Housing industry players have decried the absence of first-time homebuyers and the negative impact they have had on the housing recovery. Fannie Mae's Economic and Strategic Research team, in the most recent edition of Housing Insights, says that this absence, which has long been a result of lack of demand due to financial constraints, is now shifting to a supply issue.

As the labor market has improved and wages to recover and even though tight credit may still be an obstacle recent attention has shifted to the lack of available starter homes as an impediment to first-time buyer participation. Fannie Mae's analysts see several issues involved in this shortage.

The first frequently cited issue is the "subdued construction of modestly priced houses. Another factor, perhaps not as frequently noted, is the conversion of owner occupied single-family homes to rental properties during the housing bust and recovery. To explore the shift toward renting, Fannie Mae's analysts look at net changes in the number of starter homes since the start of the housing downturn. They define these homes as single- family detached units with less than 2,000 square feet (sf) of floor area and either owner- or renter-occupied. They chose this measure as the Census Bureau's American Housing Survey (AHS) does not provide information on prices.

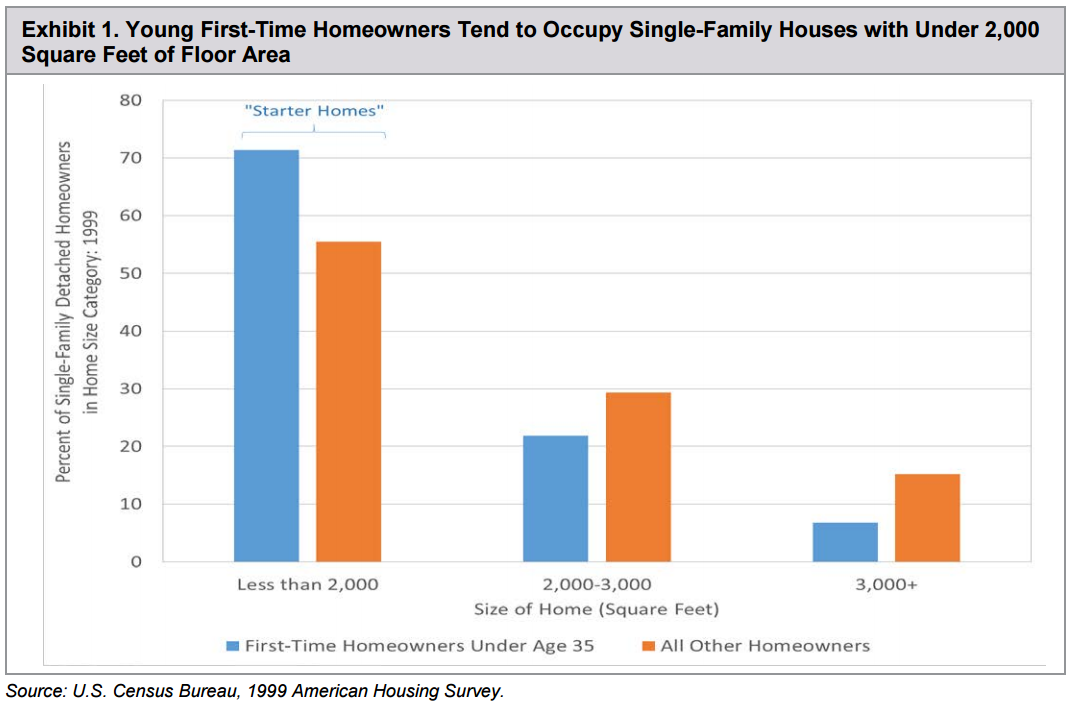

Housing Insights looks at the square footage distribution of single-family detached homes inhabited by first-time homeowners under the age of 35. Prior to the housing bubble of 2004-2006 71 percent of homes occupied by these buyers contained less than 2,000 sf. while 55 percent of other homeowners occupied homes of this size according to AHS. The National Association of Realtors reports that 59 percent of primary residences purchased by first time buyers between July 2014 and July 2015 were under 2,000 sf compared to 32 percent purchased by repeat buyers.

