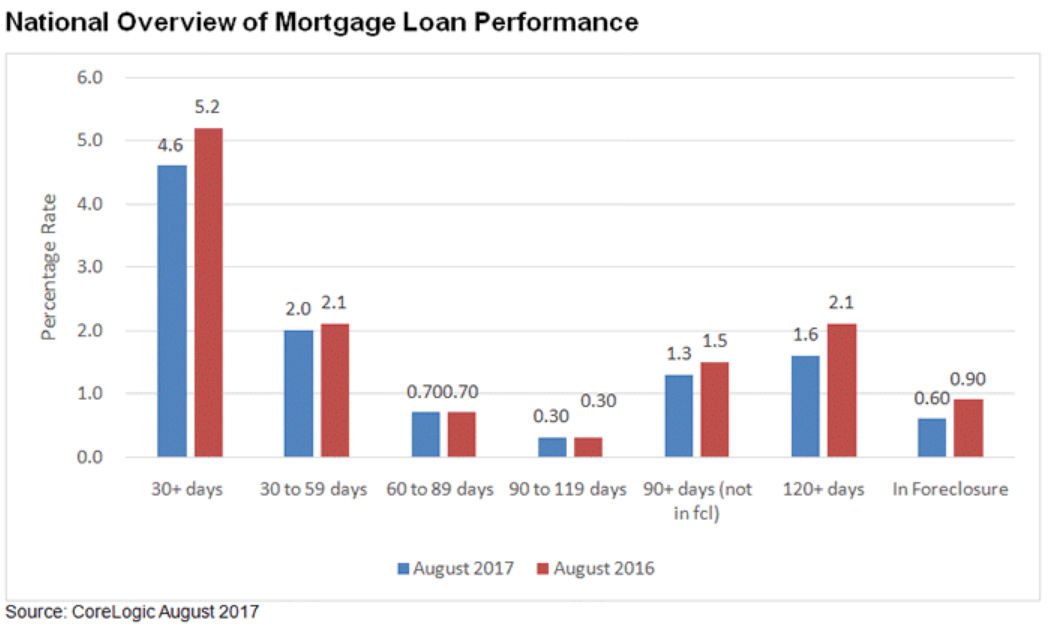

To no one's surprise, measures of mortgage distress, including delinquencies, serious delinquencies, and foreclosures, were down again in August, with many metrics falling into fractional percentage territory. According to CoreLogic's Loan Performance Report for the month, the overall delinquency rate, mortgages 30 or more days past due, fell 0.6 percentage points from August 2016, to 4.6 percent.

Within that number, the earliest delinquencies, those that have missed one payment, represented 2.0 percent of all mortgaged homes, down from 2.1 percent year-over-year, and the share of loans 60 to 89 days past due was unchanged at 0.7 percent.

The serious delinquency rate, loans more than 90 days past due, was 1.9 percent, an 0.5 percent decline year-over-year. It was the lowest incidence of serious delinquencies since October 2007 when the rate was also 1.9 percent. Alaska posted the only annual increase among the states.

"The effect of the drop in crude oil prices since 2014 has taken a toll on mortgage loan performance in some markets," said Dr. Frank Nothaft, chief economist for CoreLogic. "Crude oil prices this August were less than half their level three years ago. This has led to oil-related layoffs and an increase in loan delinquency rates in states like Alaska and in oil-centric metro areas like Houston." The delinquency rate for the Houston area was up 0.5-point year-over-year, although the serious delinquency rate ticked down slightly.

As of August 2017, the foreclosure inventory rate, which measures the share of mortgages in some stage of the foreclosure process, was 0.6 percent, down from 0.9 percent in August 2016. This was the lowest foreclosure inventory rate for the month of August since August 2006 when it was 0.5 percent.

Mississippi had the highest delinquency rate of any state, 8.4 percent, followed by New York and New Jersey at 7.0 percent. The rates in the last two appear driven by their foreclosure inventories which were the highest in the country at 2.1 and 1.8 percent respectively. Both are judicial process states and have long had huge backlogs of foreclosures. Mississippi's inventory rate, on the other hand, was only 0.5 percent.

CoreLogic says measuring early-stage delinquencies is important for analyzing the health of the mortgage market as is tracking transition rates. The latter indicate the percentage of mortgages moving from one stage of delinquency to the next. The share of mortgages that transitioned from current to 30-days past due was 0.9 percent in August 2017, the same as a year earlier. By comparison, in January 2007 just before the start of the financial crisis, the current-to-30-day transition rate was 1.2 percent and it peaked in November 2008 at 2 percent.

"Serious delinquency and foreclosure rates are at their lowest levels in more than a decade, signaling the final stages of recovery in the U.S. housing market," said Frank Martell, president and CEO of CoreLogic. "As the construction and mortgage industries move forward, there needs to be not only a ramp up in homebuilding, but also a focus on maintaining prudent underwriting practices to avoid repeating past mistakes."