Deja vu all over again?

Freddie Mac says economic growth is recovering from a weak first half of the year, the labor market is holding steady and Fed watchers are concluding that a rate hike will come in December; worldwide economic growth is weak and appears likely to get worse. The company's economists add, "We've been here before... last year."

The economy continues to sputter along and the housing market continues to be a bright spot although with "less room to run than in the prior few years." Refinance-spurred mortgage activity is starting to slow as rates rise and that will persist into 2017 as the mortgage market becomes more purchase-dominated.

Freddie Mac's Outlook for October closely mirrors predictions in the Fannie Mae forecast earlier this month with a prediction of full-year GDP growth of 1.6 percent and a slightly better rate of 1.9 percent in 2017.

The volatility in financial markets has increased this month with a prediction of full-year GDP growth of 1.6 percent anafter a quiet summer. Post Brexit, the yields on 10-year Treasuries fell to a record low of 1.37 percent on July 5 then bounced back, remaining between 1.45 and 1.65 from mid-July through the beginning of September. Over the past month and a half yields have risen, reaching as high as 1.79 percent on October 12. As rates dropped so did the implied chances of a Fed rate like this year, to below 50 percent. Now it has risen to 67 percent.

Unlike Fannie Mae which has long said there will not be a hike this year, Freddie Mac still expects at least one but points out that doesn't mean mortgage rates will necessarily rise. That will depend more on global growth and worldwide bond yields. The latter are now off their post-Brexit lows, but most remain below pre-Brexit levels with Japanese and Swiss bonds still negative. The International Monetary Fund recently lowered their outlook for global growth.

Even if those bonds recover to their pre-Brexit levels Freddie Mac sees mortgages rates remaining low for an extended period. The 30-year mortgage was still below 3.5 percent when the Outlook went to press and their forecast calls for a gradual rise in rates throughout the remainder of 2016 and into 2017, with the 30-year fixed-rate mortgage averaging 3.9 percent in the fourth quarter of 2017.

Low rates alone, however, will not drive housing starts much higher. There will be an increase in starts, but a gradual one. Home builders still face land and labor constraints and while construction job openings have risen considerably, hiring has been flat. Housing construction's slow recovery, especially new single-family homes lead to a forecast of a 7 percent year-over-year increase in starts for 2016 and 14 percent in 2017 and even these total housing starts will not meet the long-run housing demand of that period.

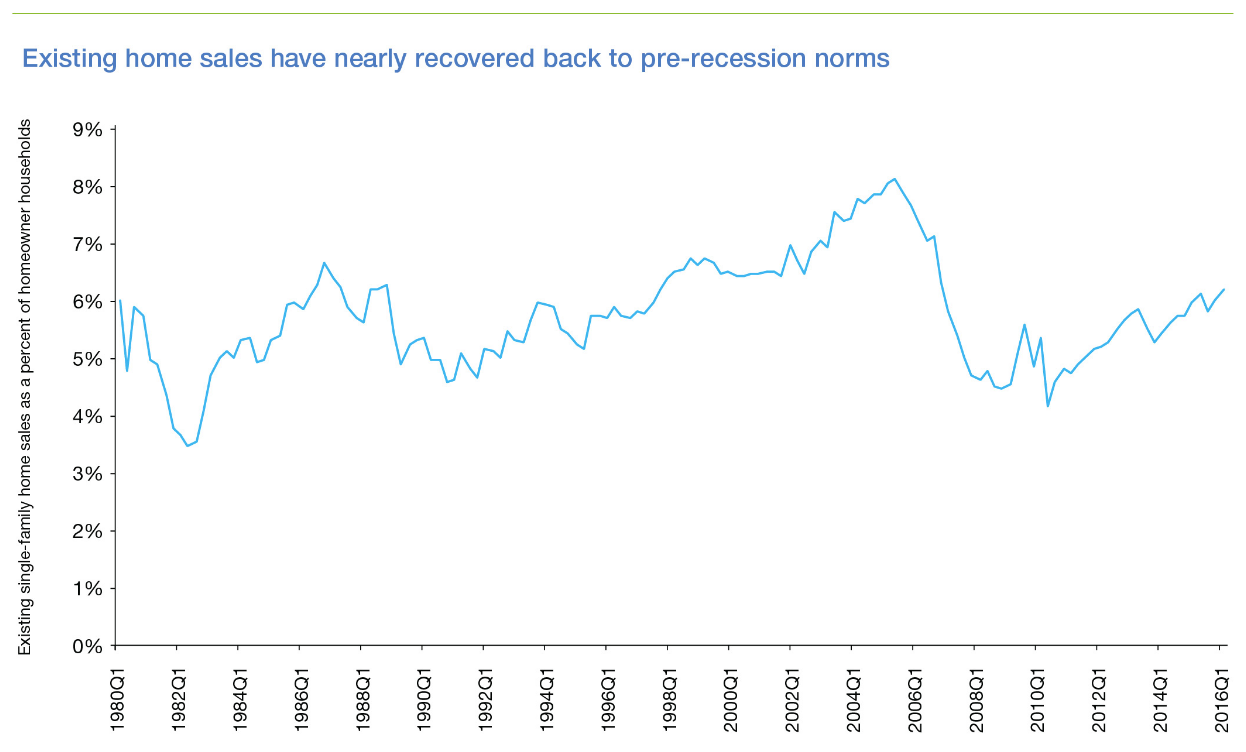

Despite the slow recovery in new home sales, total home sales will probably have their best year in a decade and existing home sales have nearly returned to pre-recession norms with the ratio of existing home sales to owner households back in the historical averaged range of about 6 percent. per year.

Freddie Mac's published an article earlier this month pointing to the decline in mobility and now say existing home sales might not have much room for improvement. The National Association of Realtors showed repeat homebuyers expect to live in their current home for 15 years (first-timers expect to remain in their home 10 year), up from 9 years (6 years) in 2006 and the Urban Institute says this declining mobility is affecting the mortgage market. This means that existing home sales are probably close to an equilibrium level.

They forecast a slight decline in seasonally adjusted total home sales in the fourth quarter. Increased construction of new homes will push total sales slightly higher in 2016, to 6.16 million in 2017 compared to 6.04 million in 2016.

Limited inventory and strong buyer demand continue to promote a robust level of price growth--about 6 percent on an annual basis through last June. Low mortgage rates are helping to offset the impact on affordability and the labor market is starting to show signs of wage growth. The considerable momentum in house prices will probably continue and the economists look for 5.6 percent growth in 2016, moderating to 4.7 percent in 2017.

The housing market should have begun its seasonal cooling, but mortgage application data show refinancing activity, while slowing from summertime highs, is still running about 30 percent higher on a year-over-year basis. Any upward movement in mortgage rates, however, will depress refinancing activity and Freddie Mac expects the volume of refinancing in 2017 will fall to just under $600 billion from this year's anticipated $1 trillion. Home purchase and home improvement mortgage activity will somewhat offset this, rising from $1 trillion in 2016 to $1.15 trillion in 2017. Total mortgage originations will fall about 18 percent from 2016 to 2017 according to the Economic and Housing Research Group's forecast.