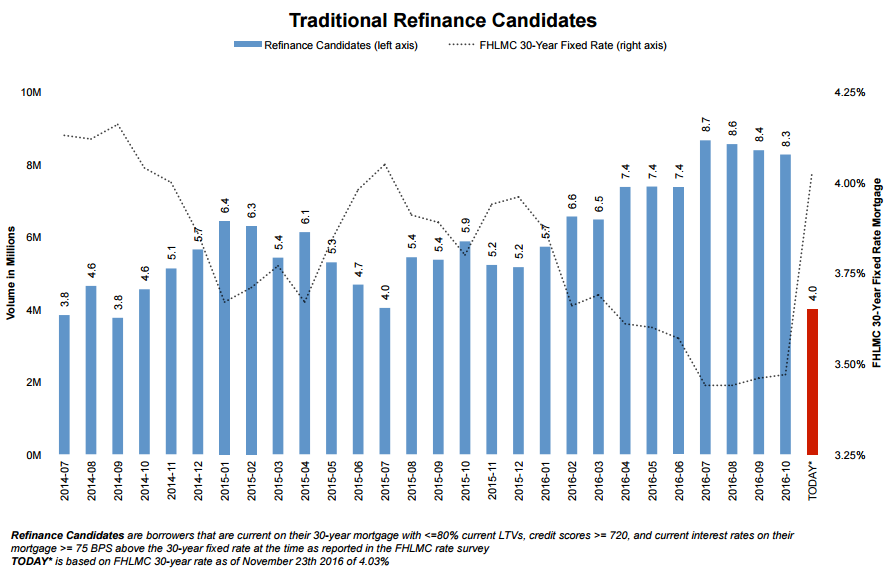

As everyone knows, interest rates shot up immediately in the wake of the November 8 presidential elections, triggered by a sell-off in Treasury bonds. Now Black Knight says, in its current Mortgage Monitor, that the jump eliminated 50 percent of candidates from the refinanceable population that existed before the election and has also pushed home affordability to a post-recession low.

Within three-weeks of the election the 30-year fixed-rate increased by 49 basis points, cutting the number of homeowners who might potentially refinance (either because they could qualify or there was a financial incentive for doing so) from 8.3 million to 4.0 million. This matches a 24-month low set in July 2015. At that time refi volumes were 37 percent lower than in the third quarter of 2016. About $2 million borrowers could still save $200 per month by refinancing but Black Knight puts aggregate potential monthly savings at approximately$1 billion, down from $2.1 billion in early October.

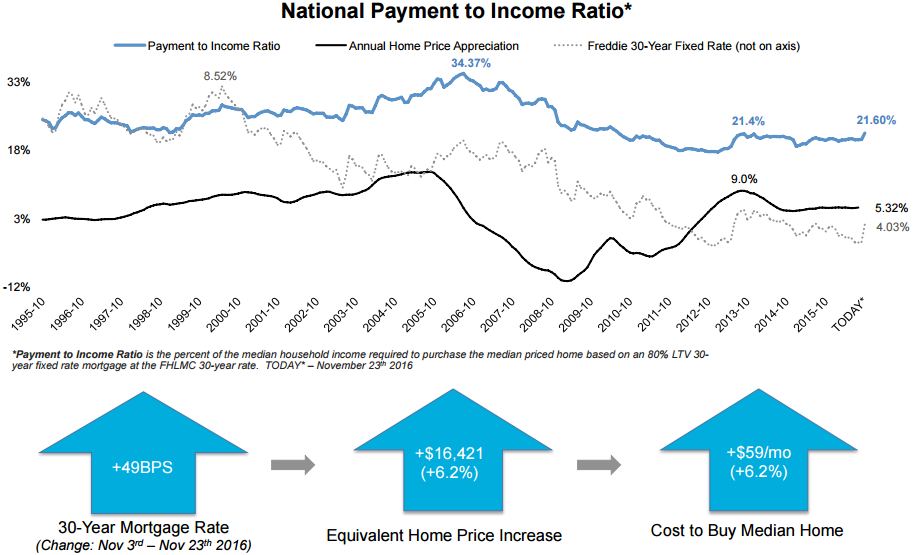

It now takes 21.6 percent of the national median monthly income to purchase the median priced home, the highest share since June 2010. At that time interest rates were higher, averaging 4.75 percent, but home values were 20 percent lower than today. Black Knight says that in 2013 the affordability ratio was also hit the 21 percent range and annual home price appreciation decelerated rapidly - from 9 percent to below 5 percent.

