The Fannie Mae National Housing Survey was released yesterday. Doug Duncan, Vice President and Chief Economist at Fannie Mae summarizes the survey findings...

“Our survey shows that consumers see a mixed outlook for housing and homeownership....These findings indicate a return to a more balanced and realistic approach toward housing. While this will likely weigh on the housing recovery in the near-term, it should, over time, help to build a stronger and healthier market focused on sustainable homeownership.”

SURVEY METHODOLOGY:From June 12, 2010 – July 14, 2010, 3,399 telephone interviews with Americans age 18 and older were conducted by Penn Schoen Berland. This included a random sample of 3,001 members of the general population, including 870 homeowners, 1,020 mortgage borrowers, 900 renters, and 289 underwater borrowers (those who report owing at least 5% more on their mortgage than their home is worth). The overall margin of error for the general population sample is +/- 1.79% and larger for sub-groups. An additional oversample of 398 random national delinquent borrowers was also polled. The margin of error for the delinquent borrower oversample is +/- 4.91% and larger for sub-groups. Delinquency was defined as not having made a mortgage payment in the past 60 or more days.

OVERVIEW OF KEY FINDINGS

Survey excerpts, tables and charts taken from the Survey Presentation....

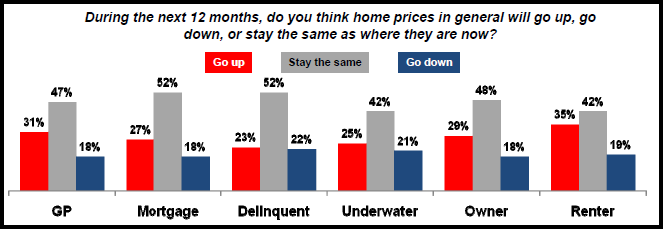

HOME PRICES: A large majority of Americans (78 percent) believe that home prices either will remain flat or go up over the next year, up five points from the beginning of the year. Forty-seven percent believe prices will hold steady, while 31 percent think they will go up. This is a notable shift from January 2010, when these numbers were 36 percent and 37 percent, respectively.

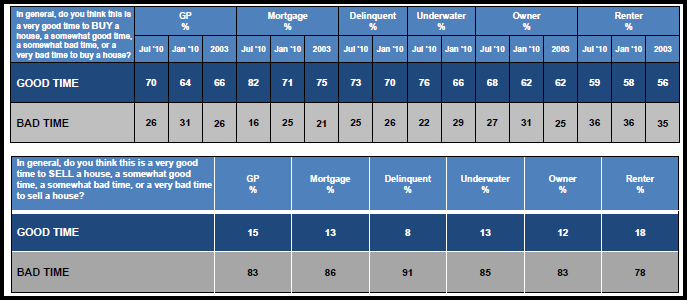

Thirty-nine percent think rental prices will increase over the next 12 months, while 46 percent said they will stay the same. Consumers continue to believe it is a buyers' market; 70 percent said it is a good time to buy a house, up six points from January. However, 83 percent believe it is a bad time to sell a house.

GOOD TIME TO BUY, BAD TIME TO SELL: 70% of Americans think it is a good time to buy a house, up from 64% in January 2010, and 36% think now is a very good time to buy a house. More than three-quarters of Mortgage borrowers and Underwater borrowers think it is a good time to buy. 83% of Americans think it is a bad time to sell a house. 91% of Delinquent borrowers think it is a bad time to sell a house, with 67% thinking it is a very bad time to do so...

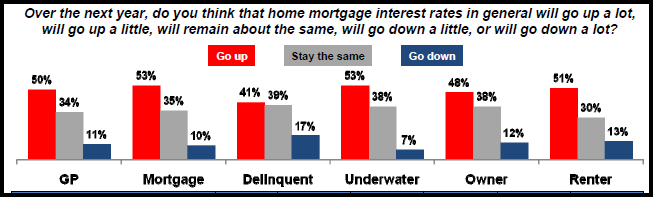

MORTGAGE RATES: Americans expect home mortgage interest rates to go up rather than down over the next year by a ratio of 5 to 1.Among the sub-groups, the highest percentages expecting mortgage interest rates to rise over the next 12 months are among Mortgage borrowers and Underwater borrowers. Delinquent borrowers are more likely than other groups to think rates will remain the same or go down

