While Irma is battering the Florida coast and costing untold billions in damages, Black Knight Financial Services released information about the ultimate costs to the housing finance industry of Hurricane Harvey. The disaster that struck primarily in the Houston/Port Arthur/Beaumont, Texas area may affect mortgage performance more than did Hurricane Katrina in 2005. Both the magnitude of the rainfall, which hit 50 inches in some locations, and the population of the area magnified the Hurricane's impact.

The current edition of Black Knight's Mortgage Monitor says the FEMA-designated disaster areas have over twice as many mortgaged properties as did the areas ravaged by Katrina, 1.18 million properties versus 456,000, and at $179 billion, nearly four times the unpaid principal balance.

The government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac together have 56 percent of the loans in the Harvey disaster area, 661,000 in total. While far fewer in number, the high-dollar value of portfolio loans has increased those lenders exposure. They have loans with unpaid balances that are, on average, $90,000 higher than those held in either agency or non-agency securities.

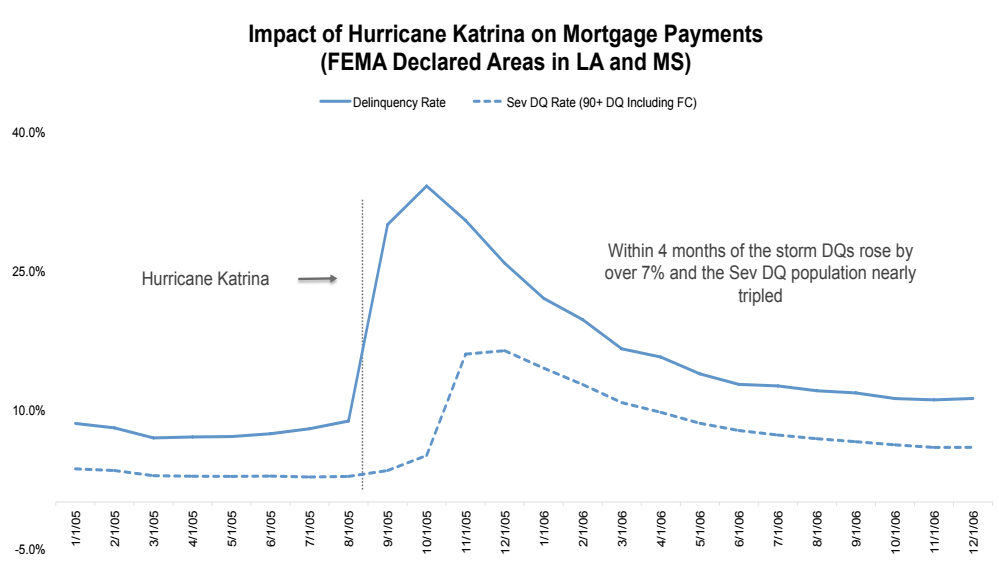

Within two months of Katrina, delinquencies among borrowers in Louisiana and Mississippi's disaster areas spiked 25 percent, peaking at 34 percent of mortgaged homes. Four months post-hurricane serious delinquencies, those over 90 days past due or in foreclosure, rose 14 percentage points to 16 percent.

Black Knight says, should Harvey victims pursue a similar pattern, the hurricane's aftermath could mean 300,000 borrowers would miss at least one mortgage payment over the next two months with 160,000 becoming seriously delinquent within four months.

The Monitor

also looked at 2nd quarter origination volumes and found that while

overall mortgage lending saw a 20 percent increase over Q1 2017, total volumes

were down 16 percent from Q2 2016. Additionally, although purchase lending hit

its highest level in 10 years, the total number of

purchase mortgages being originated still falls far below pre-crisis

(2000-2003) averages. As Black Knight Data & Analytics Executive Vice

President Ben Graboske explained, more stringent credit requirements enacted in

the wake of the Great Recession may be hampering purchase lending volumes.

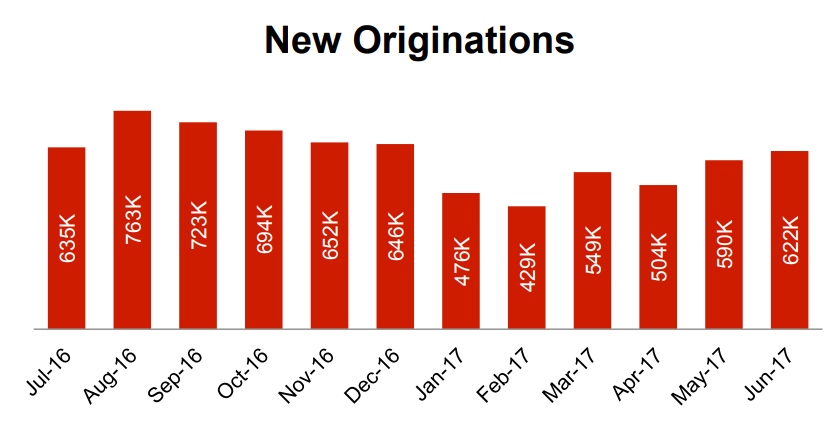

"We saw positive growth in lending in the second quarter, with $467

billion in first lien mortgages originated," Graboske said. "While down 16

percent from a year ago, that marks a 20 percent increase in mortgage lending

over Q1. Drilling down into the make-up of those originations, we see that refinance