As Black Knight Data & Analytics Executive Vice President Ben Graboske said, "These changes will likely have an impact on refinance origination volumes moving forward. And, since higher interest rates tend to reduce the refinance share of the market - specifically in higher credit segments - which typically outperform their purchase mortgage counterparts, they may potentially impact overall mortgage performance as well." He added, "In addition, from an affordability perspective, that 49 BPS rise in interest rates was the equivalent of the average home price jumping by over $16,400 basically overnight."

He noted that given the recent historical perspective of the rapid deceleration in home price growth in 2013, "It's worth watching to see how home prices react to such an abrupt rise in rates over the coming months, particularly as we await the Federal Reserve's next moves on the benchmark federal funds rate."

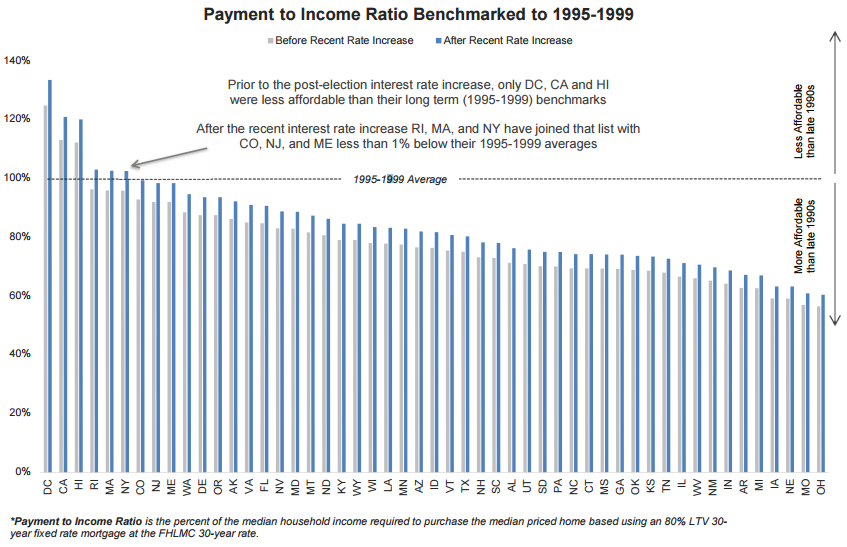

Despite the rate increases, the 21.6 payment to income ratio is 10 percent lower than in n the benchmarked period of 1995-1999. Thirty states, in fact, remain 15 percent below those earlier levels and Ohio and Missouri are 40 percent below long-term norms. Six states, are less affordable now than then, including California and New York, while Colorado is closing in on a new low.

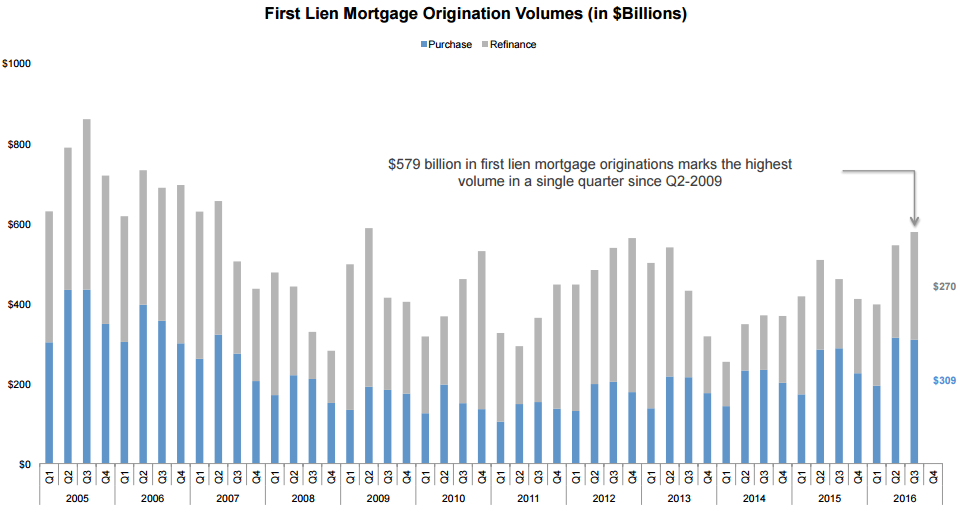

Black Knight also looked at Q3 originations, finding that despite a slight quarterly decline in purchase lending, overall originations were up six percent from Q2. The $579 billion in loans originated in Q3 2016 marked the highest total origination volume since the second quarter of 2009 and was largely due to a 17 percent quarterly rise in refinance lending to $270 billion, the largest since the second quarter of 2013.

