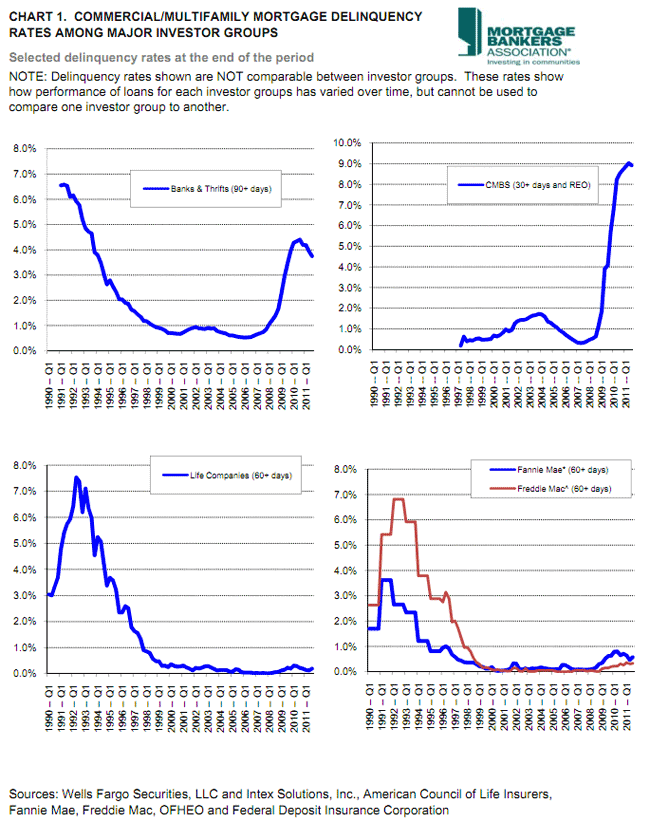

The Mortgage Bankers Association (MBA) reports that, in the third quarter of 2011, delinquencies among commercial and multifamily mortgages were mixed, with rates for loans held by some investors declining while delinquencies among loans held by others improved. While changes from quarter to quarter were modest, loans held by life insurance companies and by Freddie Mac and Fannie Mae ticked up slightly while those held by banks or in commercial mortgages-backed securities (CMBS) were down.

Delinquencies among commercial and multi-family loans held by FDIC-insured banks and thrifts decreased 0.19 percent to 3.75 percent and those held in CMBS were down from 9.02 percent to 8.92 percent. The rate increased 0.07 percent to 0.19 percent for loans held by life insurance companies while the rate for loans held by Fannie Mae rose from 0.46 percent to 0.57 percent from Q2 to Q3 and Freddie Mac loans increased from 0.31 to 0.33 percent.

The delinquency rates in the third quarter for mortgages held by banks and thrifts was 2.83 percentage points lower than the record high of 6.58 percent reached in the second quarter of 1991 and the rate for life insurance-owned loans was 7.34 points lower than the series high of 7.53 percent in the second quarter of 1992. Loans held by the government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac were 3.05 points and 6.48 points below their respective peaks in the fourth quarter of 2001 and the fourth quarter of 2002. Loans held in CMBS are down 0.10 percentage points from the high of 9.02 percent established just last quarter.

Delinquency rates are not comparable across investor types because of different methods of calculation. Rates for loans held by life insurance companies and the two GSEs are based on delinquencies of 60 or more days. The term is applied to CMBS loans which are 30+ days delinquent or are bank owned real estate, and to loans held by banks and thrifts that are 90 plus days in arrears or in non-accrual.