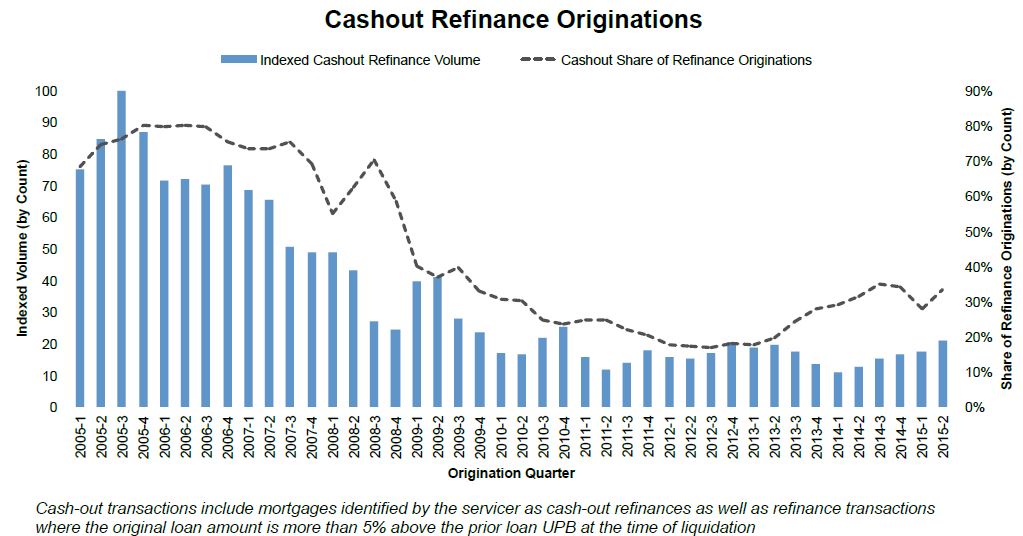

While they aren't doing it at nearly the rate they did before the Great Recession, Americans are increasingly tapping the equity in their homes with cash-out refinancing. Black Knight Financial Services says in its latest Mortgage Monitor Report released on Monday that cash-out refinances in the second quarter were at the highest rate in five years.

Lack of equity prevented many homeowners from refinancing at all for a number of years and they could not take advantage of the historically low interest rates. Now rising home prices have restored many to positive equity positions and even to having "tappable" equity based on an 80 percent combined loan-to-value (CLTV) ratio. Black Knight says total home equity is at its highest level since 2007, up nearly $1 trillion since last year, about $19,000 more per borrower. Fifty-nine percent of that equity or about $4.5 trillion, is tappable.

In the current Monitor Black Knight analyzes refinance transactions to compare the resulting mortgages to the prior loans they replaced. The company's Senior Vice President of its Data and Analytics Division Ben Graboske says that borrowers have been capitalizing on increased equity available in their homes and still historically low rates.

"In the second quarter of 2015, we saw cash-out refinance volumes rise almost 70 percent from the same period last year," said Graboske. "While this is the highest volume in cash-out refinances we've seen in five years, it's still nearly 80 percent below the peak in Q3 2005. Even so, it's clear that borrowers have been capitalizing on the increased equity available to them."

