In its Mortgage Monitor for September, Black Knight outlined the first wave of mortgage delinquencies that appeared to be arising out of Hurricanes Harvey and Irma that struck primarily in Texas and Florida in August and September. The Monitor for October updates that data and brings in new information on delinquencies in Puerto Rico, struck a few weeks later by Hurricane Maria.

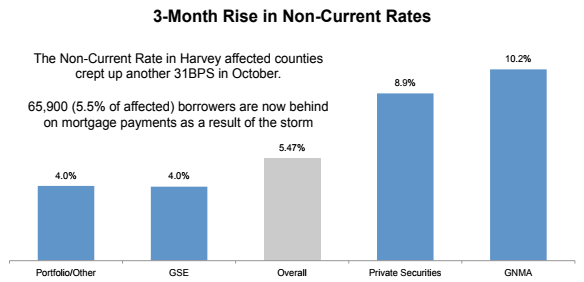

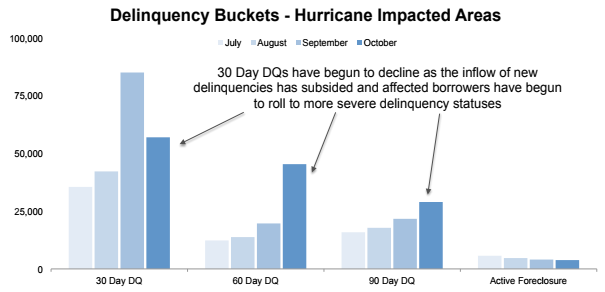

The company found a 31-basis point increase in the non-current rate in those areas affected by Hurricane Harvey. This was in addition to the 16 percent spike that occurred in the weeks following the storm. In addition to an increase of 19 percent in the 30-day bucket, those rolling into 60-days past due increased by 12 percent.

The October increase contributed to a near doubling in the delinquency rate, from 5.9 percent in July to 11.3 percent in October. The increased rate has pushed the number of past due mortgages in those areas to more than 135,000, with an estimated 50 percent, or 65,900, of them thought to be a direct result of the storm. That means that 5.5 percent of all affected borrowers in the area have fallen behind on their mortgage payments. Loans in private label and GNMA securities were hardest hit, with non-current rates rising by 8.9 and 10.2 percentage points respectively.

The rate of 30-day delinquencies has begun to shrink as the influx of new missed payments slows, but transitions into later stages continue to climb. Sixty-day delinquencies have increased by 33,000 over the last three months and there are 13,000 more 90-day delinquent loans.

