With interest rates expected to rise and most homeowners who could benefit from refinancing having done so, mortgage bankers are not expecting the sometimes record profits of the last year or so to continue. Fannie Mae's third quarter Mortgage Lender Sentiment Survey (MLSS) found just short of a majority of respondents expecting their profit margins to decline over the next three months, although that has also been the primary sentiment for the past three quarters.

The current survey found 46 percent of lenders expecting a decrease in profits, down from 69 percent in the prior survey. Thirty-eight percent believe their profits will be unchanged and 15 percent expect them to be higher.

Those expecting slimmer margins cited increased competition and changing market conditions for their pessimism, while GSE pricing and policies and strong consumer demand were the top reasons given among lenders with a more positive profitability outlook.

"On net, mortgage lenders' profitability outlook improved slightly from last quarter, although more lenders than not continue to expect profit margins to decline in the months ahead," said Fannie Mae Vice President and Deputy Chief Economist Mark Palim. "The primary-secondary spread, an indicator of potential profitability, remains wider than the previous decade's average - a positive sign for lenders - though in August it was at its narrowest since February and 53 basis points below the peak seen in August 2020. While lenders continue to overwhelmingly cite increased competition as their primary concern regarding future profitability, the share citing personnel costs for their diminished profit margin outlook increased significantly, suggesting that mortgage lenders' ability to efficiently manage their workforces will be critical to their bottom lines as competitive pressures remain intense."

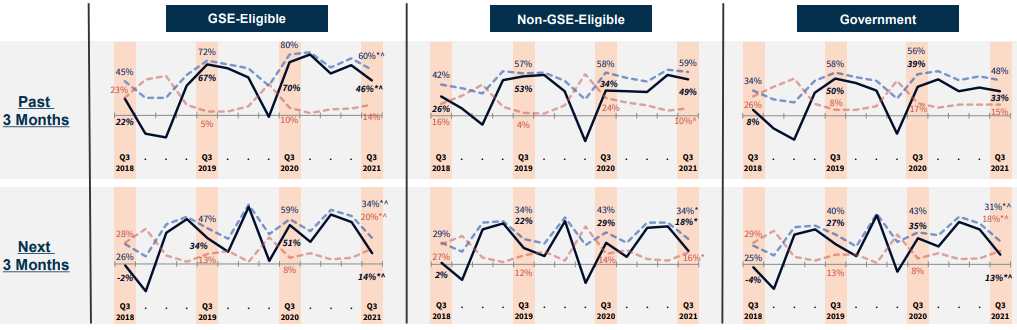

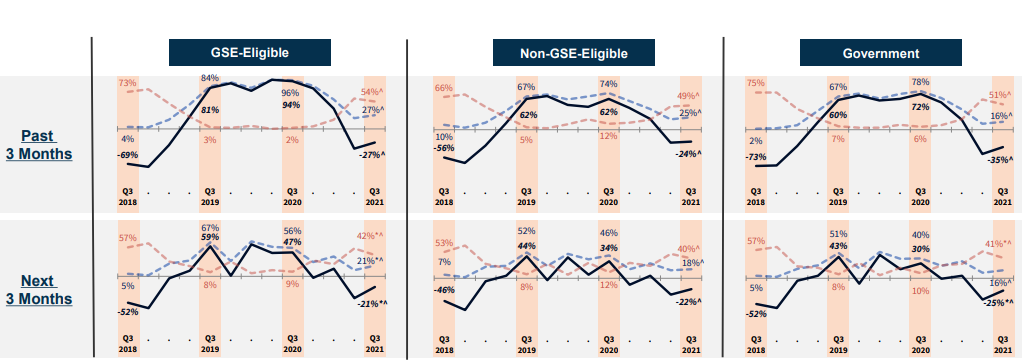

More lenders reported diminished demand for purchase demands over the last three months than previously, but reported demand for refinancing improved. Expectations for demand over the next three months remained positive on net for purchase mortgages but was slightly negative for refinances.

Purchase Demand

Refi Demand

"Mortgage lenders appear to have adopted a more neutral posture, reporting to us via the MLSS mixed expectations for purchase and refinance mortgage demand over the next three months," Palim continued. "In the third quarter, more lenders than not reported expectations that purchase mortgage demand will continue to grow, though the total share expecting such growth fell substantially compared to the previous quarter. Meanwhile, a plurality of mortgage lenders expects refinance activity to continue to wane from the highs of the past year and a half - even so, their outlook on likely refi volumes was improved compared to the prior quarter. Of the lenders who expect purchase mortgage demand to decrease in the coming months, high home prices and a limited supply of homes for sale were the primary reasons given - these were also among the top reasons provided by the 63 percent of consumers who believe it's a 'bad time to buy a home', according to our latest Home Purchase Sentiment Index."

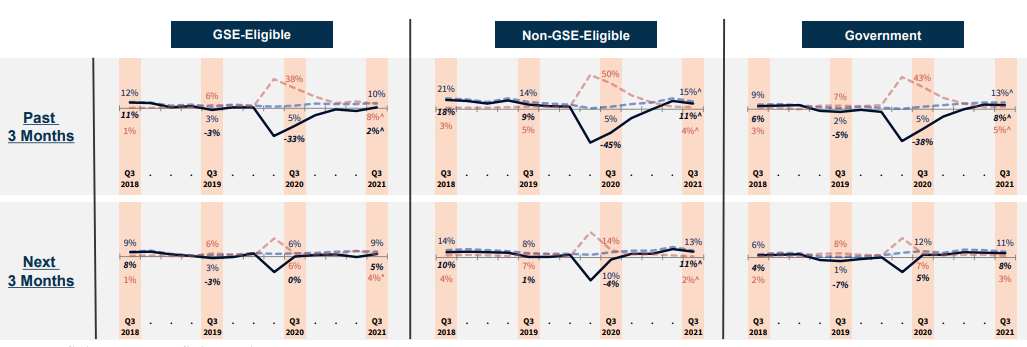

More lenders reported an easing of credit standards over the past three months and the share expecting them to ease further for GSE-eligible loans also grew. Expectations declined for easing of non-GSE credit and remained flat for government loans.

Credit Standards

A total of 211 senior lending executives responded to the Q3 2021 survey. Eighty-four represented mortgage banks, 68 worked for depositories, and 39 for credit unions.