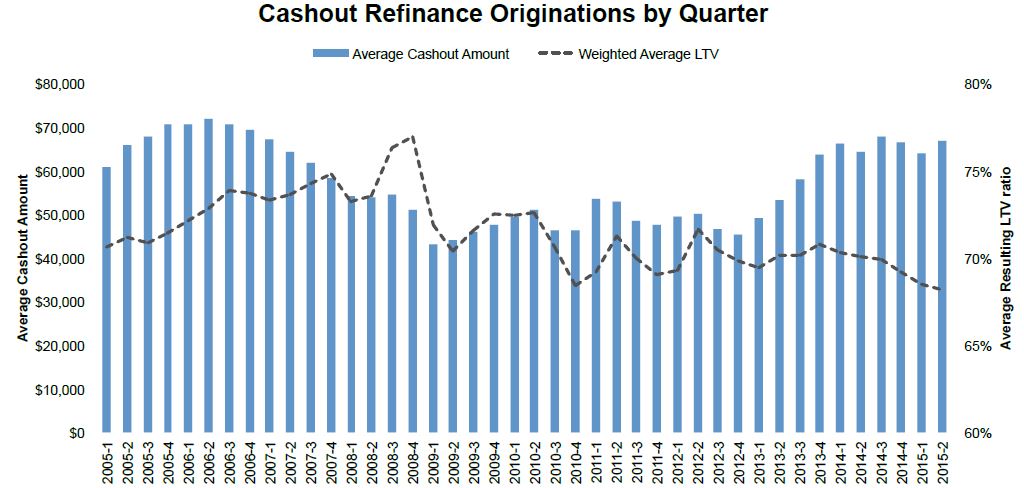

Graboske says borrowers today are pulling out an average of $67,000 of equity through cash-out refis, nearly the levels seen in 2006 but even after pulling out that equity, resulting average LTVs are at 68 percent, the lowest level in over 10 years. "During this same time span," he said, "we've seen second lien HELOC lending rise, albeit at a lesser rate; that volume is up 40 percent from last year. However, as interest rates rise, we could see an increase in HELOC lending and corresponding slowing in first lien cash-out refis, as borrowers will likely want to hang on to lower rates for their first mortgage while still being able to tap available equity."

The analysis found that less than 10 percent of cash-out refinances result in LTV's above 80 percent, the lowest level in 10 years. Nearly 60 percent of cash-outs by volume are of loans with UPBs under $200,000.

As it analyzed the new loans in comparison to those they replace the company found that the distribution of cash-out refinances is highly concentrated geographically, with over 30 percent of all such transactions occurring in California alone. Texas is second among states in terms of cash-out refinance volume, at just 7 percent of the nation's total.

