Why are so many people holding on to mortgages with high interest rates? Sentiment? Inertia?

Apparently not. In the current issue of CoreLogic's MarketPulse, Principal Economist Molly Boesel drills down into the universe of borrowers who are standing fast with their old loans, even though it looks on paper like a refinance would be a smart move. She finds that many of these borrowers haven't refinanced either because they can't or it really isn't worth it.

Looking at the mortgages that were outstanding at the end of May, Boesel found that 41 percent of them representing 31 percent of unpaid principal balance (UPB) had mortgage rates greater than 4.38 percent, roughly 100 basis points higher than the current rates at that juncture and a point at which refinancing makes financial sense. Eighteen percent of all mortgages (representing 17 percent of UPB) have rates between 4.38 and 5.0 percent, and 23 percent have rates over 5 percent. Why wouldn't these borrowers refinance?

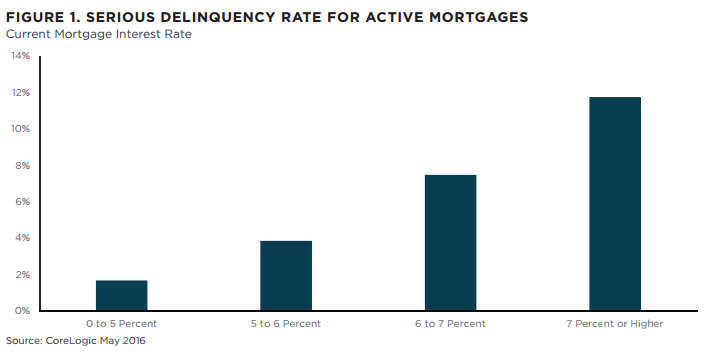

First she found that a lot of them are currently seriously delinquent on their existing loans. While only about 2 percent of low interest rate mortgages (under 5 percent) are seriously delinquent, 12 percent of those with rates above 7 percent are 90 or more days past due and would be unlikely to qualify for a new mortgage.

Even current mortgages with high rates present a difficult credit profile. Between 30 and 50 percent of loans with rates over 5 percent have at some point had a 30-day delinquency. The incidence rises with the rate. Only about 11 percent of those with rates below 5 percent have at some point been 30 days overdue. Those "ever late" borrowers may not be able to qualify for a low enough rate to make refinancing attractive.

Boesel also removed mortgages in private-label securities from the list of refinancable borrowers because they would not be eligible for HARP loans that are reserved for refinancing Fannie Mae and Freddie Mac loans.

After taking the currently delinquent, ever delinquent, and private label loans out of the mix she found that the share of loans with interest rates greater than 5 percent had fallen to 13 percent of those outstanding and to 7 percent of UPB. And that latter number is the final piece of the puzzle.

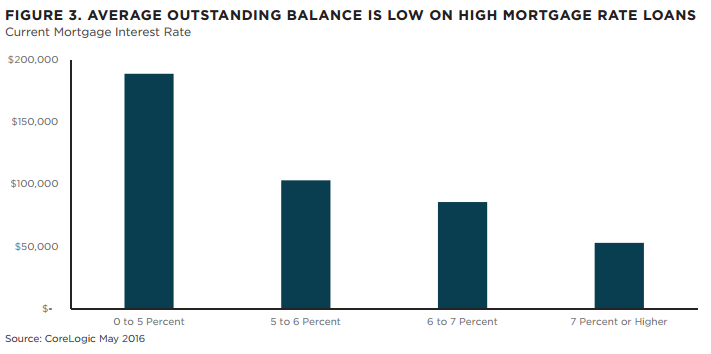

Small outstanding balances may not be worth refinancing as the resulting savings would be low. The figure above shows the average UPB of outstanding mortgages that have never been delinquent and are not in private pools by their interest rate. Those borrowers with rates above 5% have very low UPB; those above 7 percent have average balances of $53,000.

While mortgages rates are near historic loans, Boesel concludes, there may not be many borrowers left who have the incentive or are eligible to refinance.