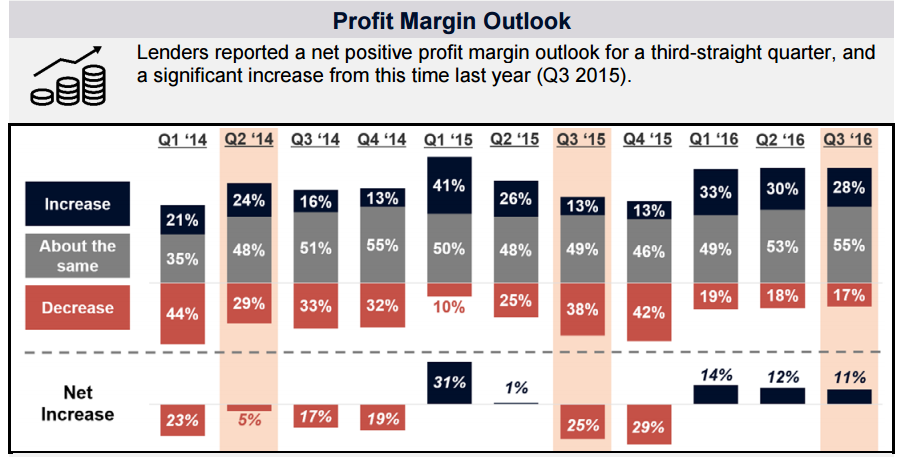

Mortgage lenders are feeling more positive about profits this quarter than they did in the second quarter with 28 percent of those surveyed by Fannie Mae expecting an increase over the next three months. Seventeen percent expect lower profits and 55 percent do not anticipate a change. It was the third straight quarter that lenders reported a net positive profit margin outlook, and was a significant increase from the third quarter of 2015. The largest year-over-year increases in net profit margin outlook were seen among smaller institutions and credit unions.

Fannie's third quarter Mortgage Lender Sentiment Survey asked the optimistic respondents what they expected would drive their higher profits and the top two reasons given were operational efficiency and technology and consumer demand. The company said these are the top reasons for increased profitability cited in every Lender Sentiment Survey. Those expecting profits to decline however were much less likely in the recent survey to cite regulatory compliance as a driving factor, down to 39 percent, a survey low, from 61 percent in the third quarter of last year. Competition from other leaders was the top reason cited for the eroding profit outlook at 46 percent, knocking the compliance answer out of first place for the first time in survey history.

"For lenders, the most encouraging aspect of the survey is a significantly brighter profit outlook this year compared with last year," said Doug Duncan, senior vice president and chief economist at Fannie Mae. "More lenders, on net, reported a positive profit outlook for the third straight quarter, the first time that has happened since the survey's inception. Their perception of profit outlook in the third quarter of this year is in stark contrast to the third quarter of 2015, when a sizable net share of lenders expected a deteriorating profit outlook over the next three months. It appears that lenders have incurred the increased compliance costs from new regulations such as TRID, and are now on a stabilized though higher-cost footing to focus on growth strategies. However, any upward move in interest rates will bring reduced origination volumes and competitive pressure on profits. That pressure would likely result in lowered expectations and additional demands for cost containment."

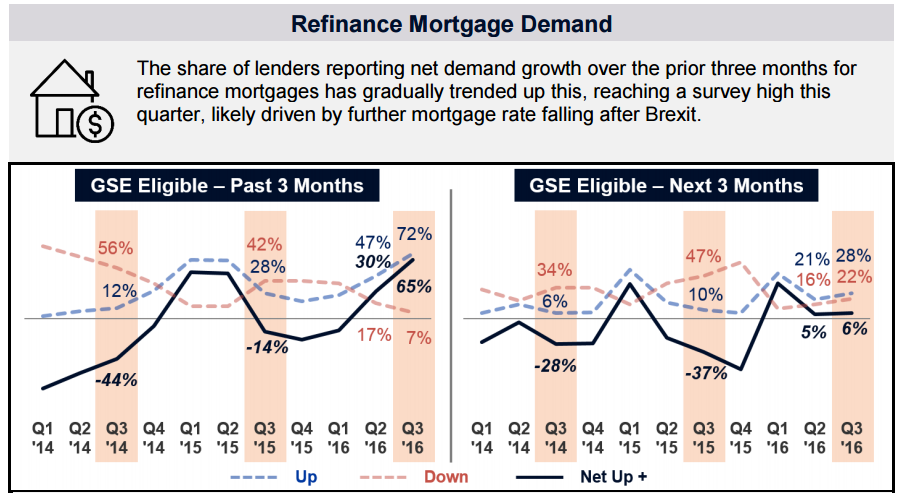

Lenders report they have experienced a net growth in demand over the past three months for refinancing across all loan types. That number reached a survey high this quarter, likely driven by further mortgage rate declines post-Brexit, Fannie says.

For purchase mortgages, the share of lenders reporting net demand growth over the prior three months is similar to this time last year (Q3 2015), across all loan types.

Net demand growth expectations for the next three months for both refinancing and purchase mortgages also remain near levels seen a year ago.

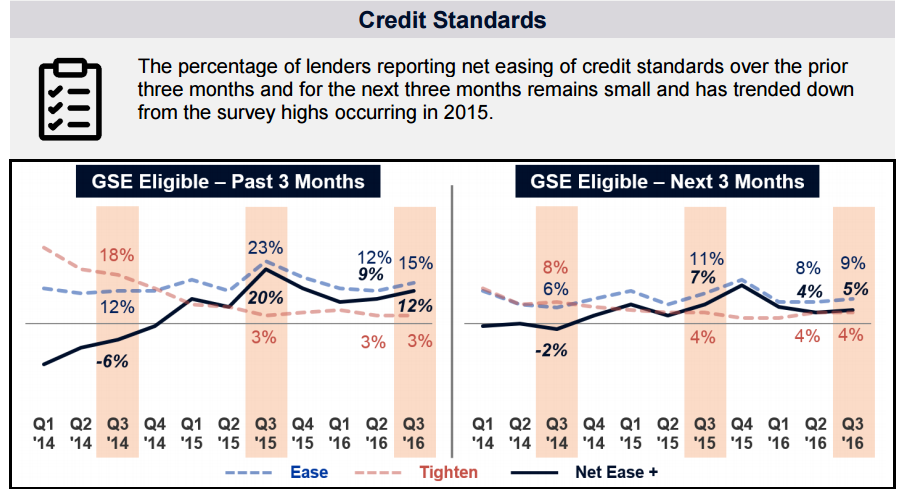

There has also been modest net easing of credit standards over the last three months, although the numbers reporting net easing has gradually trended down from the survey high in the third quarter of 2015. Lenders report on that they expect credit to continue to ease on net over the next three months although the numbers of those responses are also trending down.

This quarter, more lenders reported expectations to grow GSE (Fannie Mae and Freddie Mac) shares and reduce portfolio retention shares. More lenders also reported they expect to decrease their share of MSR sold and increase their retention rate. This reverses the trend earlier in the year.

Fannie Mae's Mortgage Lender Sentiment Survey polls senior executives of its lending institution customers on a quarterly basis to assess their views and outlook across varied dimensions of the mortgage market. The third quarter survey included respondents from 200 institutions, 65 percent of which were defined as "smaller", with volumes under $175 million. Sixty-five were mortgage banks, 19 were depository institution and 49 were credit unions. Seven were not classified.