The Mortgage Bankers Association (MBA) released its report on the commercial/multi-family finance picture for the second quarter on Tuesday, saying that the markets had gained a "not-inconsiderable momentum." What the data does not show, the report says, is any of the impacts that will result from "an August to forget" which saw a debilitating debate over the debt limits, a downgrade of the country's credit worthiness, and the focus on an uncertain European economy. "For all these reasons," the MBA says, "the information presented here is best viewed as prologue."

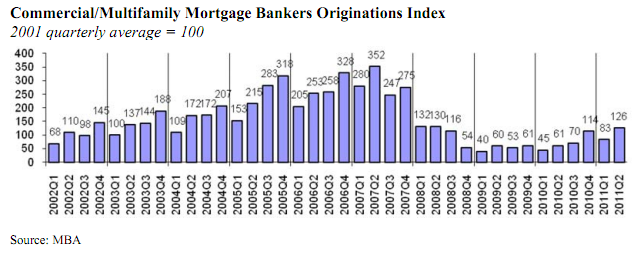

The Commercial/Multifamily MBA Originations Index rose from 83 in the first quarter of 2011 to 126, more than double the index of 61 one year earlier. The index, which reached an all time low of 40 during the first quarter of 2009, reflects the quarterly average in 2001 of 100. CRE/Multifamily Originations for Fannie Mae and Freddie Mac rose 58 percent, 87 percent for life insurance companies (to the highest level ever), and 150 percent for commercial banks. Originations for CMBS conduits rose 638 percent for the market's highest quarterly issuance volume since 2007 of $12.4 billion.

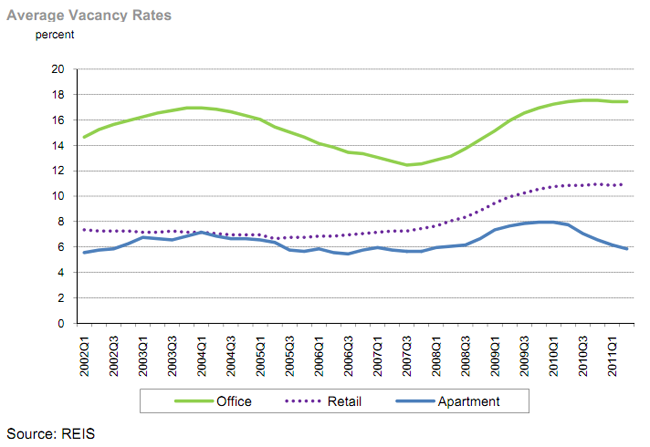

The increased demand for rental housing was reflected in apartment fundamentals; vacancy rates fell to 5.9 percent in the second quarter and average asking rents rose two percent from the second quarter of 2010 to an average of $1,053 a month. These increases were not seen in office or retail vacancies; the former held steady at 17.5 percent and the later rose 0.1 percent to 11.0 percent and rents were essentially unchanged.

During the second quarter construction was begun on 163,000 housing units, 123,000 of which were single family units. These figures are an increase from the 126,000 units started in Quarter 1, 90,000 of which were single family. Of the 40,000 units in buildings with two or more housing units, 93 percent were being constructed for rent.

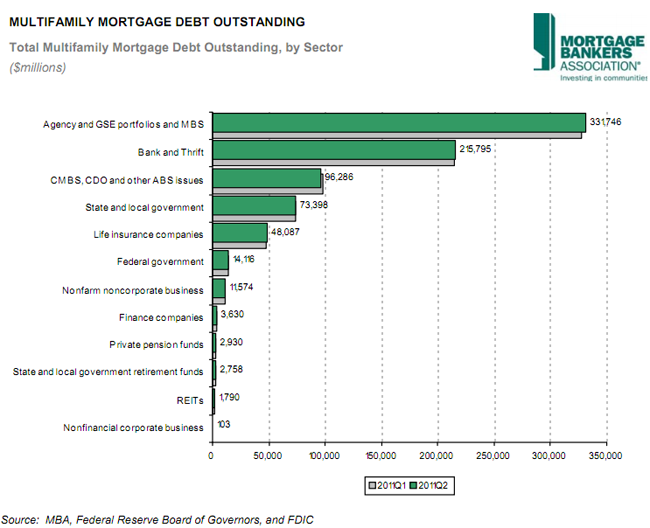

Outstanding multifamily mortgage debt is at $802 billion, up 0.5 percent from the first quarter. The largest increase by sector is in Agency and GSE portfolios and MBS, now at 331.75 billion, or 41 percent of the total multifamily debt, an increase of 1.3 percent from Q1. Banks and Thrifts increased their holdings by 0.6 percent to a 26.9 percent share and CMBS, CDO, and other ABS issues fell 1.6 percent to a 12.3 percent share of multifamily debt. Private pension funds and finance companies, already small players, fell even further, losing 5.3 percent and 4.6 percent respectively of their holdings.