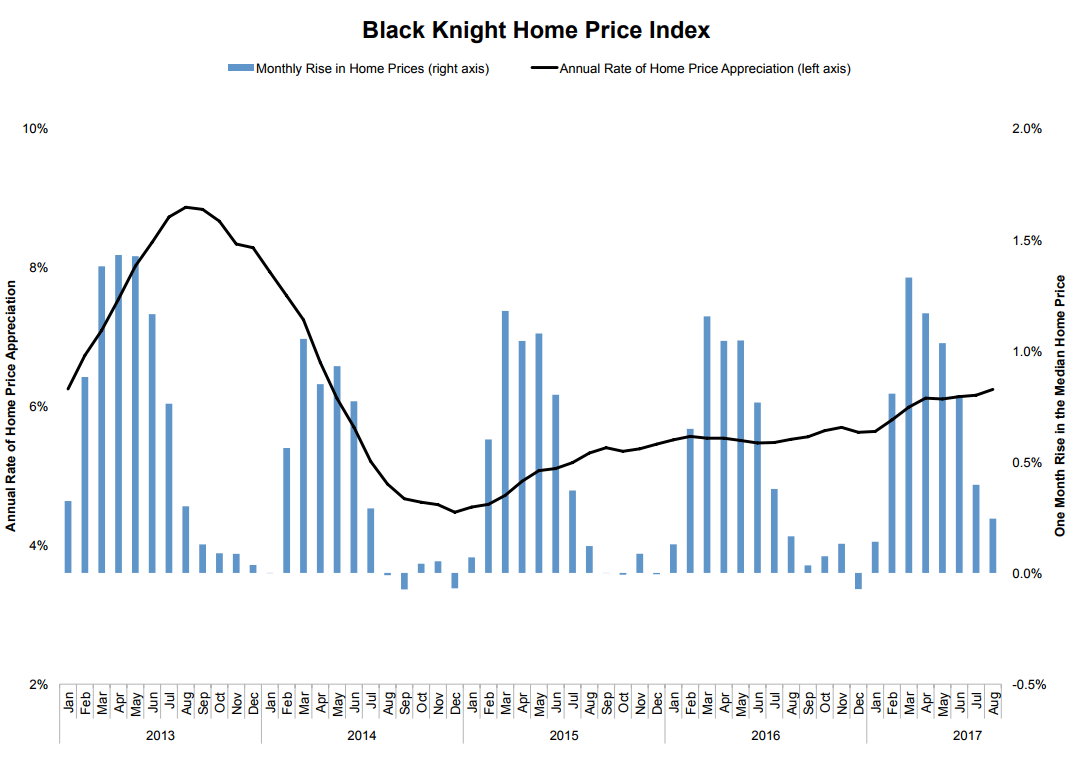

During the first eight months of 2017, home prices increased at the fastest clip than any equivalent time period since 2013. Black Knight Financial Services said late last month that there had been just over 6 percent in appreciation in its nationwide Home Price Index (HPI) over that period, a quarter point gain in August alone. The median home price for the country as a whole is up $16,000 since the beginning of the year.

In the current edition of its Mortgage Monitor, released on Tuesday, the company takes another look at the pattern of price gains and presents some scenarios as to how affordability could be affected if the rapid increases continue.

Looking at gains with a slightly wider lens, from August 2016 to August 2017, the national increase is 6.24 percent, the highest annual rate since April 2014. The West has led the rest of the country, with one state, Washington, nearly doubling the national rate with 12.2 percent year-over-year appreciation. Nevada was not far behind; its HPI was up 11.1 percent. Nevada also saw the greatest degree of acceleration; +4.3 percentage points over 12 months, from an annual rate of 6.8 percent in August 2016. The acceleration in price changes for the nation as a whole over the same time period was 0.72 point.