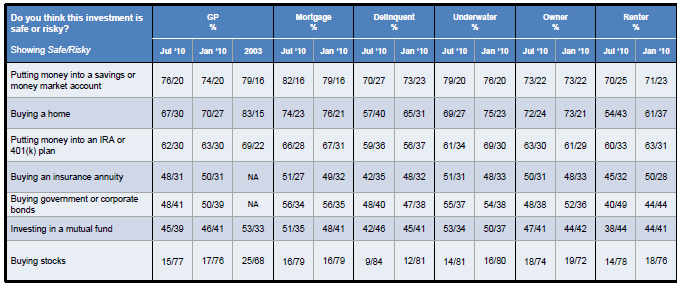

IS BUYING A HOME A SAFE INVESTMENT ?: Fewer Americans consider buying a home a safe investment than in January 2010 or 2003.Although 67% of Americans think buying a house is a safe investment, this is down 3 points from January 2010 and 16 points from 2003 – the largest declines among all tracked alternatives over both timeframes. The perception that buying a home being is a safe investment has decreased among all sub-groups since January 2010, especially among Delinquent borrowers, Renters, and Underwater borrowers (down by 8, 7, and 6 points, respectively). Mortgage Borrowers and Owners view purchasing a house as a safer investment than the General Population and the rest of the sub-groups

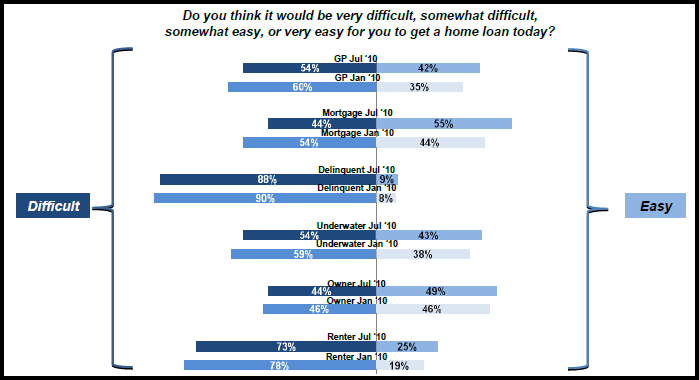

QUALIFICATION: Most Americans think it would be difficult to get a home loan today. However, this sentiment is waning: 42% of Americans think that it would be somewhat easy or very easy to get a home loan today up 7 points since January 2010. The vast majority of Delinquent borrowers continue to believe it would be difficult.

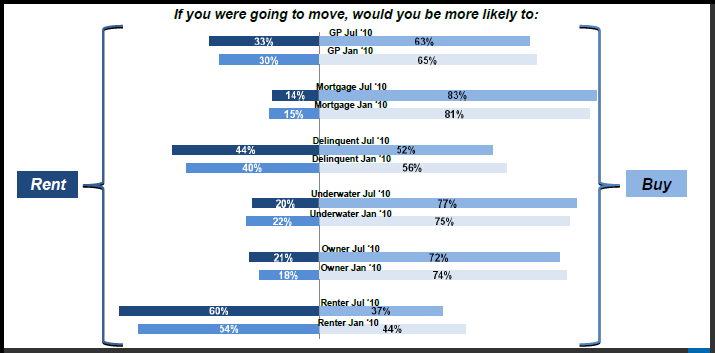

RENT OR OWN?: Americans overwhelmingly believe that owning makes more sense than renting because of potential rent increases and value appreciation – consistent with January 2010. This is true of Renters as well, although there is a 6 point decrease since January 2010. Mortgage borrowers have a strong preference for owning, including Underwater borrowers.

BUT....the number of respondents who said they would be more likely to rent rather than buy their next home if they were going to move increased from 30 percent in January to 33 percent in July. A majority of renters said they would be more likely to rent their next home if they were to move, increasing significantly from 54 percent in January to 60 percent in July, even though 69 percent of renters think it makes more sense to buy a home.

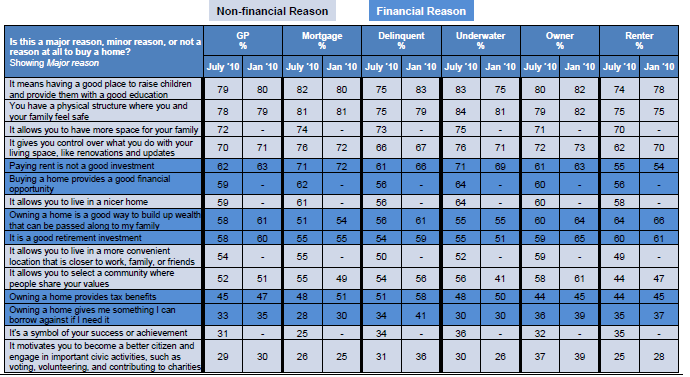

WHY BUY A HOME?: Non-financial considerations, such as accessing good education and safety, continue to trump financial reasons for owning a home, although reasons for homeownership in general have degraded since January 2010 among Delinquent borrowers and Renters

