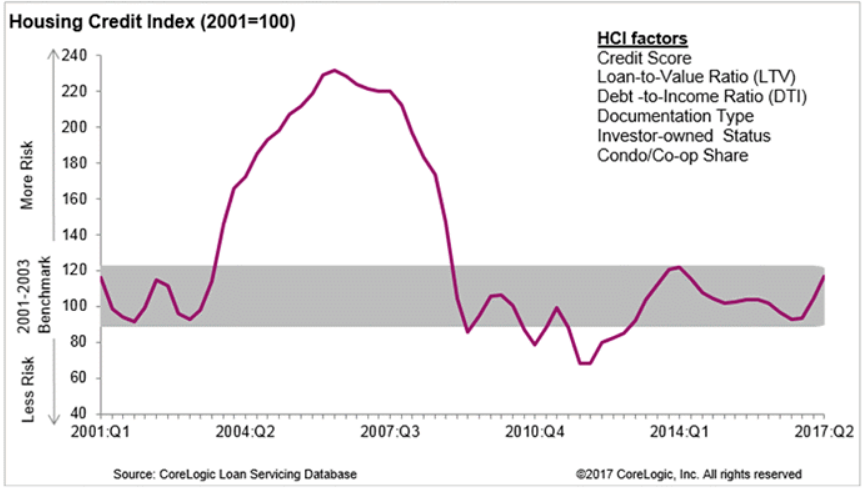

While it is still within what is considered normal limits, credit risk did move higher among loans originated during the second quarter of the year. CoreLogic says its Housing Credit Index (HCI) increased by 20 points when compared to the second quarter of 2016, to 117.

The HCI measures the relative increase or decrease in credit risk for new mortgage loan originations when compared to earlier periods across six risk categories. The six are borrower credit score, debt-to-income ratio (DTI), loan-to-value ratio (LTV), investor-owned status, condo/co-op share and documentation level.

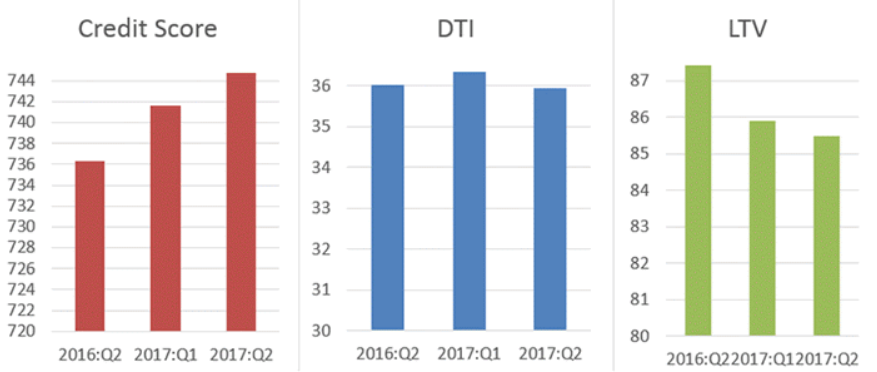

CoreLogic says risks in the three borrower credit categories, credit score, DTI, and LTV, improved during the quarter. Credit scores moved higher by 9 points to an average of 745, LTV's were down from 87.4 percent to an average of 85.5 percent, while the average DTI was unchanged. Those improvements, however, were offset by shifts in the other three attributes.

The investor share of home purchase loans increased year-over-year from 3.6 percent to 4.2 percent and the share of home purchase loans secured by a condo or co-op moved from 9.6 percent to 11.1 percent. Low-or no-documentation loans remained only a tiny part of the market, but did bump up 0.2 percentage point to a 1.7 percent share.

Risk factors in the second quarter 2017 HCI are within range of those for 2001 to 2003, a period which CoreLogic says is a normal baseline for credit risk. For example, the share of homebuyers with scores under 640 was 2 percent in the second quarter of 2017 compared to a share of 25 percent in 2001. On the other hand, the share of homebuyers with DTIs equal to or greater than 43 percent has risen slightly, from 18 percent in 2001 to 22 percent and there was a big jump, almost 50 percent, in the share of loans with LTV's of 95 percent or more.

"Mortgage risk for new originations increased modestly in the second quarter of 2017, but much of this rise was due to a small shift in the mix of loan types to more investor and condominium loans, which have slightly higher risk attributes," said Dr. Frank Nothaft, chief economist for CoreLogic. "Despite the somewhat higher risk of new origination loans, purchase mortgage underwriting remains relatively clean with an average credit score of 745 and low delinquency risk."