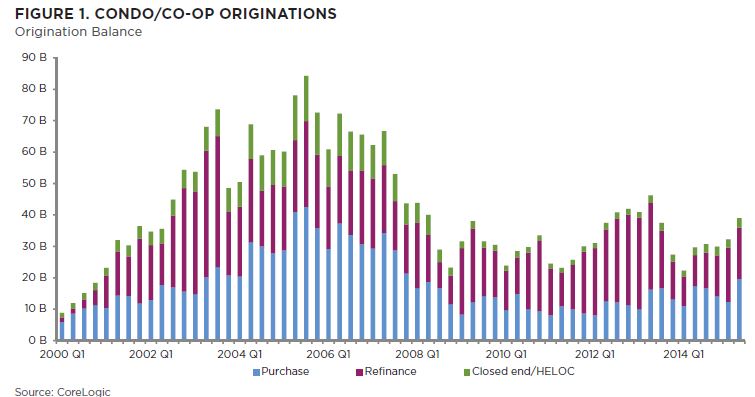

There was a sizable increase in mortgage originations for condominiums and cooperatives in the second quarter of 2015. Purchase applications rose significantly but several other factors played an ever strong role.

CoreLogic, in their October Market Pulse said that mortgage originations for the two property types rose 31 percent compared to the same quarter in 2014 - from $29.7 billion to $39 billion. Refinancing was responsible for much of the surge, rising by 65 percent in dollar volume while Home equity lines of credit (HELOCs) gained 29 percent. Purchase loans did well, gaining 13 percent to $19.6 billion, the highest level since the end of 2007 when the number hit $21.3 billion.

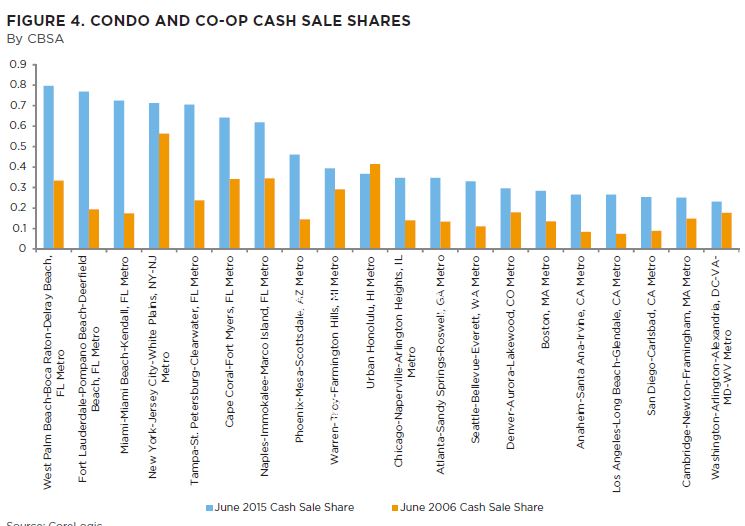

There was another factor in play, CoreLogic Senior Economist Kristine Yao says, and that was a drop in cash sales, which are frequently an indication of investor purchases. All cash sales still made up a significant share of condo and coop purchases at 47 percent in June, the last month of the quarter, but this was down from 50 percent a year earlier and a peak of 63 percent in February 2012. The cash share of these sales has fallen on an annual basis every month since that peak. In the pre-housing crisis years cash sales generally averaged 27 percent of the condo market.

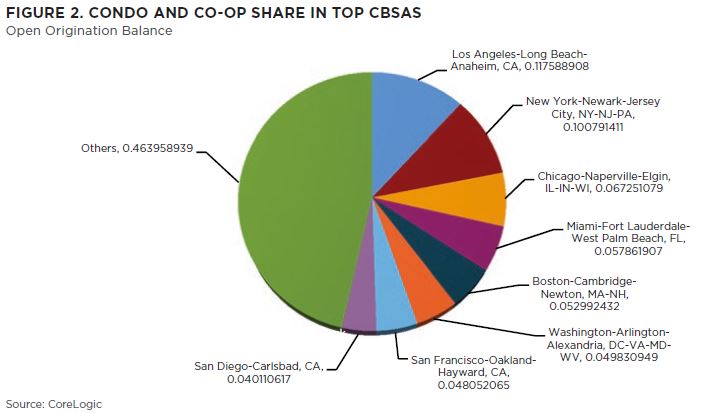

Condo and coops are concentrated in urban markets and even more concentrated within those markets. Yao says about 50 percent of existing mortgages on these properties are located in just eight Core Based Statistical Areas (CBSAs). As far as recent originations, during the 12 months that ended in June nine of the top 25 counties in dollar volume were in California, led by Los Angles. That county had new condo/co-op loan originations of $12.2 billion, and represented 9 percent of the national market. Cook County, Illinois (Chicago) was second with $7.4 billion. Seven counties among the 25 had year-over-year growth of 25 percent.

Some condo markets have been affected more than others by cash sales, with shares still running well above national averages such as the West Palm Beach-Boca Raton-Delray Beach area where the June 2015 cash share was 80 percent. CoreLogic says these high share areas could result in the largest opportunities for lending. "However, tighter eligibility requirements on condo and co-op lending after the recent financial crisis have made it more challenging to qualify for a mortgage. Building efficiencies in the loan approval process to make housing credit more accessible and affordable to consumers will be a critical factor in the continual recover of the condo and co-op mortgage industry.