The Mortgage Bankers Association (MBA) today released its Weekly Mortgage Applications Survey for the week ending October 8, 2010.

The MBA's loan application survey covers over 50% of all U.S. residential mortgage loan applications taken by retail mortgage bankers, commercial banks, and thrifts. The data gives economists a snapshot view of consumer demand for mortgage loans. In a low mortgage rate environment, a trend of increasing refinance applications implies consumers are seeking out a lower monthly payment. If consumers are able to increase disposable income through refinancing, it can be a positive for the economy as a whole (creates more consumer spending or allows debtors to pay down personal liabilities like credit cards). A falling trend of purchase applications indicates a decline in home buying demand, a negative for the housing industry and the economy as a whole.

Excerpts from the Release...

The Market Composite Index, a measure of mortgage loan application volume, increased 14.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 14.8 percent compared with the previous week. The four week moving average for the seasonally adjusted Market Index is up 3.0 percent.

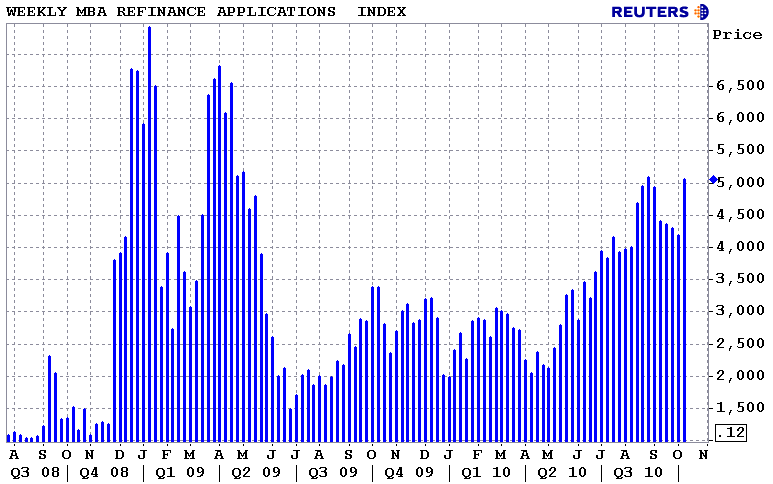

The Refinance Index increased 21.0 percent from the previous week. The four week moving average is up 3.9 percent for the Refinance Index. The refinance share of mortgage activity increased to 83.1 percent of total applications from 78.9 percent the previous week and is the highest refinance share since January 2009.

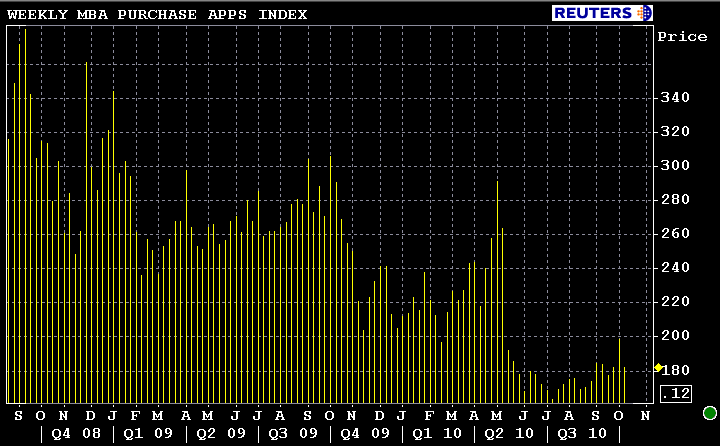

The seasonally adjusted Purchase Index decreased 8.5 percent from one week earlier. The unadjusted Purchase Index decreased 8.3 percent compared with the previous week and was 37.1 percent lower than the same week one year ago. The four week moving average is down 0.3 percent for the seasonally adjusted Purchase Index.

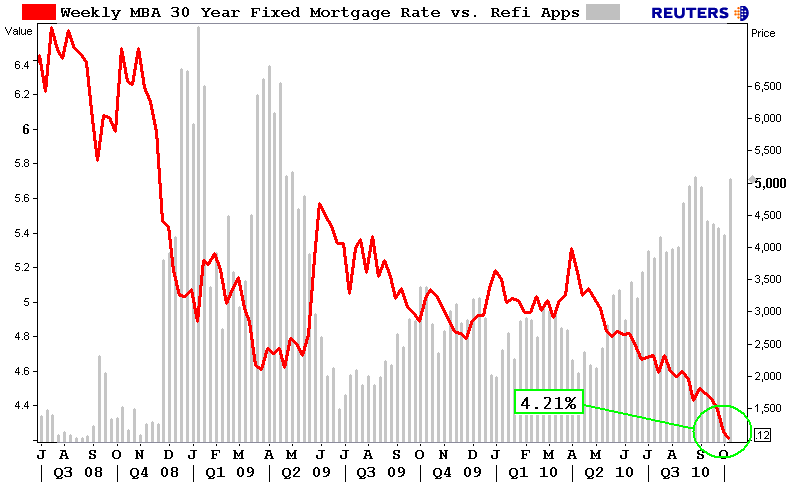

The average contract interest rate for 30-year fixed-rate mortgages decreased to 4.21 percent from 4.25 percent, with points increasing to 1.02 from 1.00 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans. The 30-year contract rate is the lowest recorded in the survey, while the previous low was observed last week. The effective rate also decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.62 percent from 3.73 percent, with points decreasing to 1.06 from 1.14 (including the origination fee) for 80 percent LTV loans. The 15-year contract rate is the lowest recorded in the survey, while the previous low was observed last week. The effective rate also decreased from last week.

The average contract interest rate for one-year ARMs decreased to 7.03 percent from 7.11 percent, with points increasing to 0.27 from 0.24 (including the origination fee) for 80 percent LTV loans. The adjustable-rate mortgage (ARM) share of activity decreased to 5.4

percent from 6.1 percent of total applications from the previous week.

Michael Fratantoni, MBA's Vice President of Research and Economics, sums up the survey results...

"After five weeks of steadily declining rates to yet another new low, borrowers who had been on the fence jumped off, which factored into refinance activity surging more than 20 percent. Refinance application volumes are now close to the highest level this year. Purchase activity remains generally weak, but applications for conventional purchase mortgages are now at their highest level since the beginning of May following the expiration of the tax credit. Last week saw a big jump in applications for FHA loans to purchase homes. We surmised that this was due to potential buyers wanting to beat the stricter FHA standards that went into effect October 4th. This conjecture was confirmed by the fact that this week FHA applications fell back to a level closer to the average seen over the past four months. "

READ MORE ABOUT FHA MIP UPDATES AND UP IN AIR SELLER CONCESSION REDUCTIONS

Last week was the first time mortgage rates were being offered on a consistent basis below 4.25%. I am wondering if the rise in refinance apps was a factor of new loan applications being submitted by fence sitting borrowers...or....was the uptick a fuction of increased fall-out followed by reapplications. Did you lose a few loans to a competitor last week?

Feedback appreciated.