Purchase volumes are up 7 percent from 2015 and the $818 billion volume year-to-date is the highest for any such period since 2007. The volume is still nearly 30 percent below that in 2005 but within 13 percent of third quarter 2006 levels.

The growth in purchase origination growth is slowing, however, and most markedly among higher credit borrowers (740+ credit scores), the segment which has mainly driven the overall recovery in purchase volumes and currently accounts for two-thirds of all purchase lending. Black Knight says this could be a sign of possible market saturation and bears close watching.

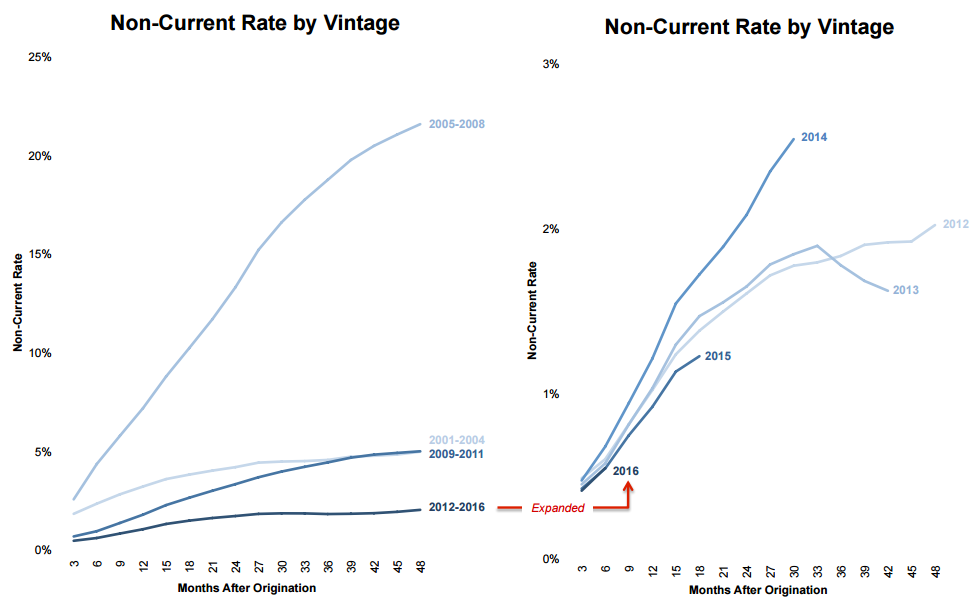

The Monitor also dug further into delinquency data released earlier in its "first look" report. It notes that delinquencies in 2012-2016 vintage mortgages are extremely low, fewer than 2 percent among those with at least two years of seasoning. This is 50 percent under the rate for 2009-2011 vintage loans and 60 percent lower than those originated from 2001 to 2004, which was prior to the loosening of credit which led to the housing crisis.

Those mortgages originated in 2015 have a 10 percent lower non-current rate than the second lowest year, 2012. This year's originations appear to be performing in a similar manner. Black Knight says one reason behind the "stellar" performance of the last two years' originations is the high ratio of refinancing, loans which typically perform better than purchase mortgages. Those refinances were also weighted toward high credit borrowers.

