Hard to believe it's already that time again, but Freddie Mac's Economic and Housing Research Group are out with their forecast for 2018. The headline is that they expect the economic environment to remain favorable for housing and mortgage markets, with moderate economic growth of about two percent, solid job gains, and low mortgage interest rates. In other words, Deja vu all over again.

There will be, they say, three trends driving the 2018 mortgage market: an increase in purchase mortgage volume; cooling of rate refinance activity, and more borrowers tapping their home equity. They put forward specific expectations for each.

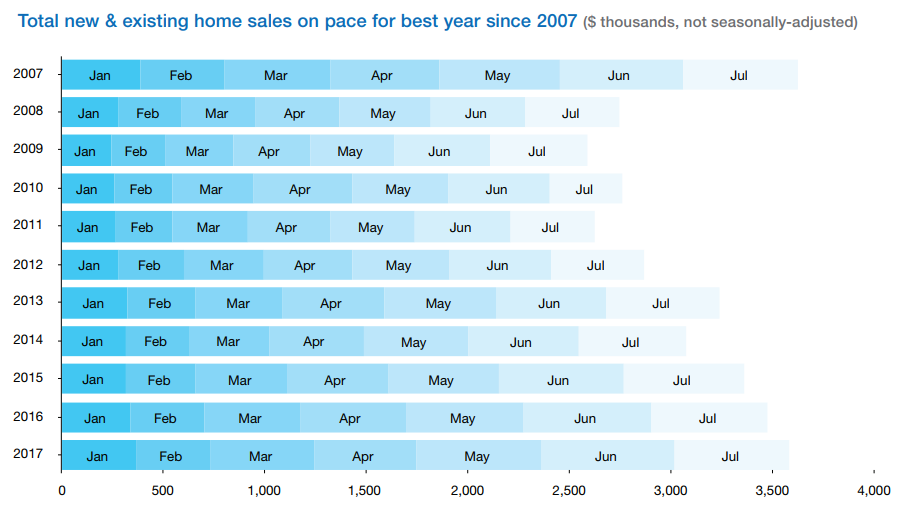

Increases in the volume of purchase mortgages will be the result of modest gains in both home sales and home price growth. Thus far in 2017, home sales are the highest in a decade, but are unlikely to grow by much going forward. Inventory problems will continue to limit sales in the short term and longer-term trends like the aging of the population and declining mobility across all age groups will hold down existing home sales. New home sales will become a more important force once single-family construction picks up. Freddie Mac forecasts home sales, both new and existing, will increase by about 2 percent next year.

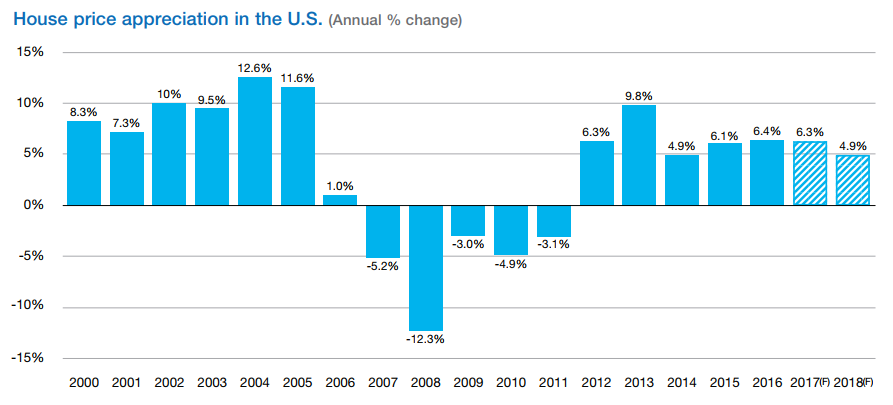

Home price growth has been strong. FHFA reports growth in its House Price Index (which includes Freddie Mac's purchase mortgage price data) at 6.6 percent from the second quarter of 2016 to the same period in 2017 and, in some markets, prices are up 10 percent on an annual basis. Freddie Mac sees gradual gains for residential construction and moderate increases in mortgage interest rates reducing price growth next year to an average of 4.9 percent.

The mortgage market has been shifting slowly, and often in fits and starts, from one dominated by refinancing to a more purchase oriented one. Freddie Mac's economists expect that will continue next year. The refinance share of the market will decline to around 25 percent, the lowest since 1990.

Refinancing has been sustained at a high level for some years by rate refinancing. With rates moving up - although that has also been by fits and starts, the potential for this type of refinancing has declined. Freddie Mac says one concern is that a sudden rate spike could virtually eliminate it. They cite as an example, a 2-percentage point jump in the 30-year rate that occurred from the third to the fourth quarter in 1994. The dollar volume of refinancing fell by 80 percent in response. A similar spike now would be likely to prompt the same outcome.

