While it sometimes seems as though Americans live online, there is still apparently one area where they still value human contact. A recent survey conducted by Fannie Mae found borrowers continue to put a lot of trust in their real estate agent and their mortgage lender.

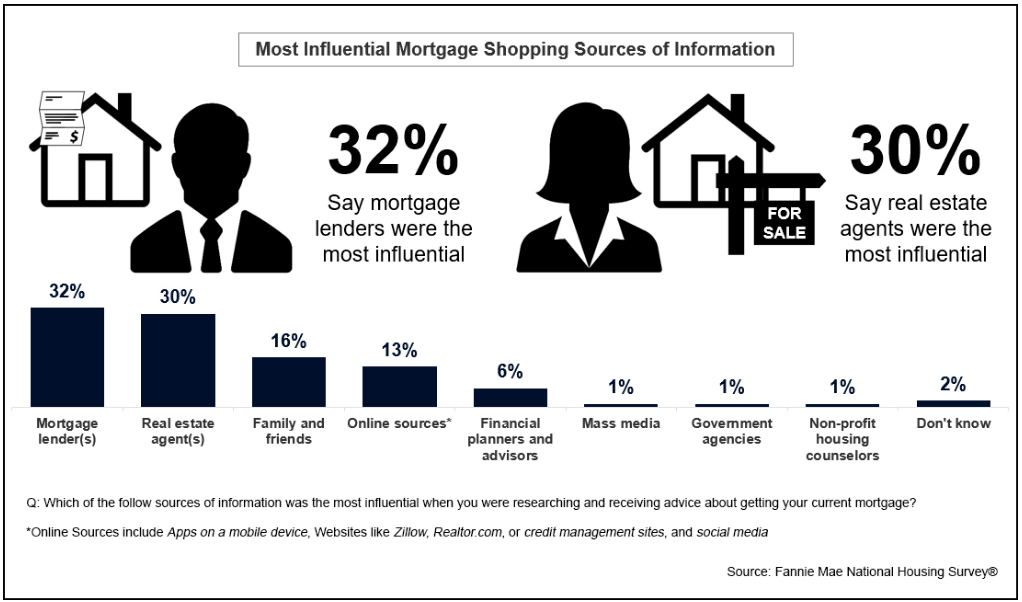

The survey, conducted with borrowers who had purchase mortgages originated in 2016 in the Fannie Mae book of business, found that homebuyers relied on a variety of information sources when shopping for a mortgage. These included friends and family, financial planners, government agencies, mass media and non-profit housing counselors. However, when asked which were the most influential, borrowers most often cited, in fact at nearly double the rate of the next closest response, were mortgage lenders at 32 percent, with real estate agents coming in only slightly lower.