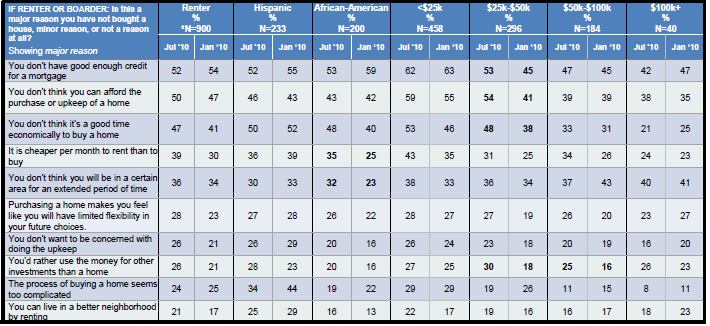

WHY NOT BUY A HOME?: Poor credit remains the top reason given by Renters for not buying a home, followed closely by purchase/upkeep affordability, and not a good time economically to buy a home. The importance of the top three reasons given for not buying changed materially as perceived barriers since January 2010 in the $25k-$50k income segment. Since January 2010, African-Americans increasingly believe it is cheaper to rent than to own (up 10 points) and desirable to rent for mobility flexibility (up 8 points)

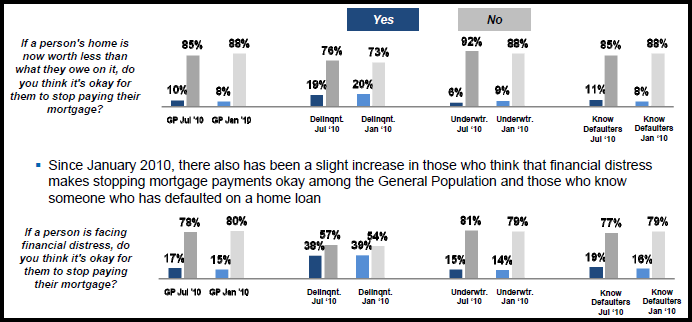

STRATEGIC DEFAULTS: Since January 2010, there has been a slight increase in those who believe it is acceptable to stop making payments if a borrower is underwater among the General Population and among those who know someone who has defaulted on a home loan. Delinquent borrowers have remained almost flat and Underwater borrowers declined in this regard

75% of Mortgage borrowers consider their mortgage payment to be most important, in line with the January 2010 results. 50% of Delinquent borrowers consider their mortgage payment to be most important, down meaningfully from 57% in January 2010. 28% of Delinquent borrowers consider paying their utility bills as most important – two and one-half times more than the incidence among all Mortgage borrowers.

OTHER OBSERVATIONS....

- 77 percent% of respondents expressed some degree of confidence that they would receive the information they need to choose the right loan if they bought or refinanced a home today, down one point since January. However, only 48% said they are “very confident” (compared to 47% in January).

- 80% of Renters think they would have to make a financial sacrifice in order to own a home, with 55% thinking it would require a great deal of sacrifice. Even for Renters in the $50k to $100k income bracket, 48% think that owning a home would require a great deal of financial sacrifice

- 65% of Mortgage borrowers are very satisfied with their current mortgage’s features, but only 22% of Delinquent borrowers feel the same about their current mortgages. Furthermore, 36% of Delinquent borrowers are not at all satisfied with the features of their current mortgage

- 74% of Americans would prefer getting a fixed-rate mortgage over floating-rate alternative. The number rises to 93% among Underwater borrowers.

- Even though 6 in 10 Americans think the U.S. economy is on the wrong track, only 13% of Americans expect their personal financial situation to get worse in the next year (down by 4 points). Those who own their home outright, more than any other sub-group, expect their financial situation to remain about the same

- 82% of Americans think that a high rate of homeownership is important to the overall economy – 2 points higher than in January 2010.The biggest positive shift is among Underwater borrowers, of whom 89% (5 points up) perceive homeownership as an important factor for the overall economy. Renters are the least likely to view homeownership as important to the overall economy and there has been a 5 point downward shift since January 2010

HERE is the survey factsheet

Doug Duncan adds, "Although most Americans believe that home prices have bottomed, they are adopting a much more cautious approach toward buying. Homeowners and renters alike continue to be wary of taking on risk, and they are less confident in the long-term outlook for housing.”

MND Perspective...

Common Sense Not Found in Automated Underwriting Engines

Expanding the Pool of Eligible Homeowners: Common Sense Underwriting Needed