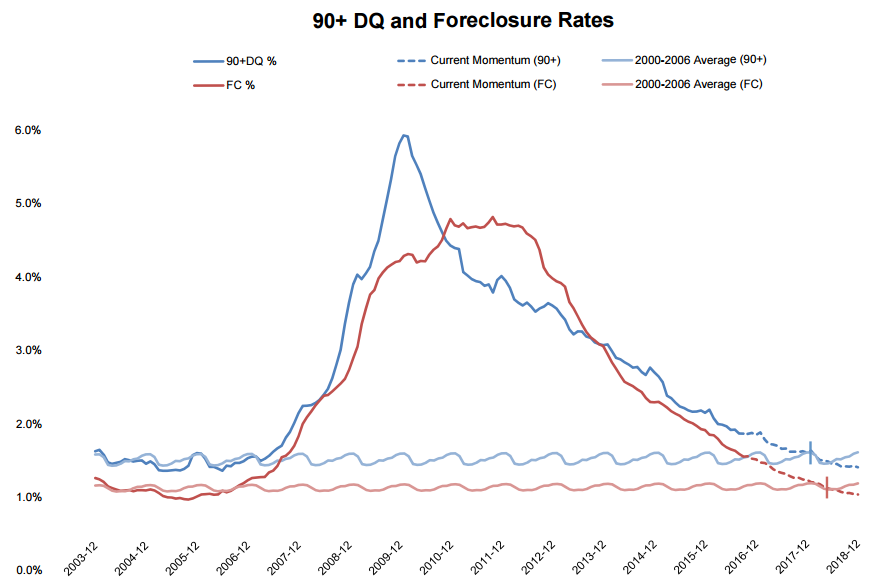

Looking at foreclosures also gives insight into the improving quality of loans. While there are still 1.2 million loans that are 90 days or more past due or in foreclosure, a whopping 52 percent of them are in the perpetually troublesome 2004-2007 vintage; originations that make up only 18 percent of active loans. By loan type, Black Knight says "there are currently more serious delinquencies and active foreclosures (313,000) in bubble era private label securities (PLS) than there are for the 2008-2011 vintages combined. The second largest group is the 2008-2011 era FHA/VA originations. This suggests "there may yet be a need for loan modifications focus in post-bubble era originations as well."

Black Knight finds that foreclosure inventories are declining at rates of 30 percent or more annually and foreclosure rates in 15 states are now below their pre-crisis levels. Early state delinquencies also continue to drop with the 30-day rate in October nearly 20 percent below long-term October averages.

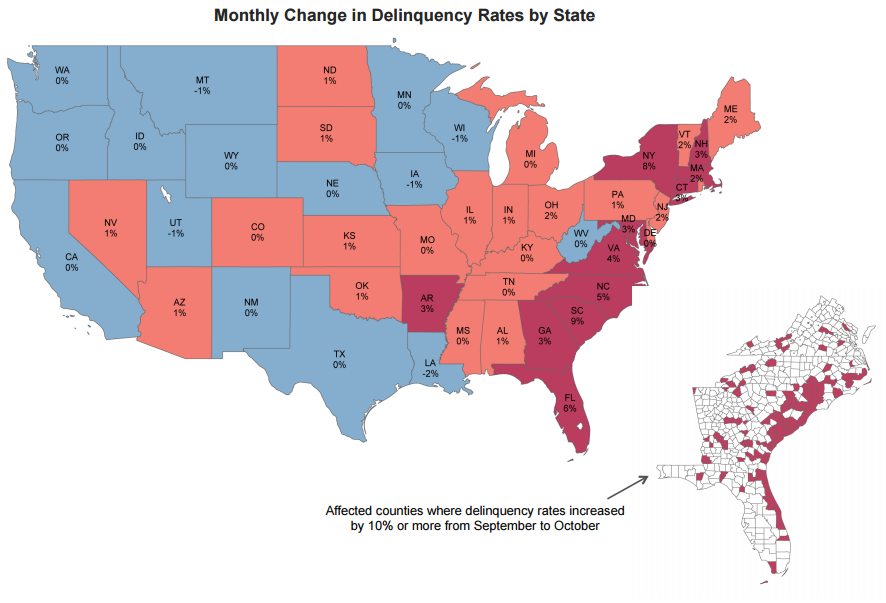

There is an exception however. The Monitor notes there has been a sharp increase in past due loans in states affected by Hurricane Matthew in early October. The hurricane hit from mid-coast Florida up through North Carolina. In South Carolina, the delinquency rate jumped nine-percent, from 5.1 to 5.6 percent and increased as much as 20 percent in some areas. In northeastern Florida, the increase ranged from 10 to 20 percent.

The report notes that, since the worst of Mathew hit on October 7th and 8th, many homeowners had already made their monthly payments. "We could yet see further impact in November's mortgage performance data."