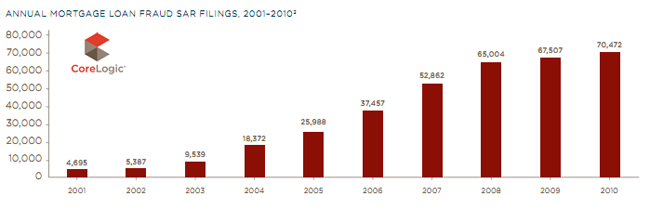

While overall rates of mortgage related fraud appear to have fallen significantly in 2011, some particular manifestations have increased dramatically according to a new report authored by CoreLogic. The company predicts that fraud related U.S. residential mortgage originations will total $7.4 billion this year, a near 40 percent decline from the estimated $12 billion experienced in 2010.

The dollar figure placed on fraud is down partially because of the decline in mortgage volume, but lenders are also better managing the situation. CoreLogic said its Fraud Index which represents the collective level of fraud risk the industry was experiencing each quarter, has remained relatively flat for the last five quarters and has declined more than 28 percent since its peak in the third quarter of 2007. This indicates, Core Logic said, that lenders' improved fraud controls have reined in fraud growth. Fraud losses in 2011 are expected to be 75 percent below those when the CoreLogic began the study in 2005.

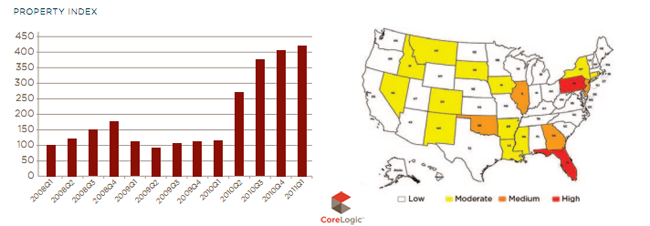

The types of fraud reported have changed significantly over the last year. Property fraud, which increased only 4 percent between the first quarters of 2009 and 2010, skyrocketed 262 percent over the next four quarters. Fraud related to undisclosed debt grew at a slower rate (19 percent) between 2010 and 2011 than in the 2009-2010 period (68 percent). Fraud involving occupancy increased 11 percent. Identity theft dropped by 45 percent during the recent period, fraud related to employment was down 11 percent and fraud related to income was unchanged.

Property fraud includes flips and flops, and distressed sales remain the source of significant risk. CoreLogic estimates that unrealized recoveries on short sale transactions may be costing lenders as much as $375 million a year. Unscrupulous investors, real estate agents, and other actors are preying on delinquent borrowers and arranging same day flips through the short-sale process.

The report notes that FHA loans present significantly higher risk of fraud than the non-FHA counterparts. The less stringent requirements for loan-to-value and down payments leave borrowers with less "skin in the game" and lenders at risk for larger losses.

In compiling its report, CoreLogic, a provider of information, analytics and business services analyzed 10.5 million loan applications from the first quarter of 2005 through the first quarter of 2011.

"Although our data shows the overall fraud rate has been relatively flat over the last few quarters, new fraud schemes are constantly evolving to infiltrate weaknesses and vulnerabilities in lenders' fraud prevention programs," stated Tim Grace, senior vice president of Product Management and Analytics at CoreLogic. "For example, the study shows that the primary reason for the increase in property fraud risk is related to potential fraudulent flipping and flopping of properties.

The five riskiest areas of the country for fraud-related originations are Chicago, Washington, DC; Brooklyn, NY; Atlanta, GA, and Jamaica, NY. Each has a fraud rate that is at least 30 percent higher than the national average.

CoreLogic advises originators to establish and optimize fraud prevention procedures by combining multiple alerts with predictive fraud scoring.