Interest rates are, quite naturally, the focus of Freddie Mac's November Outlook. The company's Economic & Housing Research Group looked at the potential impact of the interest rate surge since the election and what it called "the near certainty" that the Federal Reserve's Open Market Committee (FOMC) will raise the fed funds rate at its December meeting.

Over two weeks post-election the 10 -year Treasury note surged by over 50 basis points, closing at 2.35 percent on November 18. The increase was driven by higher than expected inflation and anticipation of the FOMC move -the probability of which the futures market was putting at 92 percent.

Not only has the likelihood of a December rate hike increased, but expectations for future rate increases have shifted as well. At their last press conference in September FOMC members expressed a significantly higher median expectation about the appropriate level of the funds rate. Freddie's economists said, "In recent years the FOMC median has been consistently above market expectations, and over time the FOMC expectation has drifted down towards market expectations. In November, that trend reversed with market implied expectations for the federal funds rate shifting up"

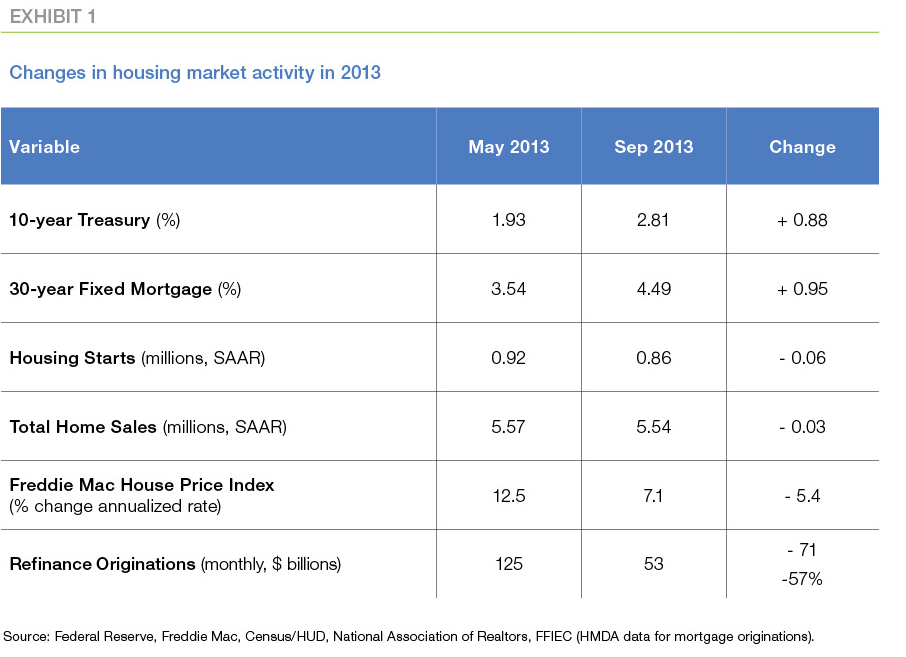

This leads Freddie Mac to conclude that interest rates will continue with modest increases and that rates through the end of next year will be significantly higher than they thought as recently as last month. To get some idea of what this might mean for the economy and the housing market they examined another period when rates rose unexpectedly, the period following the so called "Taper Talk" in 2013. During that period, mortgage rates rose a full point from 3.5 percent in May to 4.5 percent in September.

The first impact was the slowing in house price growth. Freddie Mac's house price index was showing a 12.5 percent appreciation in May; that fell to 7.1 percent in September. A slowdown had been expected but the higher rates certainly helped.

Home sales declined by about 30,000 units (at a seasonally-adjusted annual rate). Because many transactions were already in the pipeline when rates rose, it took several months before home sales responded to higher rates. By January 2014, existing home sales fell an additional 400,000 units.

While single-family housing starts didn't suffer to the extent of existing home sales, the previous double digit percentage gains stalled during this period.

The most immediate impact of the Taper Talk was a sharp downturn in refinancing activity. In months just prior, refinance origination volume averaged about $130 billion per month. Following the rate increases the volume fell more than 50 percent and only recovered after rates declined again throughout 2014 and into 2015.

The economists say these negative reactions to the rate increases in 2013 will probably be repeated in 2017 and forecast the following.

Rising interest rates will exacerbate growing affordability challenges in many markets. Housing activity began to level off even before the recent rate moves; single-family housing starts were flat for most of 2016 and existing home sales had started to lose some momentum. "Regardless, 2016 will still end up being the best year for home sales in a decade, but 2017 will be hard pressed to match those levels."

The flat construction numbers mean new home sales will only increase slightly, and existing home sales are likely to decline next year, reflecting affordability problems. Total housing starts are expected to reach 1.16 million this year and 1.26 million next year, far short of long-run demand of 1.6 to 1.7 million units. Total home sales will decline by about 220,000 units from 2016 to 2017 and while new home sales will rise, they will not offset existing home sale losses.

Home prices have been rising at about a 6 percent annual pace for the past two years. Higher mortgage rates will contribute to moderation in house price growth. Home price appreciation will probably finish this year at an average of 5.9 percent, falling to 4.7 percent in 2017.

While housing market activity will be able to weather slightly higher rates without a major correction, mortgage activity will be "crushed," particularly refinance originations. Following the Taper Talk rate increases, single-family refinance mortgage originations declined 54 percent from 2013 to 2014. This time around, Freddie Mac anticipates a decline of 53 percent from 2016 to 2017. Total mortgage originations will equal $1.5 trillion in 2017, down from $1.7 trillion in the company's October forecast.

They expect the 10-year Treasury note to finish 2016 at an average of 2.3 percent and forecast the rate in 2017 will average 2.6 percent. The 30-year fixed-rate mortgage rate will average 3.8 percent in 2016 and 4.2 percent through 2017.

Freddie Mac's economists also have forecasts for the economy outside of housing.

- Economic growth will improve with some sort of fiscal stimulus early in the year, probably one including a mix of infrastructure spending and tax cuts. This should lead to higher growth than predicted earlier. This, however will be offset by rising rates, resulting in only a 1.9 percent increase for the entire year.

- Inflation, which has been ticking higher recently will continue to do so. The Consumer Price Index will average 2.2 percent next year.

- Labor markets will hold steady. The recent slower pace of hiring is consistent with full employment and the unemployment rate should reach 4.7 percent by the fourth quarter of next year.

- The recent increases in interest rates are likely to stick, but absent some major shock or shift in economic policy will probably not go much higher. Freddie Mac expects FOMC to act in December but while the Fed held off increasing rates for most of a year after doing so in 2015, they probably won't repeat this pattern in 2017. "With the labor market at full employment and inflation showing signs of picking up, we anticipate the FOMC will move more than once in 2017 pushing short-term interest rates higher, with the 1-year Treasury rate reaching 1.5 percent by the fourth quarter of 2017."