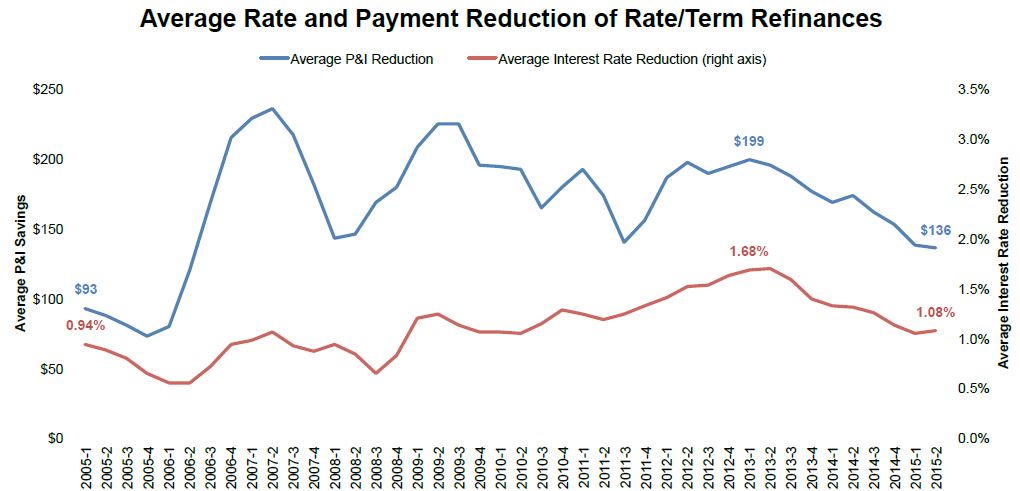

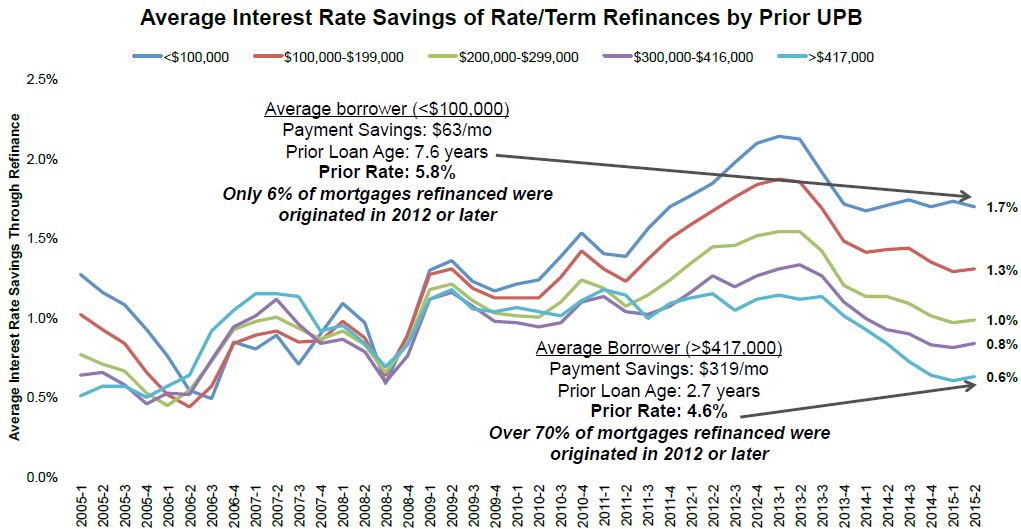

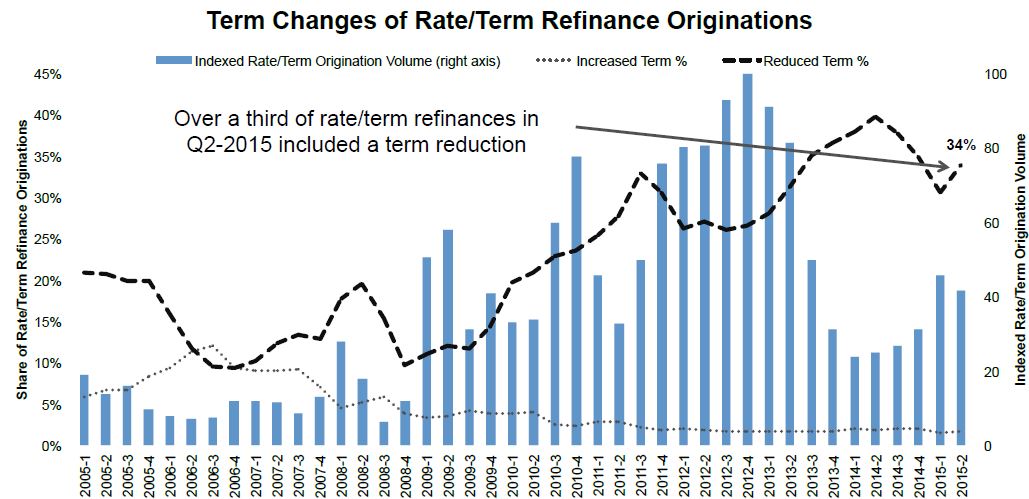

The 2015 refinances are saving the average borrower $136 per month in principal and interest payments and cutting their rate by just over 1 percent. These are the smallest savings in nine years and the lowest rate reductions in five. Black Knight attributes this to the fact that borrowers refinancing either have lower unpaid balances (UPB) and thus smaller savings, or that higher UPB borrowers are taking advantage of low rates for a second or third time, and so are seeing incremental savings compared to earlier reductions. Black Knight also observed increased interest among borrowers in securing term reductions through refinancing; 34 percent of rate/term refinances in Q2 2015 included a term length reduction.

Those borrowers with UPB's of less than $100,000 had carried their previous mortgages for longer periods - generally 7 to 8 years - compared to those with UPBs over $417,000. Only 6 percent of the low balance loans were originated in 2012 or later compared to 70 percent of those with high balances.

Dollar savings on the large UPB loans averaged $319 in the second quarter compared to over $670 per month in the third quarter of 2013 while savings on loans with an unpaid balance of less than $100 dropped from the peak of $91 in the fourth quarter of 2012 to $63.

