The Federal Housing Finance Agency (FHFA) is requesting public comment on two alternative mortgage servicing compensation structures. The proposed structures are the result of work done under a Joint Initiative involving Freddie Mac and Fannie Mae (the GSEs), FHFA, HUD, FHA, and Ginnie Mae.

FHFA's stated intention in issuing a directive to the GSEs last January to participate in such planning was to improve service for borrowers, reduce servicers' risk, and provide flexibility for guarantors to better manage non-performing loans (NPLs) while promoting continued liquidity in the To Be Announced (TBA) mortgage securities market. The Joint Initiative also seeks to develop options for compensating servicers that will enhance competition and can be replicated in any future housing finance structures that emerge under GSE reform.

Servicer compensation (Mortgage Servicing Right or MSR) is currently decided by the originator setting the mortgage rate offered to borrowers in terms of the spread above the par TBA price net of the guarantee fee that, when combined with the other income derived from origination and servicing (late fees, interest on escrow and payment floats) provides the servicer with an acceptable risk adjusted return on capital. The spread charged in the mortgage rate for origination and servicing is based on competition, expected costs, and the expected returns of originator and servicer and should cover the expected costs of servicing including servicing NPLs. When a loan is sold into the secondary market for Enterprise, FHA, or VA loans, the servicer is generally required to retain a Minimum Servicing Fee (MFS) of 25 basis points for the GSEs and 44 basis points for Ginnie Mae.

The servicer collects its servicing fee from the interest portion of the mortgage payment before passing it on to the investor. When a loan fails to perform there is no payment and the servicer receives no servicing fee cash flow but is still expected to perform to the terms of its contract obligations.

FHFA said that, in order to understand the proposed context for determining alternative compensation structures, it is important to frame the following fundamental aspects of the current compensation framework:

- The servicers' right to receive MSR cash flow is dependent upon its continued performance under the contract guidelines and these rights are typically reflected as an asset on the servicer's balance sheet.

- The minimum 25 basis points that servicers are required to retain serves as collateral for the GSEs and sets a minimum level of ongoing cash flow compensation under Servicing Guidelines. As a result, changing the MSF does not create or eliminate revenue to the servicer; instead it changes the timing of when the revenue is received in cash, and the corresponding tax treatment.

- The originator prices into the note rate expectations about future default rates and related servicing costs. Any changes that raise expenses result in the servicer realizing lower returns than expected.

- The MSR is a capitalized asset by definition and, even in the current credit cycle with its higher costs, the compensation framework still results in the MSR being an asset for most servicers.

- The current financial crisis has revealed a number of issues in the current servicing model such as a failure of the servicers to invest some of their historically large spreads in technology, systems, and infrastructure because it would have increased their costs and might have led to a write down of the MSR asset. Thus they were unprepared for the significant increase in delinquencies and default. This led to some practices that did not comport with professional standards or even applicable laws.

A form of the first proposed change in the compensation structure was proposed both by the Mortgage Bankers Association and the Clearing House Association and involves a modest change to the current Enterprise Servicing Compensation Model. Because of the similarity of the proposals, FHFA is presenting for public comment this concept.

- Servicers would retain a reduced MSF strip of 12.5 to 20 basis points with an additional reserve account (ranging from three to five basis points) to cover non-performing loan servicing costs.

- The reserve account would "kick-in" after pre-determined thresholds are met. If reserves are not needed, servicers could reclaim all or part based on triggers such as geography-based market conditions, time periods, or performance measures. Each servicer would have its own reserve account related to its loans; there would be no cross-collateralization among servicers' reserve accounts.

- The reserve account would move with any transfer of servicing from old to new servicer.

- The reserve account would be subject to the rights of the GSE in the event of servicing seizures.

- Selling representations and warranties would be held by the servicer, as they are today, and would transfer with the servicing to the new servicer. Bifurcation would continue to be evaluated and negotiated on a case by case basis.

- The servicer bears the risk that the MSF and the reserve account are insufficient to cover the servicer's costs. The guarantor/investor/trustee may directly compensate servicers to cover any resulting shortfall, consistent with current practice.