lending made up just 31 percent of all Q2 originations - the lowest such share

in over 16 years. Refinance volumes were down as well, falling 20 percent from

Q1, but that drop was more than offset by a 57 percent seasonal rise in

purchase lending. Purchase originations totaled $321 billion in Q2 2017; up six

percent from last year, and the highest quarterly volume since 2007. As a

result of growing average loan amounts for purchase originations, the total

dollar amount of purchase originations is higher than averages seen from

2000-2003, prior to both the peak in home prices and the Great Recession that

followed. This is partly due to rising home prices, but also comes as a result

of an all-but-total absence of second lien usage for purchases, a shift toward

high-dollar/low-risk loans among non-agency lenders and a higher share of cash

purchases at the lower end of the market.

"However, the number of purchase loans being originated still lags the

pre-crisis average by almost 30 percent; while overall purchase origination

volumes are strong from a total dollar amount perspective, the market still

does not appear to be performing at peak capacity. One key cause is the more

stringent purchase lending credit requirements enacted in response to the financial

crisis. Consider that borrowers with credit scores of 720 or higher accounted

for 74 percent of all Q2 2017 purchase loans as compared to a pre-crisis

average of 47 percent. Today, there are 65 percent fewer purchase loans being

originated to borrowers with credit scores below 720 than in those years. The

lack of credit availability for those borrowers is causing a strong headwind

for the purchase market. Using 2000-2003 averages as a measure, as many as

645,000 purchase loans were not originated in Q2 due to tighter lending

standards. To put it another way, the purchase market is operating at less than

two-thirds of peak capacity because of these factors."

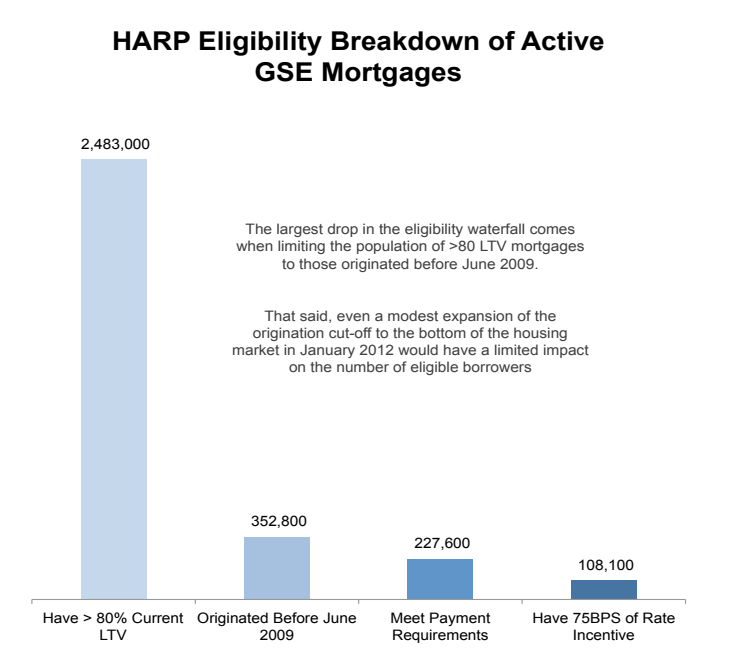

The Federal Government has announced an extension of the Home Affordable Refinance Program (HARP) through the end of 2018 but Black Knight concludes it will have little effect as the remaining pool of HARP-eligible borrowers is relatively small. HARP is designed to allow homeowners with extremely high loan-to-value (LTV) ratios to refinance but, since the program began some 3.5 million borrowers have taken out HARP mortgages and rising home prices have eliminated the need for the program among many other homeowners. Black Knight estimates that at the end of July only about 108,000 borrowers remain who could qualify for the program and have at least 75 basis points of interest rate incentive.

Opportunities for traditional refinancing are at calendar year high, with interest rates again below 4.0 percent. Except for a single week in July, rates have been very consistent over the past 12 weeks. While 600,000 borrowers refinanced in the second quarter, rising prices have replaced them in the refinancing pool by about the same number of borrowers who now have enough available equity. What Black Knight calls "a delicate balancing act" has kept the refinance pool steady over the last three months.

As of August 17, an estimated 4.41 million borrowers could both likely qualify for a refinancing and have an interest rate incentive to do so. This is the most so far in 2017, but has not changed more than a hair since May.