When it comes to mortgage risk there is a lot of good news. Sam Khater, CoreLogic's Deputy Chief Economist says in the current issue of the company's MarketPulse that underwriting remains tight compared to the early 2000s and serious delinquencies among recent originations are at a 20 year low. Risk factors such as negative equity and home prices are moving in the appropriate directions and risk as reflected in foreclosure starts and distressed sales have decreased. Cash sales remain elevated, lowering overall leverage and the economy continues to improve and the labor market to tighten.

That said, Khater warns that there are some worrisome signs - red flags for risk.

The percentage of what he calls "scratch and dent" loans - loans previously more than 60 days delinquent but since cured, remains at 12 percent of active loans - about 5.5 million units - down from a peak of 15 percent in late 2011, but well above the 5 percent level of normal times. These loans are also indicative of a second risk factor. Most of that damaged merchandise was originated between 2005 and 2008 and this vintage accounted for 62 percent of foreclosure starts this past July. For comparison, loans originated prior to 2003 accounted for 10 percent. As Khater says, these legacy loans "are the bad gifts that keep giving."

The persistence of legacy loans in driving foreclosures a decade later Khater says indicates how sensitive mortgage market performance is to underwriting decisions made years earlier even in an otherwise healthy economy. "Clearly, this means that a large segment of mortgage loans remains very sensitive to the economy and home prices"

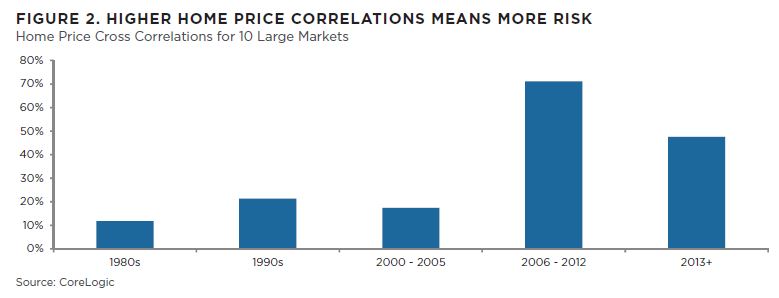

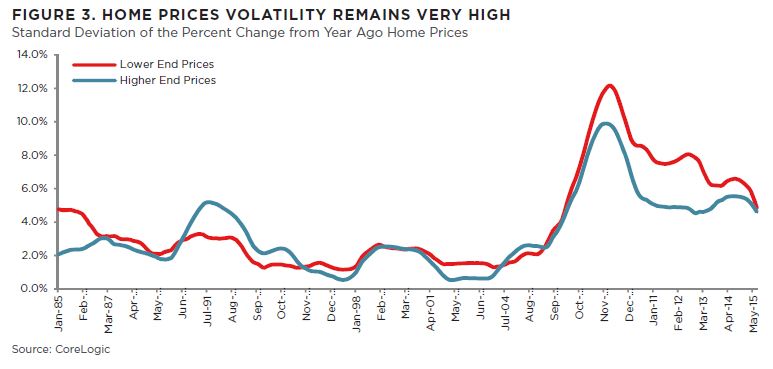

Home prices are another risk factor, he says. The national market is becoming unaffordable, price volatility is elevated, and home price cross correlations nationwide remain quite high. The home price to rent ratio is high and has been increasing since 2012. Home prices are disproportionately skewed toward the lower end of the housing price spectrum. At the lowest end, 75 percent or less of the median sales price, prices are growing by more than 10 percent. Khater says this accelerated growth was partially driven by the cut in FHA annual premium despite existing tight housing inventories.

Home price cross correlations and price volatility are high although their relationship to risk is not heavily researched. Cross-correlations for 10 large markets are currently three times higher than in the three prior decades. Higher home price correlations increase home price volatility and risk of national booms and busts because the benefits of geographic diversification is reduced. Defined by the standard deviation of the inflation-adjusted three-year moving average of price changes, volatility is currently twice the historic average.

Khater says while the industry must watch for traditional risk red flags like employment and home price growth it must also look for less traditional ones like the performance of legacy loans, mortgage transition rates, and home price volatility to get an early reading on where the market is heading.