Fannie Mae's economists are painting a much improved picture for the economy in the coming months with encouraging news in the area of business investment, manufacturing, and business spending on structures. Despite the unexpected drop in consumer spending in July the company's economists, Doug Duncan, Orawin T. Velz, and Brian Hughes-Cromwick, expect growth "to moderate from the above-par pace of the second half of this year and average 2.5 percent for all of 2015, an acceleration from a projected 2.0 percent in 2014. However, given the strength expected going into next year, the 2.5 percent pace may be more of a lower bound on growth expectations."

Housing however is a different story; it is "struggling to gain traction" the company's September forecast says. Activity improved at the beginning of the third quarter with both single and multifamily housing starts rising in July for the first time in three months although that increase was driven by the multifamily sector which accounted for 40 percent of starts, the highest share since the mid-1980s. Multifamily construction is not the strong contributor to GDP that the single family sector is.

Home sales were mixed in July. Existing home sales were strong, rising for the fourth straight month to a 10-month high and pending sales suggest that sales would continue to rise through the quarter. Contract signings for new home purchases were weak, moving down in July to a level well below the second quarter average. The later development was at odds with homebuilder confidence which, in the August National Association of Home Builder (NAHB) survey, rose for the third consecutive month to the highest level since January.

Home prices have continued to rise, due in part to limited inventory and a sharp decline in distressed sales over the last year. Those sales represented 9.0 percent of transactions in July compared to an average of one-third of all sales in 2009.

The strength shown by measures of pending sales contrasts with data on purchase mortgage originations which remain a soft spot for the mortgage market. According to the Mortgage Bankers Association, purchase applications have trended down over the past three months to the lowest level since February even as interest rates have also declined. This suggests that the pace of improvement in housing indicators will likely be subdued for the rest of the year.

Cash sales may explain some of the gap between home sales and mortgage applications. The share of these sales is still elevated by historic standards but has declined more than 10 percentage points from the peak. This is good news for first time homebuyers as it means less competition from investors who make up the bulk of cash buyers. But the National Association of Realtors has bad news as well. Its first-time buyer affordability index edged down in the second quarter to the lowest reading since the end of 2008. The economists say that until and unless there are signs of a resurgence in first-time homebuyer demand to replace investor demand they will remain cautious on their outlook for the housing market.

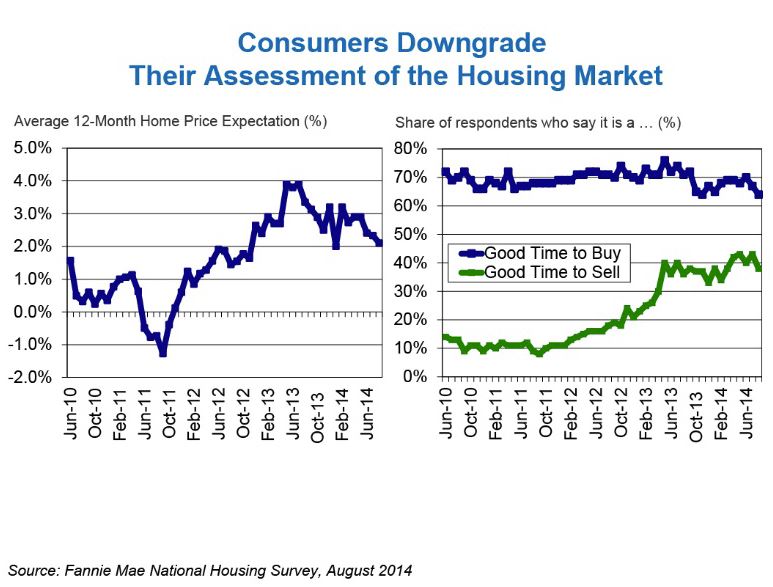

Fannie Mae's August edition of its National Housing Survey posted a decline in the share of consumers who think it is a good time to buy a house to 64 percent, tying the all-time survey low. At the same time those who thought it was a good time to sell decreased to 38 percent and expectations about home price increases fell as well.

This weakening sentiment, the economists say, was due partly to respondents' assessments of their own financial situations; fewer reported increased household incomes. Data from this and other sources provide support, they say, for their view that housing's growth this year and next will be modest.

One positive note is interest rates which have recently stabilized near 2014 lows. Mortgages rates have moved in a very tight range of 4.10 percent to 4.12 percent over the past four weeks and the economists expect them to hold relatively study for the remainder of the year then trending up to 4.5 percent by the end of 2015.

The economists say their forecast for the housing and mortgage market has changed little from August. "We expect total mortgage originations to decline 42 percent from 2013 to $1.11 trillion in 2014 and drop another 5.0 percent to $1.05 trillion in 2015. We expect the mortgage market to skew more toward the purchase market, with the refinance share trending down to 26 percent in 2015 from a forecast of 39 percent in 2014." They also expect that, after posting six consecutive annual declines, total single-family mortgage debt outstanding will increase slightly this year and strengthen modestly in 2015.