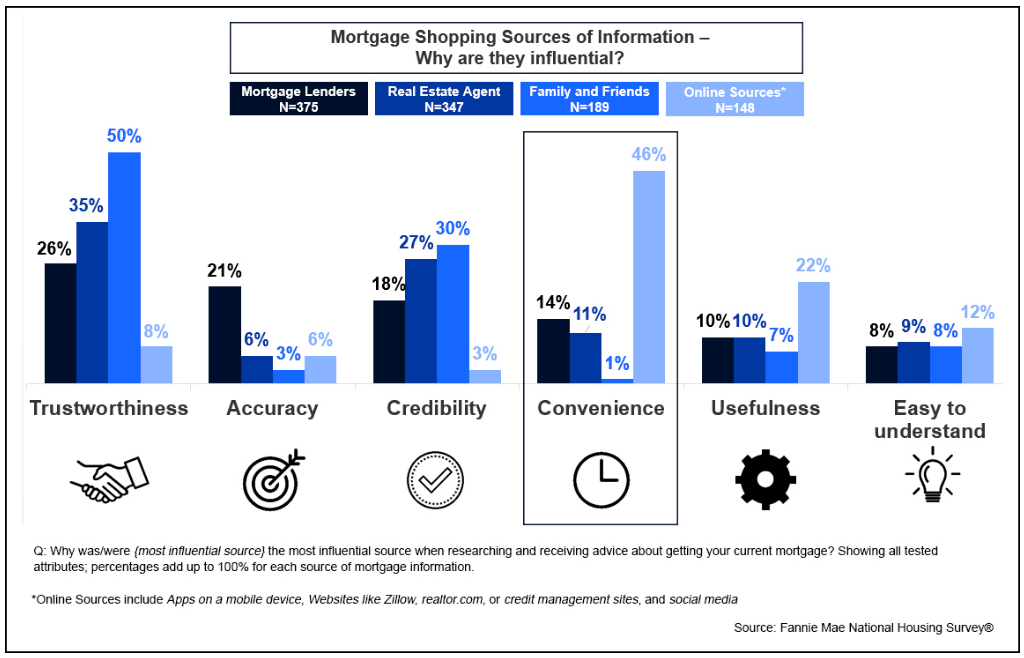

Steve Deggendorf, Fannie Mae's Director of Market Insights Research, reports that borrowers saw mortgage lenders, real estate agents, and family and friends as more trustworthy and credible than online sources. The latter however, are viewed as much more useful and convenient sources than personal interactions.

The Millennial generation, those between the ages of 18 and 34, are assumed to be moving into an increasingly mobile-data-driven world, but Deggendorf said they report using mortgage lenders, real estate agents, online sources, and family and friends with similar frequency as sources of information for mortgage shopping as the other age groups. They are also the most frequent users of real estate agents and online sources compared with the total sample of recent borrowers and say their most influential sources of information are mortgage lenders, real estate agents, and family and friends, not online sources.

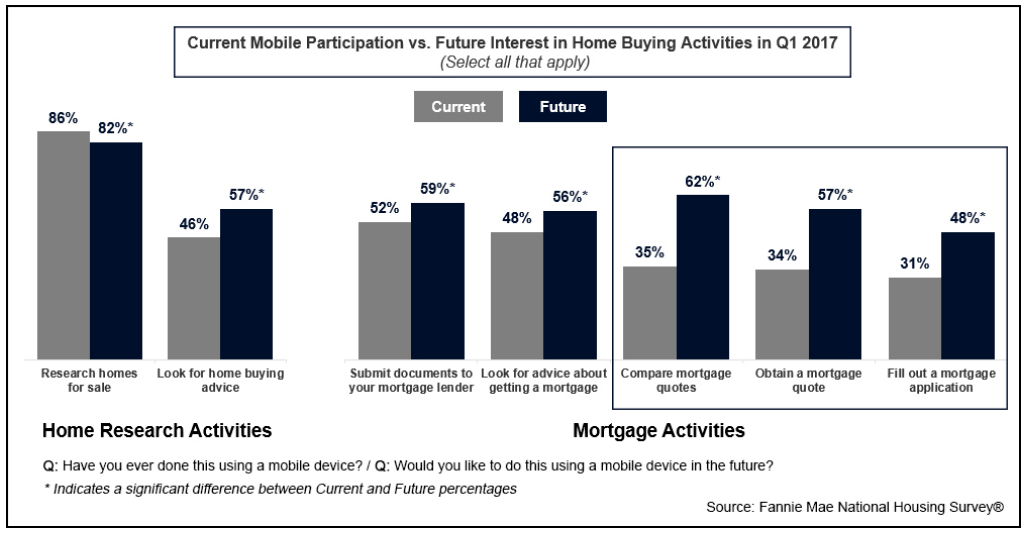

Consumers of all ages do use on-line, and increasingly their mobile sources for mortgage information. Fannie Mae asked the borrowers if they had ever used mobile devices to gather mortgage information, and if they would like to do so in the future. Responses pointed to a growing interest in performing nearly all the functions of the mortgage process about which they were questioned via phone or tablet.

Deggendorf says both person-to-person and on-line sources of information face challenges as mortgage influencers. Online sources have more work to do to gain trust and credibility before they can play a greater role influencing consumers, and person-to-person sources need to be vigilant regarding advances in online technology that might make that possible. "To be competitive, lenders and real estate agents need to continue to evolve their digital offerings to provide a multi- or omni-channel experience that allows consumers to move conveniently between online and personal interactions to create the experience that best suits their needs."

But he adds, that since previous research by Fannie Mae has shown that consumers' understanding of the mortgage qualification process is uniformly poor across different age groups, young consumers may continue to look to more traditional person-to-person sources for mortgage information and reassurance.