Over a third (34 percent) of refinances in the second quarter of 2015 featured a reduction in the term of the loan. Term reductions ran as high as 40 percent of refinancing back in mid-2014 and Black Knight says that this is in line with historic data showing that, as the volume of rate/term refinancing increases it is usually driven by interest rate reductions and the share of term reductions falls. However, during the refinancing boom from late 2011 to 2013 the rate of terms reductions was 25 percent. (The Home Affordable Refinance Program (HARP) was reconfigured in late 2012 and carried a feature encouraging the reduction of loan length which might account for some of the subsequent increase.)

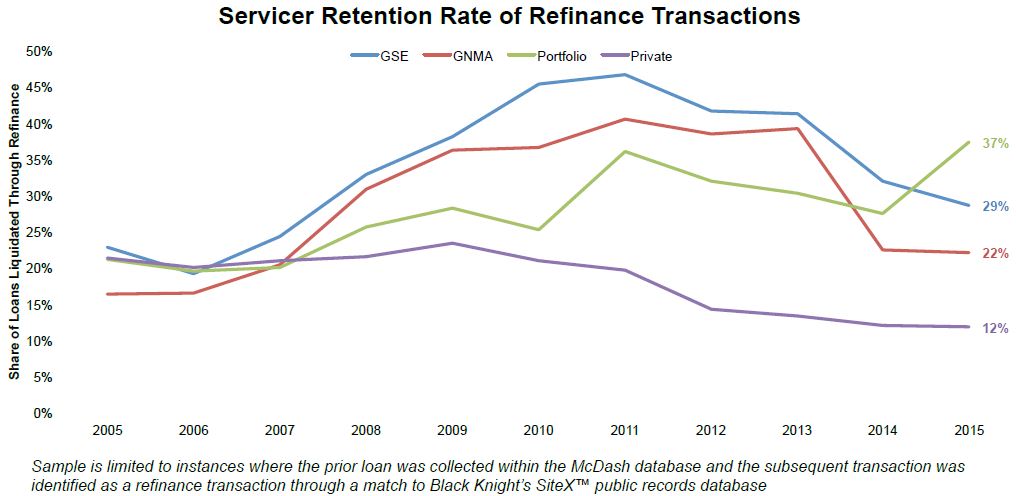

Servicers are not doing a particularly good job retaining loans through the refinancing process; the rate of retentions has dropped from 44 percent at the 2011 peak to about 26 percent in the second quarter of 2015. Servicers of GSE loans and portfolio loans have higher retention rates - 29 percent and 37 percent respectively. Black Knight speculates that the GSE figures are presumably aided by HARP refinance originations while portfolio retentions may be attributable to the emphasis many servicers place on retaining jumbo and high credit borrowers. The data also show that retention rates trend lower on cash-out refis than on those for rate and term.

