The Mortgage Bankers Association, American Bankers Association, and six other trade groups representing the financial services sector sent a letter Wednesday to Obama Administration policy makers calling for a delay in considering improved disclosures for mortgage borrowers under the Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA).

The letter, addressed to Treasury Secretary Tim Geithner, Housing and Urban Development Secretary Shaun Donovan, and Federal Reserve Chairman Ben Bernanke expresses concern that the government's intention to combine two disclosures into a single integrated document may be one change too many for financial institutions to manage in the current environment.

The writers applaud the actions of the Federal Reserve and HUD to improve disclosures to borrowers and states that integrating them into a single document will greatly increase transparency and consumer understanding of the mortgage transaction, but states that the government must realize that the initiative, which is currently being managed by Special Advisor to the President, Elizabeth Warren and Treasury staff, is coming "in the midst of a surfeit of proposed and final regulations that require fundamental changes to the mortgage finance business model and a generation of systems which support it."

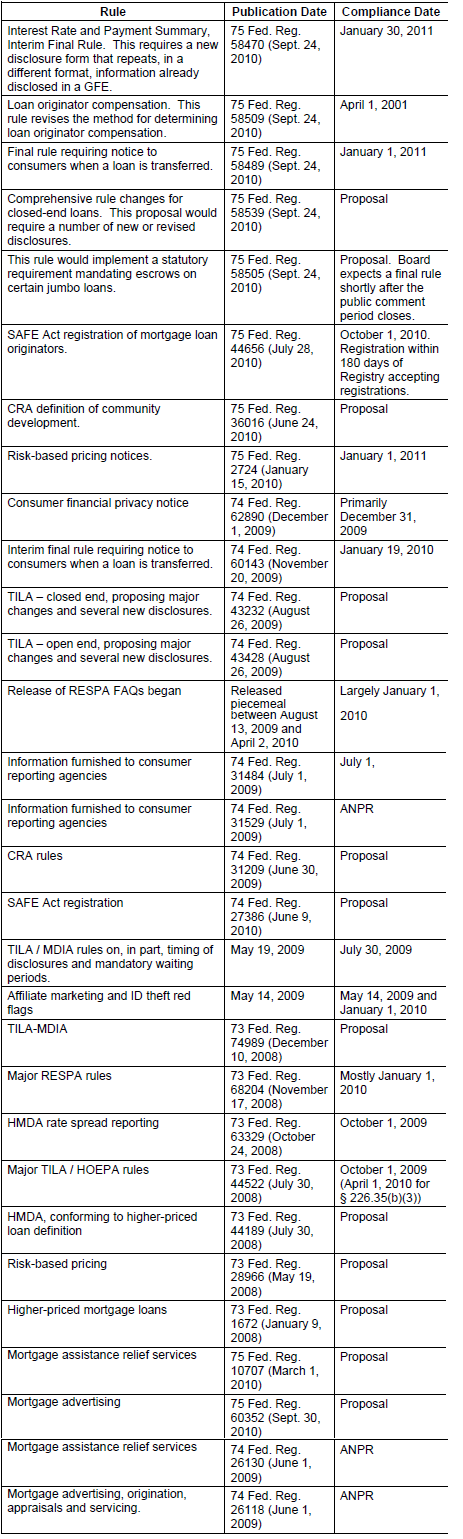

Attached to the letter is a list of 28 rules affecting TILA, RESPA, loan officer compensation, the SAFE Act and other regulations that are in various stages ranging from proposal to comment to upcoming compliance deadlines. The associations state that these "have stretched thin the compliance capabilities of financial institutions. If these efforts are not coordinated, they state that the cumulative burden will "threaten the availability of housing finance options, and it will also be difficult for stakeholders to provide input to these changes.

The letter stresses that the groups, which also include the American Financial Services Association, Community Mortgage Banking Project, Consumer Bankers Association, Consumer Mortgage Coalition, Housing Policy Council, and Independent Community Bankers of America, view integration of RESPA and TILA Disclosures as a first priority and that if they were made truly simpler and combined, or at least made harmonious and complementary, and if they were presented along with other essential information in a coordinated manner at rational times in the process, consumers would be better equipped to navigate the market, understand their mortgage and settlement costs, and shop intelligently to meet their financing needs.

However, the group complained that HUDs Good Faith Estimate and HUD-1 Settlement Statement became effective on January 1; the Federal Reserve made changes to its TILA disclosures which have not yet become effective, and has now issued 1,000 pages to further amend them. Each of these have required "extensive review and an enormous investment of time by stakeholders to comment, diverting energy that would be better spent on RESPA-TILA integration" The letter further states, that "Considering that comments are due December 23, and that to comment effectively the proposed changes must be considered in the light of the RESPA-TILA proposals to come, a public announcement of a postponement is warranted" and the disclosure provisions could and should await the RESPA-TILA integration process.