The National Association of Realtors released the Pending Home Sales Index for October today.

NAR's Pending Home Sales Index measures the number of home purchase contracts that were signed in the monthly reporting period. Once "pending" sales contracts are closed, they are considered an Existing Home Sale. Because the Pending Home Sales index tells us how many contracts were signed, it is considered a forward indicator of Existing Home Sales. A signed contract is not counted as an Existing Home Sale until the transaction actually closes.

Excerpts from the Release....

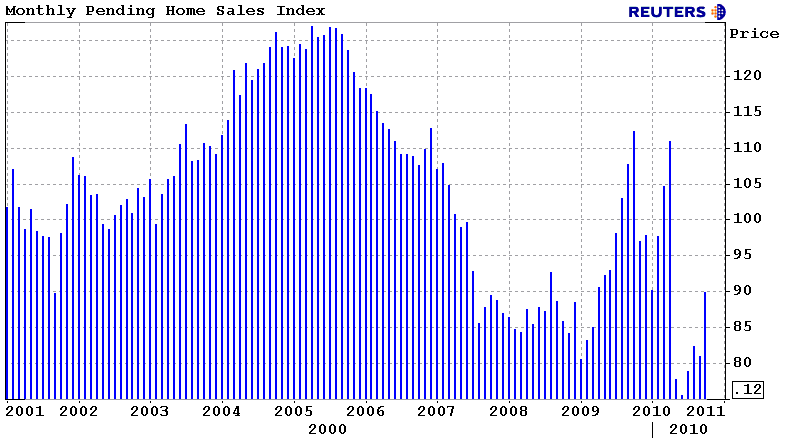

Pending home sales jumped in October, showing a positive uptrend since bottoming in June, according to the National Association of REALTORS®.

The Pending Home Sales Index, a forward-looking indicator, rose 10.4 percent to 89.3 based on contracts signed in October from 80.9 in September. The index remains 20.5 percent below a surge to a cyclical peak of 112.4 in October 2009, which was the highest level since May 2006 when it hit 112.6.

Last October, first-time buyers were motivated to make offers before the initial contract deadline for the tax credit last November.

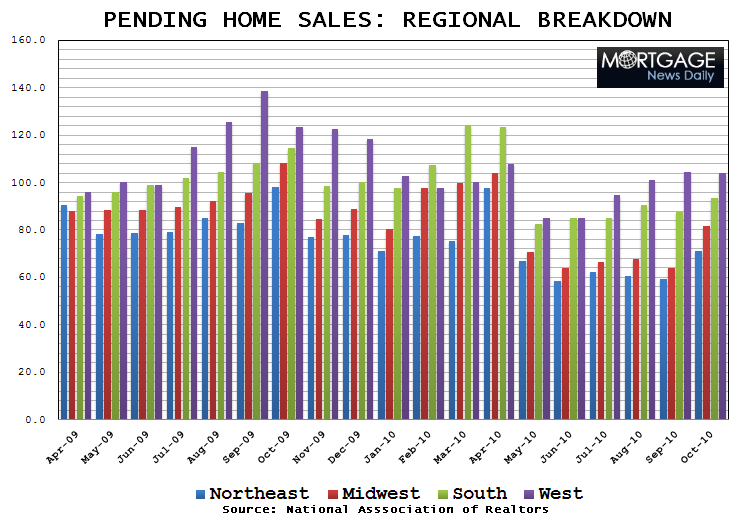

The PHSI in the Northeast jumped 19.6 percent to 71.3 in October but is 27.3 percent below the tax credit peak in October 2009. In the Midwest the index surged 27.3 percent in October to 81.7 but is 24.8 percent below a year ago. Pending home sales in the South rose 7.1 percent to an index of 93.8 but are 18.4 percent below October 2009. In the West the index slipped 0.4 percent to 104.3 and is 15.6 percent below a year ago.

Expanding a bit on regional activity...

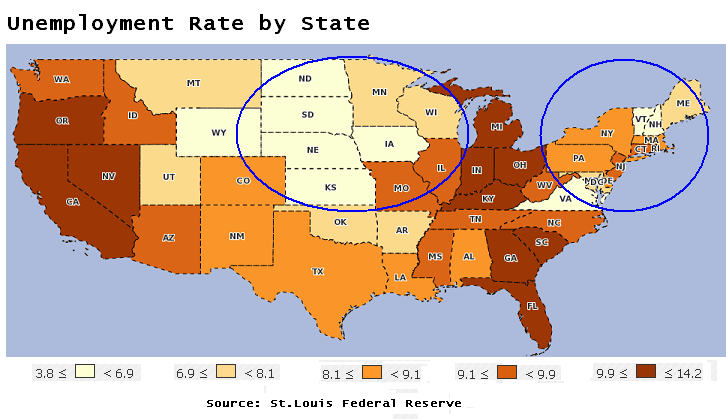

The Northeast and Midwest saw the largest upticks in Pending Home Sales activity in the month of October. Below is a heat map illustrating unemployment rates in individual states. The two regions with the most improvement in sales contracts signed, the Northeast and the Midwest, also happen to be the two regions with the lowest unemployment rates. As the economy slowly recovers, we should expect this observation to become more relevant. I am calling it a "Segmented Recovery"....

HERE is a breakdown of Census regions.

Lawrence Yun, NAR chief economist, said excellent housing affordability conditions are drawing home buyers. “It is welcoming to see a solid double-digit percentage gain, but activity needs to improve further to reach healthy, sustainable levels. The housing market clearly is in a recovery phase and will be uneven at times, but the improving job market and consequential boost to household formation will help the recovery process going into 2011,” he said.

“More importantly, a return to more normal loan underwriting standards and removal of unnecessary underwriting fees for very low risk borrowers is needed and could quickly help in the housing and economic recovery,” Yun said. Recent loan performance data from Fannie Mae and Freddie Mac clearly demonstrates very low default rates on recently originated mortgages, much lower that the vintages of 2002 and 2003 before the housing boom.

Near term, Yun expects home sales will continue to climb from their cyclical low this past summer. “Even so, we now have some consumer concerns regarding the mortgage interest deduction, an important component in housing affordability,” he said. “Preliminary results of a new survey show nearly three out of four home owners and two out of three renters consider the mortgage interest deduction to be extremely or very important to them. Home owners already pay between 80 and 90 percent of all federal income taxes and additional tax burden would hurt them and the economic recovery, so we have a reasonable hope that it will not be changed.”

The NAR believes over-tightened underwriting regs and expensive loan level pricing adjustments are a major barrier to the housing market recovery. I will avoid the cliche "Mortgage Industry vs. Realtor" finger pointing and instead say, YES NAR, MORTGAGE PROFESSIONALS AGREE, WE'D LOVE TO SEE A LITTLE MORE COMMON SENSE IN THE UNDERWRITING PROCESS TOO. Unfortunately until the fate GSEs is determined and secondary market reform is passed down by the 112th Congress, it's hard to imagine we'll see looser guidelines or cheaper LLPAs. Fannie and Freddie's books are bloated with bad loans and REO, the FHFA has made it clear that the GSEs won't be stepping outside the box anytime soon either, and the FHA can only do so much before their balance sheet goes under a microscope again.

So maybe instead of complaining about tight underwriting guidelines and expensive LLPAs at the only game in town (GSEs, FHA, VA), the NAR should be calling out Congress to act on GSE Reform ASAP! Private funding needed!

READ MORE: Denationalizing Housing in America. Calling on the Private Sector