While earlier generations tended to pay off their mortgages before they retired, the leading edge of Baby Boomers, now in their late 60s and early 70s have been less likely to do so. Fannie Mae says the increasing prevalence of housing debt among the 33 million-member strong generation has raised concerns it could compromise their retirement security. Carrying mortgage debt could expand housing affordability problems, crimp essential spending in other areas, limit the accumulation of housing wealth, and raise seniors' exposure to foreclosure.

Patrick Simmons, Director of Strategic Planning in Fannie Mae's Economic & Strategic Research Group writes in the current edition of the company's Housing Insights that, while several studies have documented the rise of mortgage debt among older homeowners, there hasn't been research into whether Boomers have sped up retirement of that debt as they themselves approach retirement age and the economy and housing market have emerged from recession.

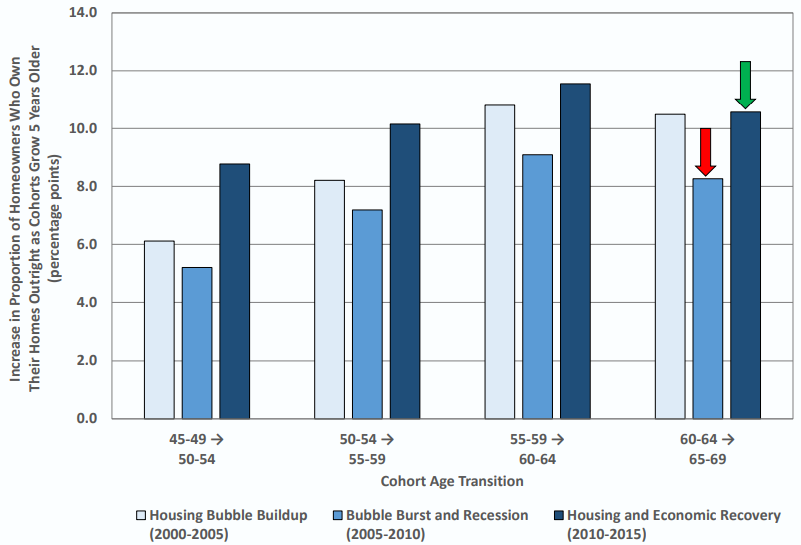

Simmons and the Research Group examined free-and-clear homeownership among Boomers across three periods; the "housing bubble buildup" (2000-2005), the "bubble burst and recession" (2005-2010), and the "recovery" (2010-2015) using age group analysis and cohort analysis. The first method compares data for fixed age groups as a generation moves through them, the second tracks changes as the same individuals grow older, passing from one age group to another.

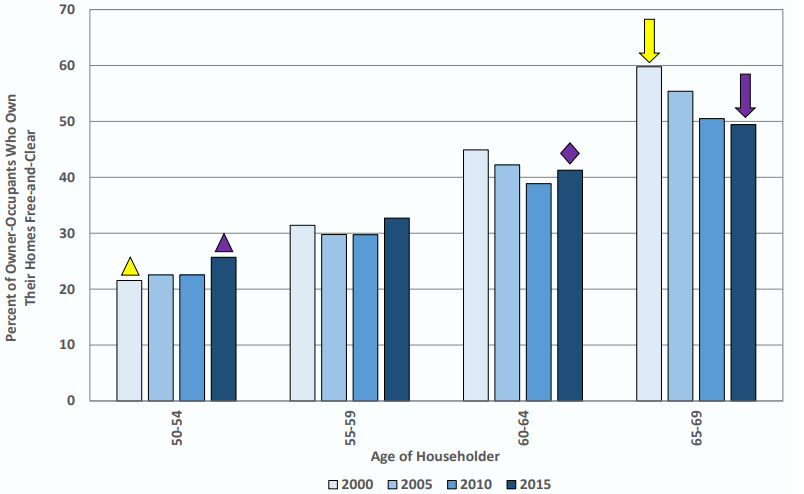

Using the age group approach, Simmons found Boomers who have passed the traditional retirement age are substantially less likely to own their homes outright than were other generations at that point. Among the generation's leading edge, owner occupants who were 65 to 69 in 2015, fewer than 50 percent were mortgage-free, 10 percentage points fewer than the preceding generation who were the same age in 2000, before the housing bubble started. Younger Boomers who were 50 to 54 in 2015 were significantly more likely to be mortgage free than those who preceded them. Twenty-six percent owned their homes outright compared to 22 percent who were the same age in 2000.

