In an early article, we summarized the first part of a new report on America's aging population, especially as related to homeownership, published by the Harvard Joint Center on Housing Studies. The second part of the report deals with the elderly's housing and financial condition.

Since the turn of the century, incomes have grown much faster among retirement-aged households than those of pre-retirement age. However, since the Great Recession most of the gains have gone to the highest-income households in each age group. The median income for the top 10 percent of earners in the 50 to 64-year group has risen nearly twice as fast (15 percent) as among the bottom 10 percent, a record median of $204,000 in the first case, $14,400 in the second. Meanwhile, the median for the highest earners in the 65 and over age group was up 22 percent while that of the lowest group declined by 4 percent.

This growing inequality reflects, in part, a trend toward later retirement. Twenty-seven percent of adults 65 to 74 were still working in 2018 as well as 9 percent of those over 75. The stock market boom has helped feed the disparities, driving up the wealth of higher earners who are more likely to invest, and since Social Security benefits are based on past earnings, income differences among older Americans are, to some extent, a continuation of those that existed earlier in life.

Homeownership rates also vary across older age groups. In 2018, 78.5 percent of those over age 65 owned their primary residence, the highest for any age group, but this is down from a peak of 81.1 percent in 2012 while the rate among the next younger group has dropped 6.2 percent from the rate of that group in 2004 to 74.2 percent. Thus, households in this age group are approaching retirement with lower homeownership rates than those of the previous generation at the same age.

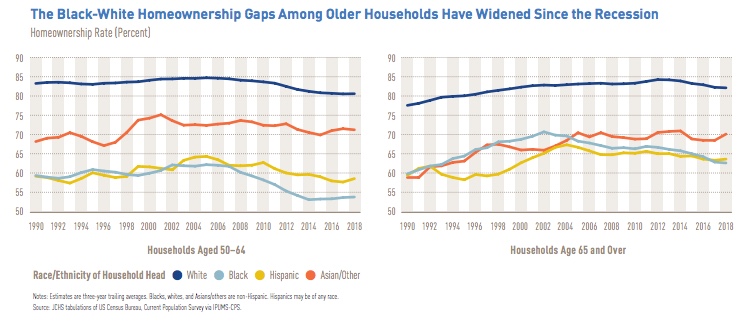

In addition, racial and ethnic disparities have widened. The black-white homeownership gap among older households reached a 30-year high of 19.4 percent in 2018 and the white-Hispanic gap was 18.4 percent. Among the pre-retirement group the relative gaps were 27 and 22 points.

These inequalities are crucial because homeownership provides greater housing security, predictable housing costs and more opportunity to build wealth than does renting. The median home equity of homeowners over age 65 was $143,500 in 2016, leading to net worth of $319,200. By comparison, a renter of the same age had net worth of $6,700. This disparity holds true for the next younger group as well, even for owners and renters with comparable incomes.

Older renters are particularly vulnerable when facing an urgent situation such as needing in-home assistance. Only a quarter of renters over age 65 have at least $5,000 in cash savings compared with two-thirds of their homeowning peers. For context, the median cost of 14 hours per week for a home health aide would total $16,000 per year.

Seniors are also increasingly debt-burdened, with mortgages as well as other debt. Three decades ago, most older homeowners were without a mortgage - about a quarter of those 65 to 79 and 3 percent of those over that age had any housing debt and where they did, the median was under $20,000. In 2016 46 percent and 26 percent of those two age groups had mortgage debt with median balances of $77,000 and $43,000. Between 2007 and 2016 the share of households in the older group with mortgages jumped by 16 points. The percentages of minority households with mortgage debts were at least 10 points higher in each age and ethnic category than in white households.

Admittedly, some of the increase in mortgage debt may reflect the recent low interest rate environment, with homeowners preferring to keep paying a mortgage to free up funds for other investments. Many have probably refinanced, extending their mortgage terms, others simply lack the resources to pay off their mortgages.

Surprisingly the number of older households carrying student debt has more than doubled, to 16 percent, since 2001 and the median amount increased from $11,000 to $18,000. Over the same period households with credit card balances have gone up 11 points to 35 percent, and the median debt has doubled to $2,400.