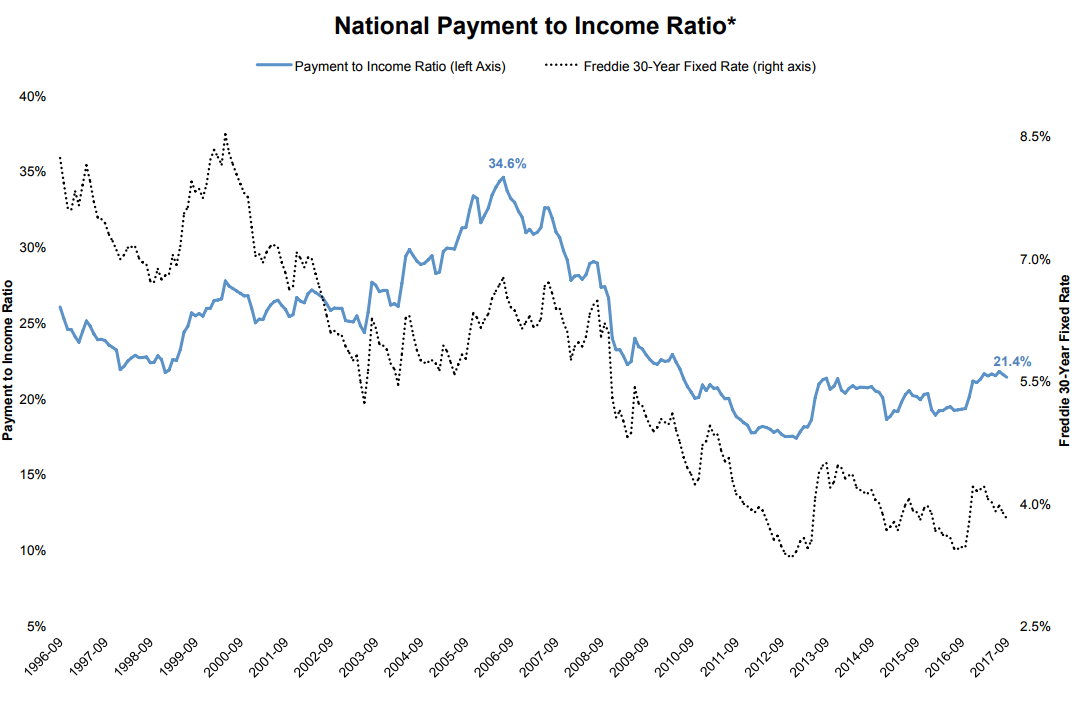

The payment-to-income ratio is the share of the median income needed at any point in time to make monthly mortgage payments on the median home given the prevailing 30-year fixed mortgage rate. Since March, interest rates have declined by 40 basis points, bringing an average mortgage payment on a median priced home down by about $50, but price increases over that period have gobbled up much of those savings. Since September 2016, when the average interest rate was 3.94 percent, the median home price has gone up $100.

As of

September 2017, the payment to income ratio was 21.4 percent, close to a

post-recession high. Yet, Black Knight notes that, when borrower incomes and

interest rates are taken into account, affordability remains favorable compared

to other periods. The ratio from 1995 to 1999 was 24.2 percent and it was 26.2

percent from 2000-2003, just prior to the run-up to the 2006 price peak.

"Rising home prices continue to offset the majority of would-be savings from

recent interest rate declines, which has kept home affordability near a

post-recession low," said Ben Graboske, Executive Vice President of Black

Knight Data and Analytics. "That being

said, when viewing the market through a longer-term lens, affordability across

most of the country still remains favorable to long-term benchmarks."

