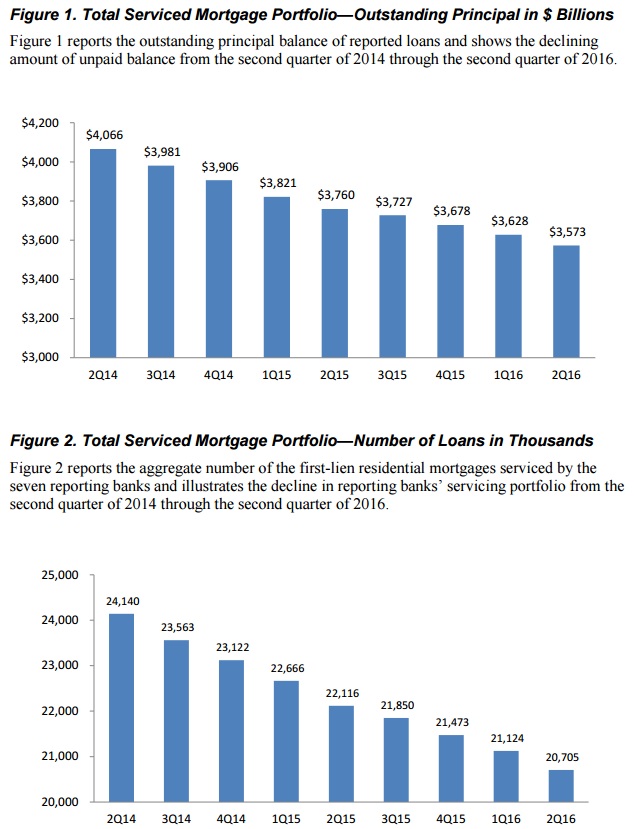

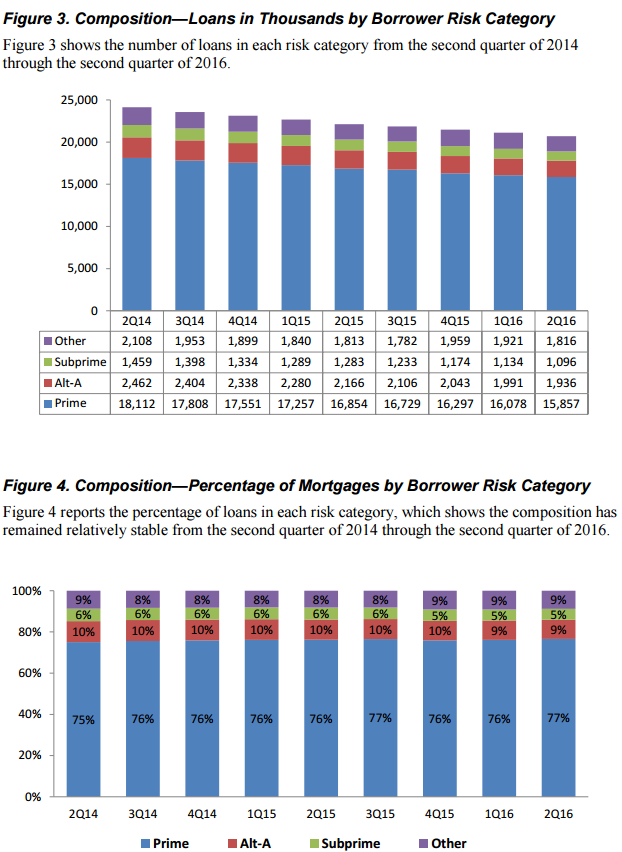

The second quarter Mortgage Metric Report from the Office of Comptroller of the Currency (OCC) shows a universe of mortgage loans that are performing in a relatively stable manner, with any movement toward further improvement. The report covers seven national banks with large servicing portfolios. In total those institutions were servicing approximately 20.7 million first lien mortgages with $3.6 trillion in unpaid principal balances (UPB). The dollar figure represents 37 percent of all first-lien mortgage debt in the US. At quarter's end, about 89 percent of these loans were being serviced by the national banks for third parties.

One trend which OCC did not mention but which stands out strongly in the graphics is the decline in mortgages, in both number and UPB, that are being serviced by the seven banks.

The share of those mortgages that were current and performing in the second quarter of 2016 was a slight improvement from a year earlier, 94.7 percent compared with 93.8 percent. This no doubt reflects the composition of the portfolio. Close to 16 million of the loans or 77 percent are rated as prime with Alt-A and subprime loans each comprising shares in the single digits. The percentage by risk has remained remarkably stable over the last two years even as the total number of mortgages has declined from over 24 million since the second quarter of 2014

Servicers initiated 48,732 new foreclosures during the second quarter, down 17.3 percent from the first quarter of the year and 31.1 percent from a year earlier. Home forfeiture which includes completed foreclosures, deeds-in-lieu of foreclosure, and short sales numbered 33,344 a decline of 29.0 percent from the second quarter of 2015.

Servicers are still involved in loan modifications and completed 34,604 during the quarter. Nearly all were what OCC called "combination modifications," those that included multiple components to improve the affordability and sustainability of the loan. Only 1,855 loans were modified using a single action.

The action with the highest prevalence was capitalization of delinquent interest and fees which was applied to 93.9 percent of the workouts while 87.6 percent received an extension of the term and 81.8 percent got an interest rate reduction or freeze. Only 7.5 percent saw a reduction in principle and 11.9 percent a deferral. The loan modification reduced the monthly payment in 87.2 percent of the cases.

Among loans that had aged six months post-modification (these would be workouts completed in the fourth quarter of 2015) 4,404 were 60 or more days past due by the six month anniversary of the modification. We could not locate, anywhere in the report, information on the total number of modifications completed in that quarter.