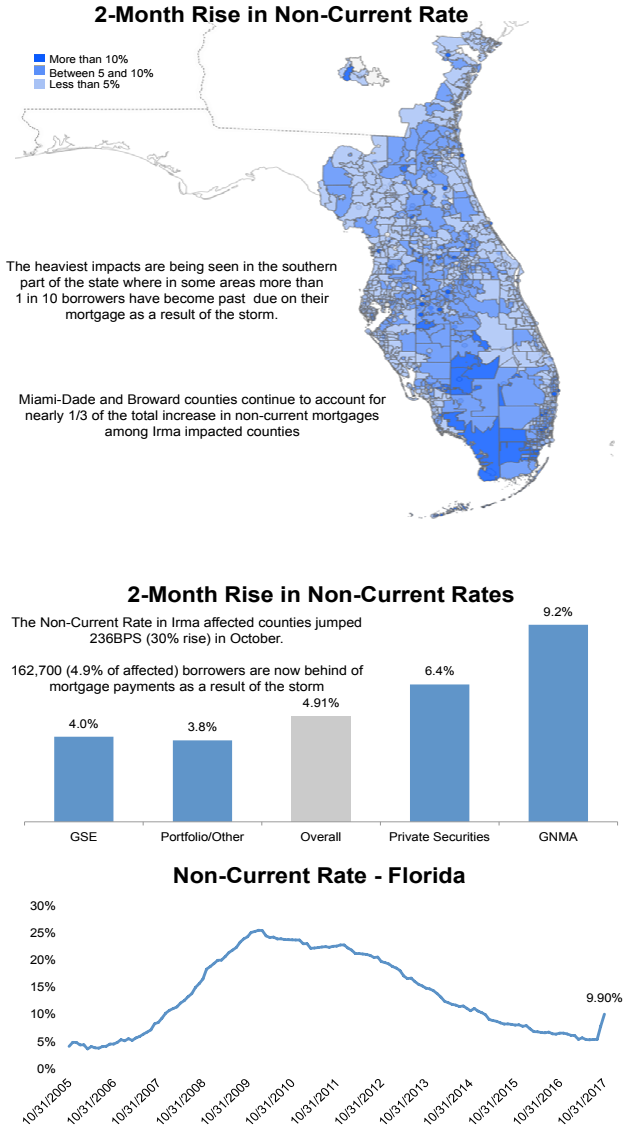

The first mortgage payments after Irma's destruction were due in October. The past due rate in affected counties were up over the two months ended in October by 4.9 percent with 163,000 borrowers becoming delinquent as a result of the storm. The rate of all borrowers in the affected areas who have fallen a payment behind is 5.0 percent, slightly behind that in Harvey-hit areas, but by count more than 95,000 more loans. Over all of Florida, the non-current rate has jumped by 468 basis points or 90 percent, to 9.9 percent, the highest since early 2015. Again, it is GNMA seeing the greatest impact in terms of percentages although Fannie Mae and Freddie Mac, the GSEs, have suffered the heaviest impact by volume, with 75,000 borrowers falling behind because of the storm.

The two hurricanes are also affecting the national delinquency rate. It rose by 27 basis points in September. Factoring in October brings that increase to 45 basis points. Black Knight says there may be an additional small increase in November, but the bulk of the storms' impact from a delinquency inflow perspective has probably already occurred. This 45-point impact is nearly twice the rise attributed to Katrina in 2005 even though that storm had a much heavier local impact.

Private label securities have been the most impacted by the storms, the delinquency rate is up 90 basis point and the hurricane cause 31,000 past due loans. Again, while the percentage increase was moderate, 35 basis points, the largest volume was among those guaranteed by the GSEs, 103,000 distressed loans.

In addition to looking at the mortgage related damage by Maria, Black Knight sketched out a portrait of the Puerto Rico mortgage market. It estimates there are about 425,000 active loans in the island territory with an outstanding balance of $40 billion. This is 1 percent of the total U.S. count, and 0.5 percent of all outstanding balances. By way of comparison its market is about the same size as the Orlando metro area or the state of Iowa.

An estimated 30 to 35 percent of Puerto Rican mortgages are GSE-related, compared to 58 percent on the mainland. Portfolio lenders and GNMA each account for about 30 percent, a much higher share than the rest of the US. The average loan balance is $95,000 (the U.S. as a whole is $193,000) and the interest rate averages nearly a point higher at 5.1 percent, probably in part because are much older; 97 months compared to 53 months in the 50 states. The average FICO score is 714, 26 points lower than the U.S. average.

Maria probably just exacerbated what was already a high non-current rate of 5.0 percent, with 3.2 percent of loans in active foreclosure. Lender moratorium have held the foreclosure rate steady, but one out of five homeowners who were current on their mortgage payments pre-Maria have now fallen behind, pushing the delinquency rate to 32 percent. When existing foreclosure cases are added in, the non-current rate goes to 35.4 percent.

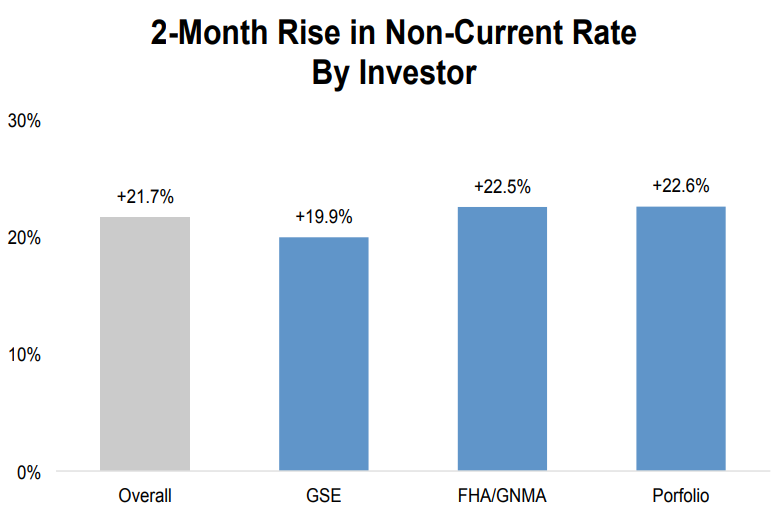

The 21.7 percent increase in non-current loans in the last two months is comparable to a rise of 22 percent in areas impacted by Katrina. In terms of borrower financial impact, the greatest effects of the storm appear to be in the central and southeastern portions of the island with the more heavily populated regions seeing lower increases per capital. Black Knight currently estimates that over 90,000 mortgages have become non-current because of the storms (Puerto Rico was also hard hit by Irma). So far the storms impacts have been close to evenly distributed across all investor groups, for a rise of 19.9 percent among GSE loans to 22.6 percent for portfolio loans.

The company concludes that prior storms have shown that the impact of Maria is likely to rise again in November and says that foreclosure moratorium and additional borrower assistance programs are certainly needed to help affected borrowers in Puerto Rico.