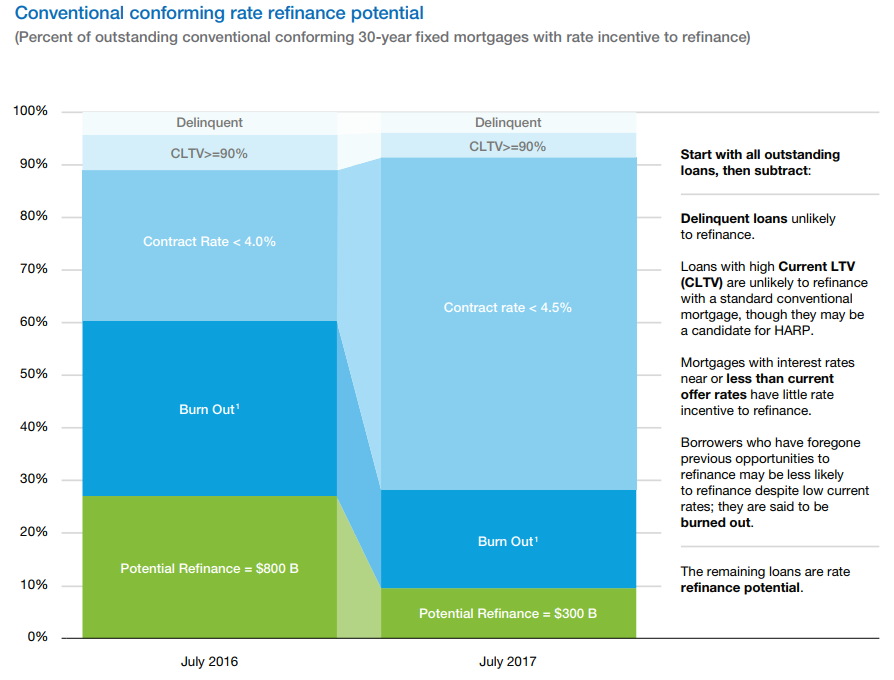

Even if rates remain relatively flat, refinance volumes are likely to decline. Exhibit 5 shows Freddie's assessment of rate refinance potential in July 2017 versus that of a year earlier. Even with little change in interest rates, 30-year conventional rate refinance potential next year will be the lowest it has been in years.

The economists note however, that refinancing has not fallen as much as their estimate of rate refinance potential. While Exhibit 5 shows a potential decrease of 63 percent in refinancing originations, in reality they have only fallen by 48 percent. The exhibit covers only part of the market and other sources of refinance are filling in some of the gap left by rate refinancing.

Shortening of the rate term has become a popular reason for refinancing, representing 35 percent of those originations during the second quarter of this year. Term refinancing has had at least a 30 percent share every quarter since early 2013 as low rates give borrowers the ability to pay down principal faster.

Refinancing from FHA loans into conventional financing is another source of originations. CoreLogic estimates as many as 250,000 FHA borrowers could chose this route to rid themselves of ongoing FHA annual insurance premiums.

As rate refinances ebb, cash-out refinancing has increased. Rising home prices have helped existing homeowners grow their equity and those looking to remodel, consolidate debt, or pay off student loans, are looking to that equity to do so. Some chose to cash out by refinancing into a larger mortgage, while others are tapping equity through a second lien, usually a Home Equity Line of Credit (HELOC).

Freddie Mac's Quarterly Refinance Statistics track conventional prime cash-out refinancing. In the second quarter of 2017, homeowners cashed out $15 billion in equity compared to $13.8 percent the previous quarter and $19.1 billion in the fourth quarter of 2016.

Those amounts are paltry when compared to the cash-out refinancing book in 2006 and 2007. In those two years homeowners pulled out between $80 and $90 billion in equity each quarter. Further, while cash-out represented about 30 percent of the aggregate amount of refinancing in those two pre-crisis years, it represented only half that in the most recent period this year.

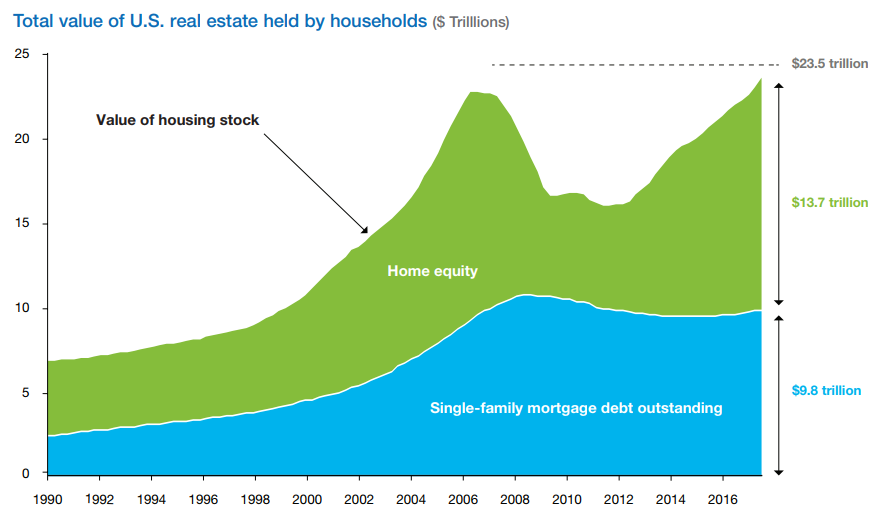

Freddie Mac says homeowner equity was up to $13.7 trillion in the first quarter of this year. As home prices keep rising, cash-out activity is also likely to rise. Even if mortgage rates rise or remain flat, cash-out will become a larger and larger share of total refinance activity. Typical cash-out refinancings result in a loan amount three to five times as large as the equity cashed out. If that extracted equity averages $20 it would mean refinancing volume of about $300 billion each year. But, the Economists say, "Even if the share of cash-out refinance activity increases dramatically, the level of overall cash-out activity will likely remain well below the levels we saw last decade and mortgage debt growth will remain modest by historical standards."