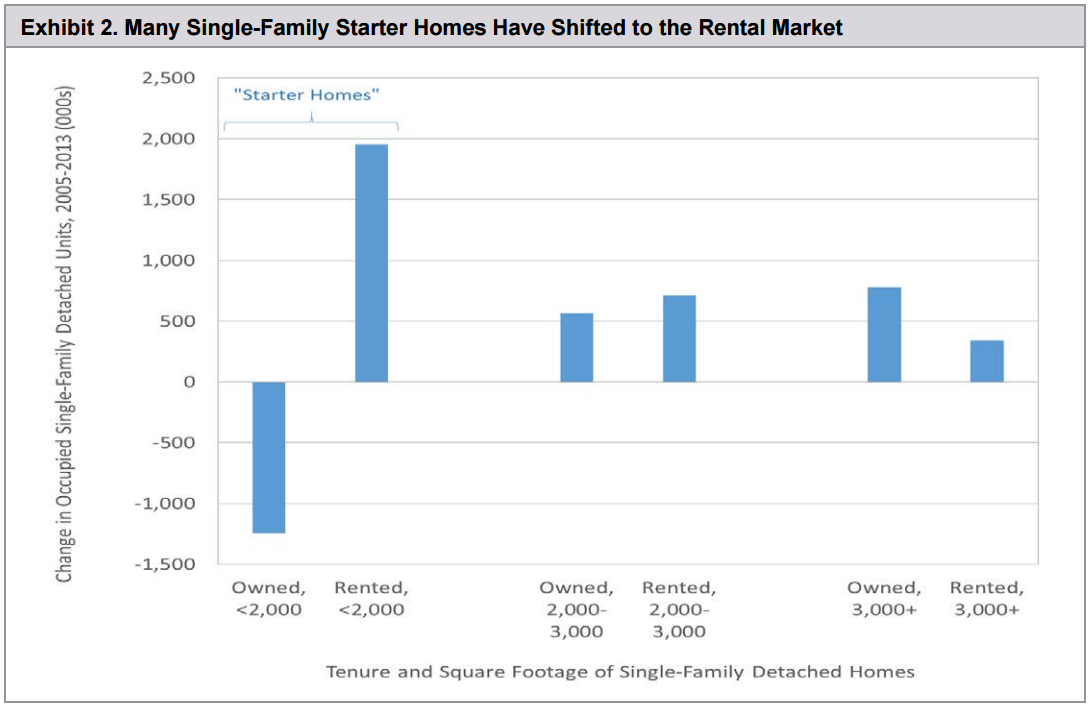

The growth of single family rentals is one of the defining characteristics of the housing bust and recovery with the number of such units increasing by approximately 3 million units, one half of the total growth of rental stock. Much of this growth came from the starter home market. The number of renter-occupied starter homes expanded by nearly 2 million between 2005 and 2013, accounting for two-thirds of the growth in all single-

family detached rentals. During the same period, the number of owner-occupied starter homes fell by more than 1 million and the number of owner-occupied homes of more than 2,000 sf grew by more than 1 million units, half of which were larger than 3,000 sf.

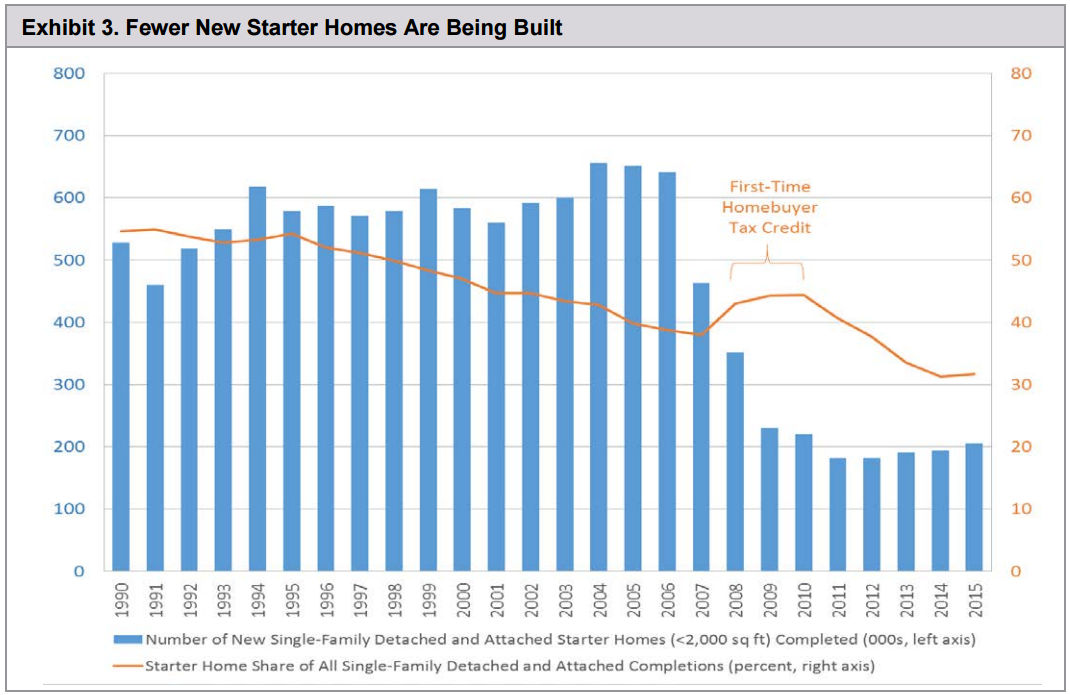

Home builders are not stepping up to fill the gap, instead building increasingly larger homes. The share of new single-family homes, attached and detached, smaller than 2,000 sf has dropped from 40 percent in 2005 to 32 percent in 2015. In 2005, home builders completed about 650,000 single-family detached and attached homes of less than 2,000 square feet (see Exhibit 3). By 2011, starter-home completions had plummeted to less than 200,000 units per year, and have since shown little sign of rebounding.

Fannie Mae concludes there was an upside to the conversion of single-family homes to rentals at the height of the housing crisis. Investors helped stabilize home prices, removed excess vacancies from the market and absorbed some of the millions of foreclosed homes. However, "While this adjustment played an important role in the housing recovery, it might also have contributed to the set of challenges facing potential first-time homebuyers by reducing the supply of starter homes available for owner- occupancy. In turn, the tight starter home supply and associated rapid price gains in the lower tiers of the home sales market are reducing first-time home buyer affordability."