- The structure will allow for a MSF that would provide a means to accommodate regulatory changes to servicing requirements.

- The structure does not substantially change the nature of the treatment or execution of excess IO from today's model.

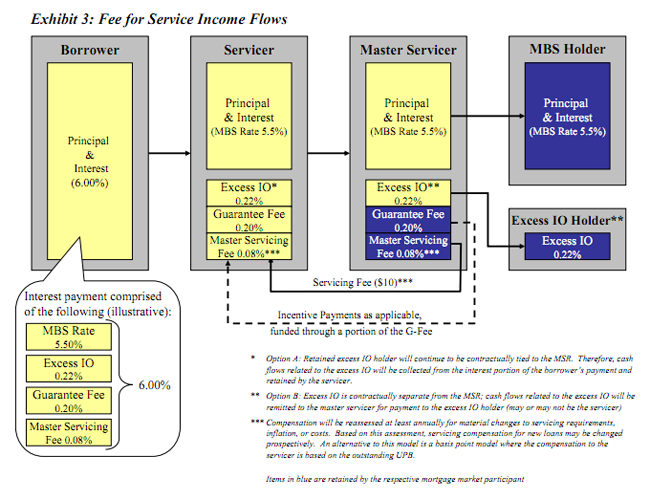

The second proposed compensation structure is a Fee for Service Model which could serve as a concept model for loans backing MBS guaranteed by the Enterprises, government-insured, and private label securities by better tying compensation paid to the servicer with the actual services performed by the servicer.

The Fee for Service model includes the following features:

- The guarantor will pay a set dollar fee per loan for servicing performing loans. This will tie the compensation to the number of loans being serviced, the predominant driver of servicing costs, rather than the size of the mortgage. This will be funded though a master servicing strip from the interest payments made by the borrower. For purposes of discussion, this fee is expected to be $10 per performing loan. An alternative is a basis point model tied to the outstanding unpaid principal balance.

- The servicer has increased flexibility in the level (if any) of excess IO strip that is retained vs. monetized up-front.

- The servicer retains ancillary fee income and interest on escrow and investor fund floats.

- The guarantor will continue to cover the credit risk for NPL and may pay incentives to the servicer to better mitigate the guarantor's loss exposure.

- The structure would allow for regulatory changes to servicing requirements to be assessed at least annually.

- Selling and servicing representations and warranties will be bifurcated.

- Two potential options for managing excess IO cash flows (above the MSF) have been discussed. They vary in how they minimize the risk of MSR capitalization, provide flexibility and liquidity to the originator/seller, and impact the management of representation and warranty risk.

Option A retains the status quo with excess IO interest contractually tied to the MSR so the seller can chose to retain the excess or sell it to the GSE though a buy-up at the time of securitization.

Option B would separate the excess IO contractually from the MSR so the seller can choose to either sell it to the GSE or receive an excess IO interest which has been separated from the servicing compensation and contract.

The Fee for Service proposal could also be applied to the private label securities (PLS) market which, members of the investment community have said must be changed to attract private capital back to the securitization business. This market currently suffers from a lack of transparency with regard to the terms of servicing contracts because they are treated as proprietary and confidential documents. The new proposal would not provide a solution for the full range of reforms needed but it would provide greater transparency around how servicing would be conducted, where the responsibilities are housed, and what remediation options are available. That compensation paid to the servicer is tied to actual services performed by the services should help alleviate investor concerns that the interests of investor and servicer are not sufficiently aligned.

Today PLS investors do not exercise direct leverage over or have a direct relationship with the servicer. They do not receive loss mitigation reports or have the right to review the servicers' loss mitigation decisions. Even termination of the servicer for cause requires a high level of red tape. Thus, to the extent that servicer compensation structure and requirements could be written into the PSA in a manner contemplated by this new compensation proposal, many investor concerns could be addressed.

Public comments on the proposal will be accepted for 90 days and should be emailed to Servicing_Comp_Public_Comments@fhfa.gov.

Read the full paper: Alternative Mortgage Servicing Discussion Paper