Tracking the Boomer cohort reveals that they have recently picked up the pace of paying down debt. Boomers of every internal age group became outright homeowners faster during the recovery period than during the recession. For example, for those who were 60 to 64 in 2010 and 65 to 69 in 2015, the show who owned their homes free and clear grew by 10.6 percentage points; more than a 2-point increase from those in the pre-Boomer cohort that passed through the same age range between 2005 and 2010.

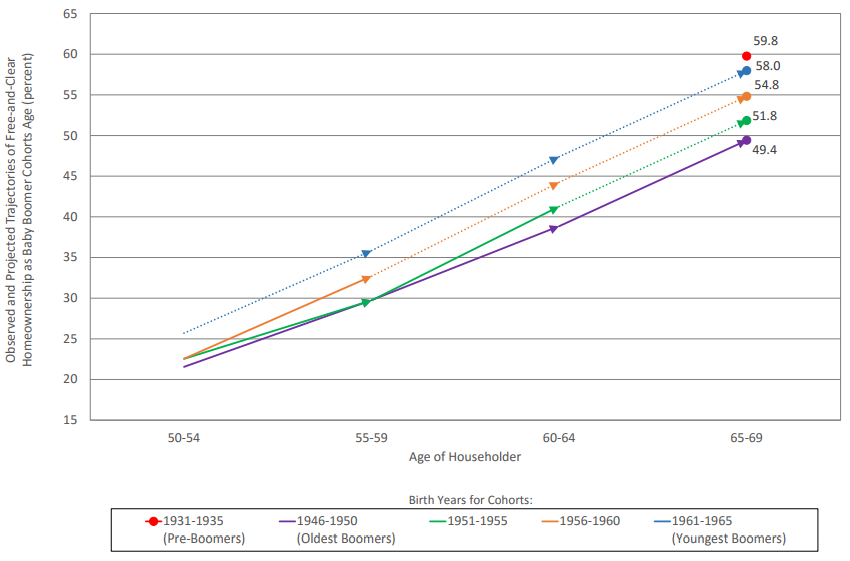

With only a few members of the huge Boomer generation presently at or above traditional retirement age, it remains to be seen how many of the remainder will get there without a mortgage. However, the authors say their cohort analysis provides some guidance. For each five-year age cohort of Boomers not yet at retirement, they project the share of those who may reach that age mortgage debt free by adding the 2010-2015 cohort increments depicted in Exhibit 2 to the observed 2015 baseline rates shown in Exhibit 1.

This leads to the estimate of 51.8 percent of Boomer homeowners in the cohort born between 1951 and 1955 will be mortgage-free when they reach 65 to 69 in 2020. Across the board, free and clear ownership of all five-year groups within the Boomer generation will lag those of the pre-Boomer cohort born between 1931 and 1935 as they reached 65 to 69 in 2000. The deficit ranges from a projected shortfall of 1.8 percentage points for the youngest Boomer group to an already observed deficit of 10.4 percentage points for the oldest.

The authors conclude that, even if Boomers continue the accelerated rate of debt reduction observed between 2010 and 2015, they will still reach lower rates of outright homeownership at retirement than their elders. To surpass them, Boomers will need to pick up the pace.

Simmons suggests some reasons for the accelerated pace of debt reduction during the recovery. Some Boomers may have adopted a more conservative attitude toward housing debt after the disruptions of the housing crisis, or may have confronted tighter credit markets or negative equity which made it difficult to borrow against their homes. As things improved, the rapid gains in equity may have enabled more Boomers to downsize to lower value homes without using mortgage financing. Improved employment and wages may have allowed homeowners to pay off their mortgages and/or reduced the need to cash out equity to meet expenses. Finally, elevated levels of foreclosure well into the recovery may have forced some boomers to exit homeownership and helped nudge the share of outright ownership higher.

The relatively high incidence of housing debt among Boomer homeowners, even with the increased rate of paydown, has the potential to strain their retirement finances. Given that income typically declines in retirement, monthly mortgage payments could stretch the household budgets of Boomers who exit the labor force without first extinguishing their housing debts. Indeed, among Boomer homeowners aged 65 to 69 in 2015, those with mortgages were over three times more likely to experience a housing cost burden than were those who owned their homes outright.

The larger share of older mortgagors and the generation's apparent openness to mortgage debt should lead to more business for both originators and servicers than in previous generations. However, whether this is a profitable situation depends in part on the ability of Boomers to successfully manage their monthly housing costs as their financial situation changes in retirement. The authors suggest this may signal the need to expand consumer outreach and education, including ensuring that older mortgagors have "fully exploited opportunities to reduce monthly mortgage payments through refinancing." They also suggest educating younger Boomers about benefits from shorter-duration mortgages and older Boomers about the advantage of trading down to less expensive homes.