Sometimes government gets it right. The Urban Institute (UI) clearly thinks that the Home Affordable Refinance Program, at least in its second iteration, was one of those times. The history of HARP, as the program is known, is the subject of a post in UI's Urban Wire blog credited to four UI analysts*.

They say that, before 2009, borrowers who had little or no equity in their homes could not refinance, even if their mortgages were current. With home prices plummeting, the number of homeowners in that situation was rapidly expanding and many were stuck in loans with 6 percent or higher rates, even as current rates fell below 4 percent. This cost borrowers significant savings and deprived the struggling economy of much needed stimulus.

In 2009, the two government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, at the prompting of their conservator and regulator, the Federal Housing Finance Agency (FHFA), took their first crack at solving the problem, allowing GSE borrowers who lacked sufficient or even any equity to refinance into lower interest HARP loans.

The program was not terribly successful. UI says the rules the GSEs and mortgage insurers (MIs) had put in place over the years to manage risk locked out the very borrowers HARP was designed to help. In 2012 there was a redo which, in addition to changing these rules, eliminated the cap on loan-to-value (LTV) ratios entirely.

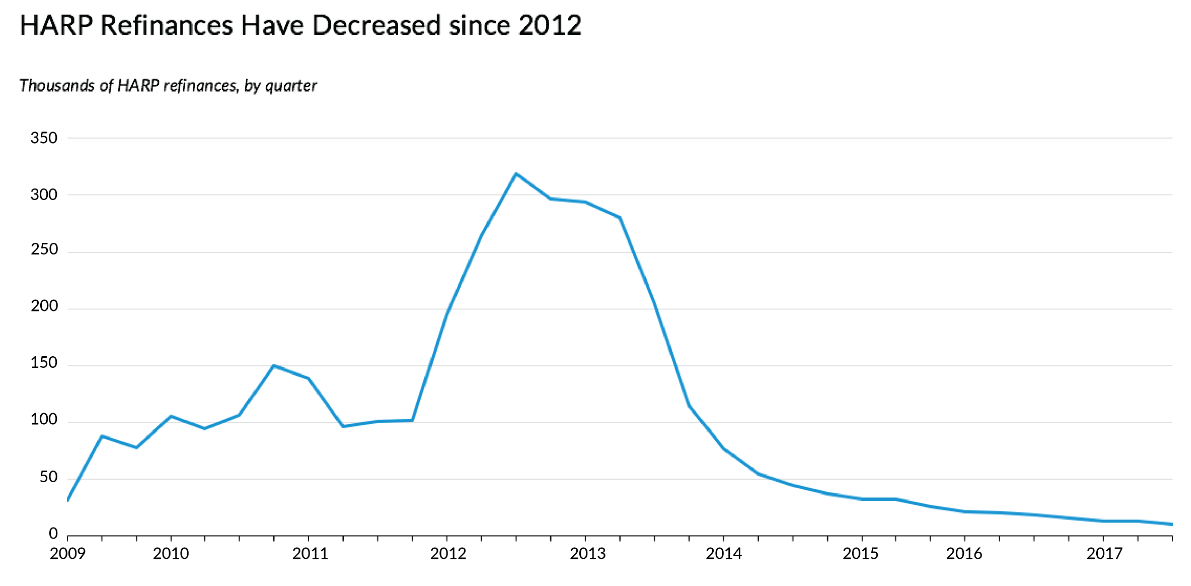

UI calls the subsequent impact "huge", and HARP "arguably the most successful housing policy initiative coming out of the crisis." An FHFA refinance report says that from 2009 to 2017 there were about 3.5 million refinances completed through the program, with nearly 2 million, or 57 percent, completed in the two years following the revamp. On average, refinancing reduced the loan rate by 1.66 points, and saved the borrower $200 per month. Aggregate savings thus far exceed $35 billion.

The program is limited to borrowers with existing loans originated prior to 2009, a population that has dwindled in recent years, so participation has dwindled as well. Ten thousand HARP refinances were completed in second quarter of 2017 in comparison with over 300,000 at the peak in Q3 2012.

HARP was designed to expire at the end of 2013, but that date has been extended several times. It is currently slated to end on December 31, 2018, with fewer loans anticipated going forward. FHFA estimated in March that there were 143,000 borrowers who could still benefit from the program, a modest number that probably overstates those who will participate, especially if interest rates rise.

UI says the legacy of the program goes beyond the borrowers who were helped and the money saved. "Overhauling the original HARP program required policymakers and industry participants to cut through prohibitive obstacles that not only held this program back, but slowed refinancing down more broadly." There were three significant impediments in the original design.

- The new loans required a manual appraisal, adding to the cost per loan and risks arising from committing to the property's value.

- Lenders had to secure new mortgage insurance, again adding to costs and the risk that no mortgage insurer would take on the risk of insuring a high LTV loan.

- Lenders didn't want the risks associated with the new loans which effectively limited borrowers to refinancing with their existing lender. Without competition, borrowers would see worse pricing and less savings.

The GSE's and MIs had to recognize that their rules were designed to mitigate risks in making new loans, not those where they already held the credit risk. The GSE didn't need to know with precision the updated value of the property, the MI did not need to decide whether the risks posed were worth backing, nor did they need to apply the same stringent underwriting to filter out risk. They already owned that risk. Indeed, to the extent the old rules kept borrowers from participating in the program and reducing their monthly mortgage payment, the GSEs and MIs were exposed to greater risk of borrower default.

With this in mind, policymakers adjusted the rules:

- The GSEs produced appraisals through their automated valuation system. This provided accurate-enough valuations for the required mortgage-backed securities disclosures.

- Mortgage insurers transferred their coverage from the old loan to the new one, avoiding all the costs and frictions of running an entirely new approval process.

- The GSEs reduced the underwriting assurances they required of lenders making HARP loans, even if the borrowers were coming from other lenders.

These steps allowed lenders to automate their participation in HARP, both for their existing borrowers and those currently serviced by other lenders. This led to a dramatic increase in the number of borrowers who benefited and what they saved in doing so. By expanding and deepening borrowers' monthly savings, the GSEs benefited through a reduction in default rates among many of their higher-risk borrowers.

UI says the HARP revamp was instructive and the GSEs and FHFA are now going to apply the lessons learned to their high-LTV lending in general. They will remove those HARP hampering impediments from guidelines for refinancing all borrowers who take out a loan backed by the GSEs after October 1, 2017. The changes will apply to those who have no more than 5 percent equity in their home, and have been paying on time for at least 15 months.

HARP was always intended to be temporary, but the new GSE programs will be permanent. UI says the new rules will make it easier for all borrowers who find themselves with little equity to refinance at competitive rates, putting more money in their pockets each month, lowering the risk to the GSEs and stimulating the economy. "And for that, we have HARP to thank."

*Linda Goodman, Jim Parrot, Karan Kaul, and Jun Zhu