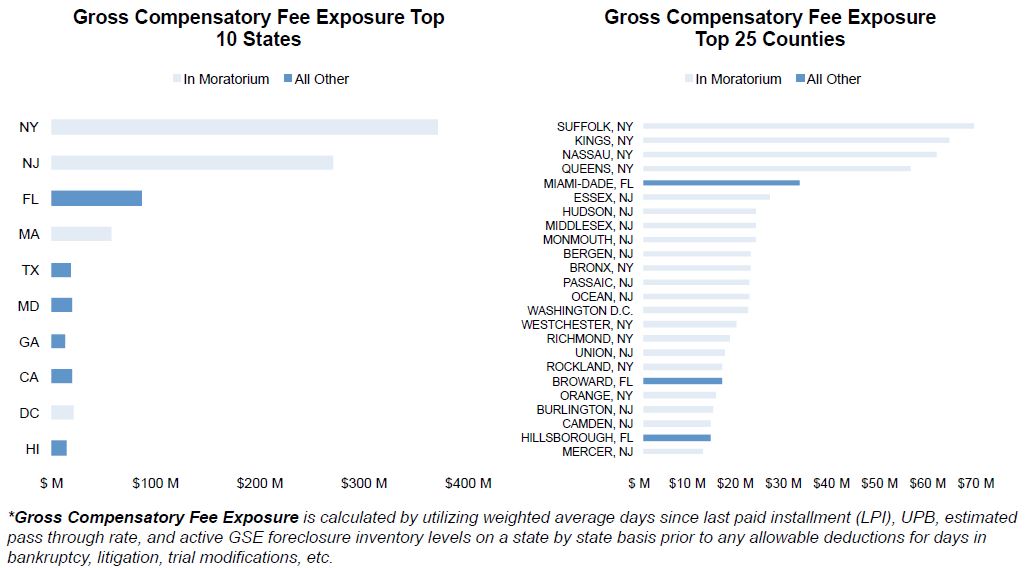

In mid-September the GSEs announced they were increasing their maximum number of allowable days for a foreclosure sale in 33 states and Puerto Rico. Extensions in 12 of the states were as small as 30 days while in Oregon the extension was for 480 days. Black Knight says these extensions play a significant role in servicers' overall compensatory fee exposure depending on what happens when they expire at the end of 2015. The GSEs also extended compensatory fee moratoria in New York, New Jersey, Massachusetts, and Washington, D.C. from June to December 31, 2015.

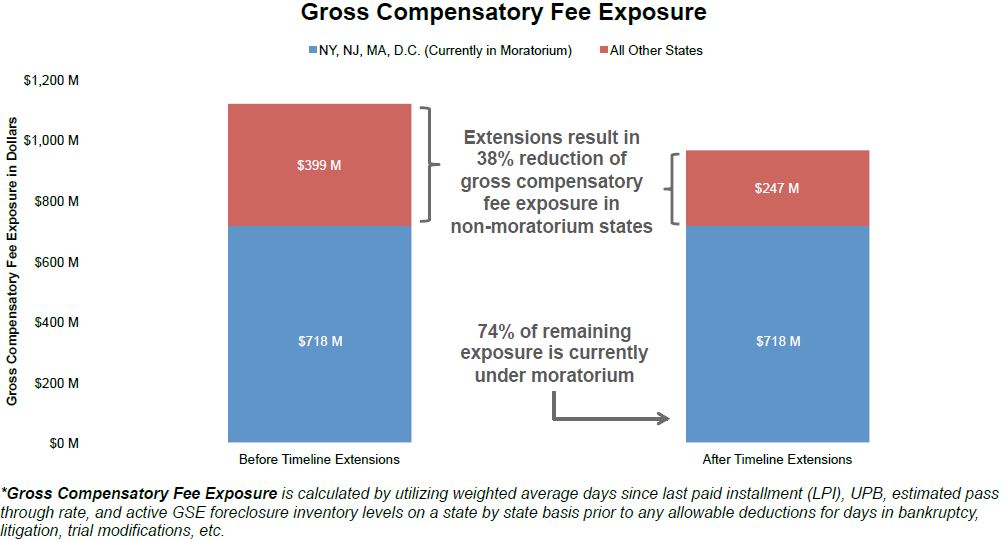

Black Knight says New York and New Jersey alone carry two-thirds of the country's compensatory fee exposure, even though these states only account for 27 percent of active GSE foreclosure inventory. All totaled, the states covered by the existing moratorium account for 74 percent of remaining compensatory fee exposure, and the foreclosure timeline extensions result in roughly a 38 percent reduction of gross compensatory fee exposure in non-moratorium states. Lifting the moratorium - with timelines remaining as they stand now - would result in nearly a quadrupling of mortgage servicers' compensatory fee exposure.

The company looked at estimated compensatory fee exposure for all active GSE foreclosures if they liquidated today (prior to any allowable deductions for days in bankruptcy, litigation, loan modifications, etc.) The GSE timeline extensions result in a 38 percent reduction of gross compensatory fee exposure in non-moratorium states while74 percent of the remaining exposure is currently under moratorium. Currently 25 percent of seriously delinquent (90 days or more) loans are already in excess of their state's allowable timelines. Lifting the moratorium with timelines remaining where they currently are would result in nearly a quadrupling of servicers' compensatory fee exposure.