"In looking at the affordability landscape across the country, we certainly see

varying levels of affordability in each market compared to their own long-term

benchmarks," Graboske explained. "But, by and large, the overall theme is that

affordability in most areas, while tightening, remains favorable to long-term

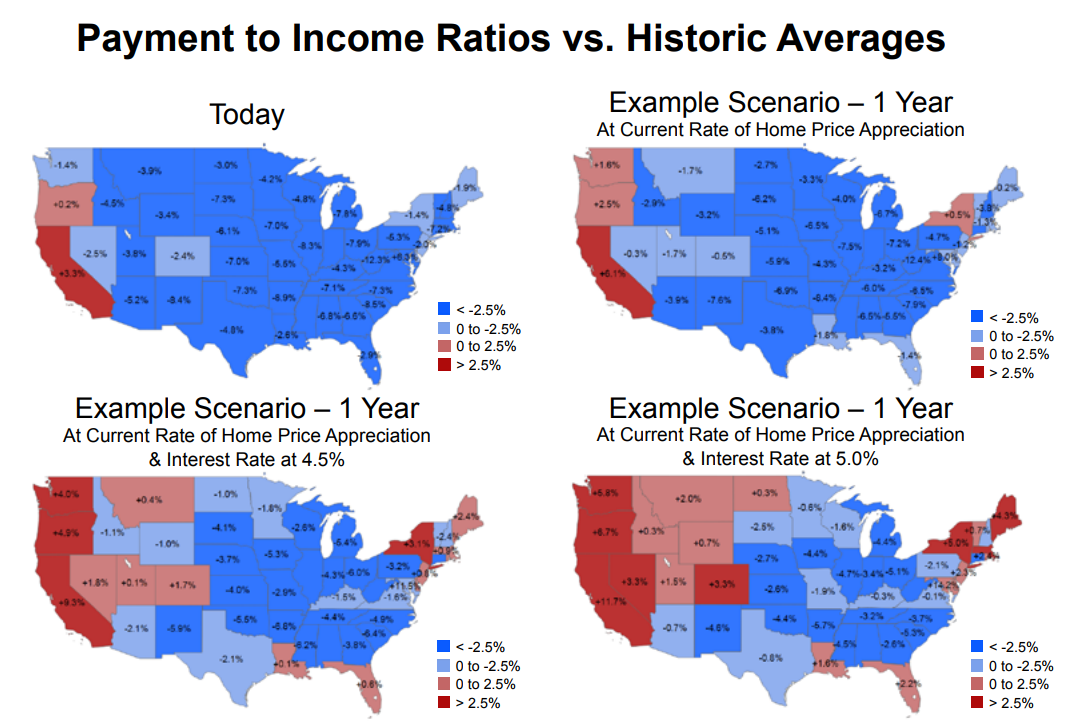

norms." When looking at state-level data, payment-to-income ratios in 47 of 50

states remain below their 1995-2003 averages. Only Hawaii (+4.3 percent),

California (+3.3 percent), Oregon (+0/2), and Washington, D.C., have higher

payment-to-income ratios today than their longer-term benchmarks.

Graboske says one certainly could ask how long the current rate of home price appreciation can continue. Even with Black Knight's HPI accelerating from 5.6 percent to 6.2 percent over the first eight months of the year, optimistic scenarios show most states remaining below long-term benchmarks even if home prices continue to rise at current rates for another year. However, under pessimistic scenarios -- including significant increases in the 30-year fixed interest rates -- affordability could surpass long-term norms in a number of states by this time next year.

The company analyzed the payment-to-income ratio in each state against its 1995 to 2003 averages and against the nation as a whole, then projected affordability under several different price and interest rate scenarios. The current chart (September 2017), shows the national scenario where, as noted above, it requires 3.7 percent less median income to purchase the median priced homes that the historic norm.

In the first example scenario, interest rates remain consistent and prices continue to rise at the current rate at both state and national levels. In one year it will take 1.3 percent more of the median income on the national level to buy a home, and Washington and New York are added to the states where housing becomes less affordable than their norms.

Under the second scenario, where prices maintain their current level of appreciation, but interest rates increase to 4.5 percent (from 3.9 percent at the time of the analysis), the national payment-to-income ratio would rise to within 0.4 percent of its historic norm and 17 states would be above their norms.

Finally, and still keeping price increases at their current rates, a 5.0 percent interest rate would send the national rate 1.0 percent above the historic norm and push 23 states and Washington, DC above their benchmarks.

Black Knight notes that it is possible that income gains or the slowing of price increases could paint a quite different picture, providing a favorable picture of affordability. Still, given current conditions, the payment-to-income ratios in many parts of the country bear watching, especially as the rate of price appreciation has been held level throughout each of the scenarios pictured.