The Joint Center report says carrying such debt has detrimental effects on the health and well-being of older adults and can result in housing and food insecurities. It can also result in mental and physical problems and may mean working well past the traditional retirement age.

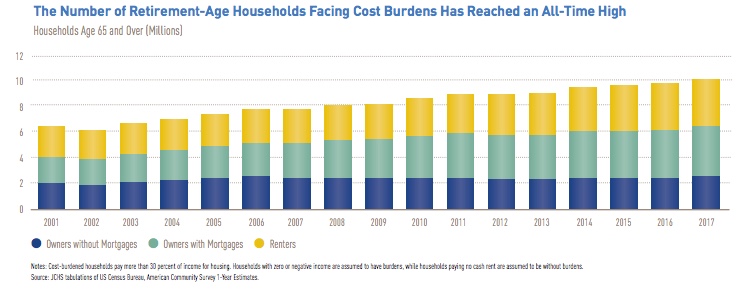

Not surprisingly, it also means a dramatic increase in the number of cost-burdened households - those over the age of 65 who pay more than 30 percent of their income for housing. That number increased by more than 200,000 just between 2016 to 2017, to a record high of 10 million. Half of these households were severely cost-burdened, paying more than half of their income for housing. Though their numbers increased along with the older population, the share remained essentially flat at about a third. Another 10 million households in the preretirement age group are also cost-burdened, again half of them severely so, although their numbers were down slightly in 2017.

Renters are even more cost-burdened - at 54 versus 26 percent - although their numbers are smaller because of the high ownership rate among those over the age of 65. Older renters with low incomes are particularly hard hit - 72 percent of those with incomes under $15,000 and 50 percent of those with incomes between $30,000 and $45,000 had a housing burden of at least 50 percent. The share of cost-burdened elderly increases with age and those living in major metropolitan areas are especially hard hit.

Heavily cost-burdened individuals may cut back on other expenses, including those essential to health and well-being and the report found they often spend only half as much on food and on housing than those who are not burdened.

These problems have led to an increase in homelessness among older adults; it jumped from 23 to 34 percent for those over the age of 50 between 2007 and 2017. The number over the age of 62 living in shelters or transitional housing rose by 69 percent over that decade to 76,000.

Older veterans have been hard hit. HUD reported that 19.2 percent of homeless veterans were over the age of 62 in 2017 and there were an additional 22,700 counted as sheltered along with 49,900 in the 51 to 61 age group.

Despite these problems, the share of income-eligible older adults (an estimated 4.7 million) receiving federal rental subsidies declined from 36 to 34 percent between 2013 to 2015. This means 3.1 million of those over the age of 62 "had to fend for themselves on the private market." Of this group, 19 million had severe cost burdens and/or lived in severely inadequate units.

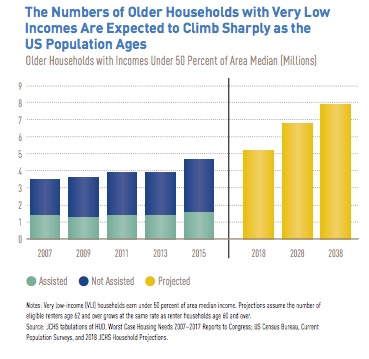

The Joint Center says this shortfall will only get worse over the next 20 years with the number of very low-income adult households expected to grow from 5.3 million in 2018 to 7.9 million in 2038. Continuing to serve only a third of them would add 2.4 million to the ranks of low-income older adults without affordable housing.

Studies have shown that failing to meet housing needs means greater expenditures are needed for other supportive services including Medicare. Also, where older adults have housing that connects them with shared meals, transportation, and meets other needs, they are able to live independently for longer.

The report concludes that the growth of the nation's older population presents a host of housing challenges; the number needing affordable, accessible housing and in-home services will soar. Transportation and opportunities for social interaction will also be critical to an ability to remain independent. Just as concerning is the growing economic inequality within the older population. A record number are cost-burdened and will have few affordable housing options as they age.

Providing the types of housing and neighborhoods needed by an aging population will depend on concerted action by both the public and private sectors. The Joint Center says the time for more comprehensive and innovating policies in the design, financing, construction, and regulation of housing and provision of community services is now. "The quality of life and well-being of a third of U.S. households depends on it."